📑 Chapter Navigation

Report Structure

Analysis Framework

📖 Complete Course Navigation

Foundation (Ch 1-4)

Analysis (Ch 5-8)

Advanced (Ch 9-13)

- Ch 9: Corporate Actions

- Ch 10: Valuation Principles

- Ch 11: Commodities "chapter-012.php" style="color: #2E7D32; text-decoration: none;">Ch 12: Risk and Return

- Ch 13: Research Reports

- Ch 14: Legal Framework

- Ch 15: Technical Analysis

Annexures (Ch 14-16)

LEARNING OBJECTIVES:

After studying this chapter, you should know about:

- Essentials of a Good Research Report

- Checklist based approach to writing research reports

12.1 Qualities of a Good Research Report

Research report is a multipurpose document and does the following:

Presents an investment idea - Provides market perspective - Detailed company analysis.

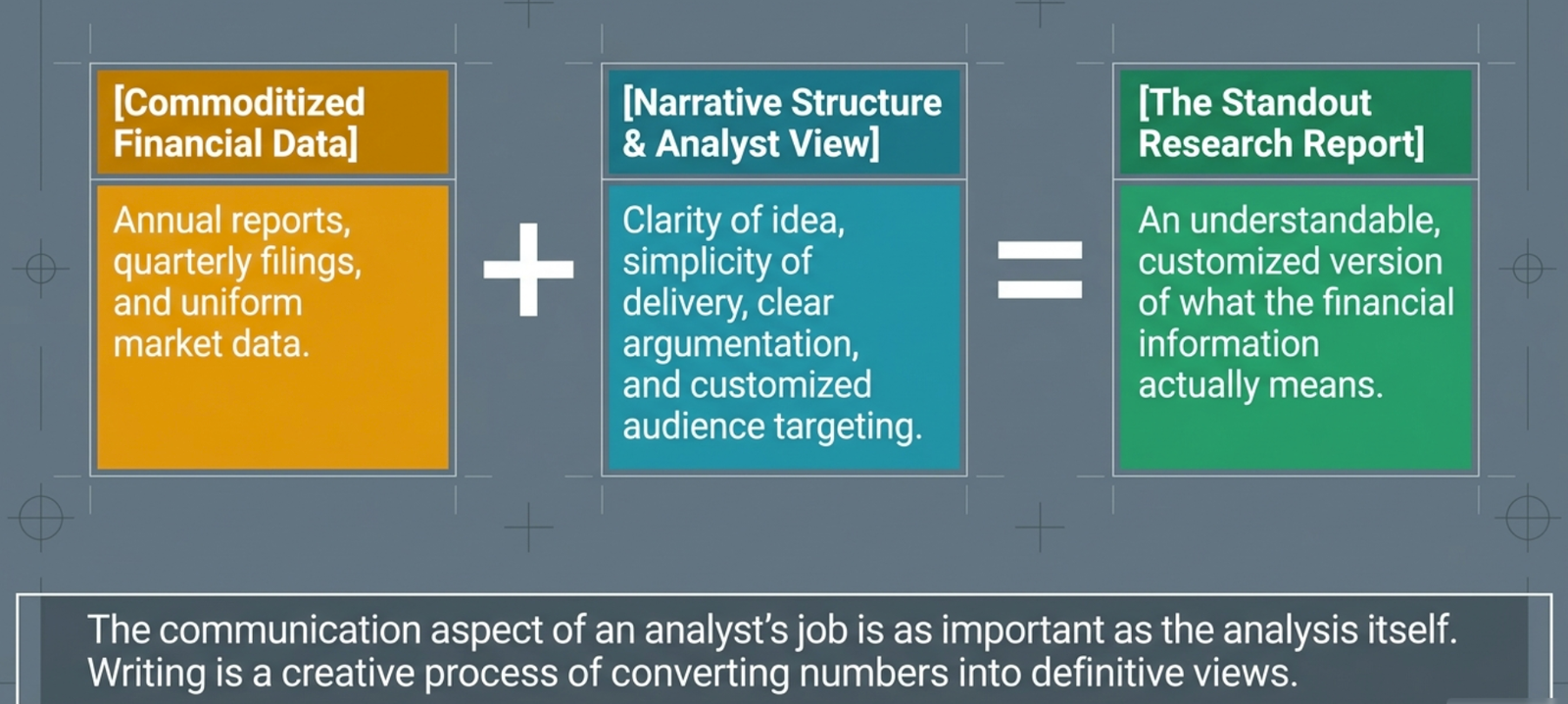

All the research analysts have access to, more or less, the same information i.e. annual reports, quarterly reports etc., In-fact, all good analysts and experts of a sector have similar things to say. So how does one stand out and be the best?

Research analysts, make a difference by the way in which they present their views, conclusions and recommendations. The communication aspect of an analyst's job is as important as analysis, of which writing research report is one.

Writing research reports, to an extent, is a creative process: creativity in the sense of how one structures the report and communicates the message. What an analyst does is to take in is a lot of financial information and give out is an understandable version of what that financial information mean. The process of converting numbers to views does demand for the certain qualities. As with many other creative processes, there is no single answer to this question but there are certain ground rules which one can follow to make a good report.

Key Elements of Good Research Reports:

- Clarity of Idea

- Simplicity of delivery

- Presenting the argument clearly

- Narrative structure

- Create customized reports according to the reader type

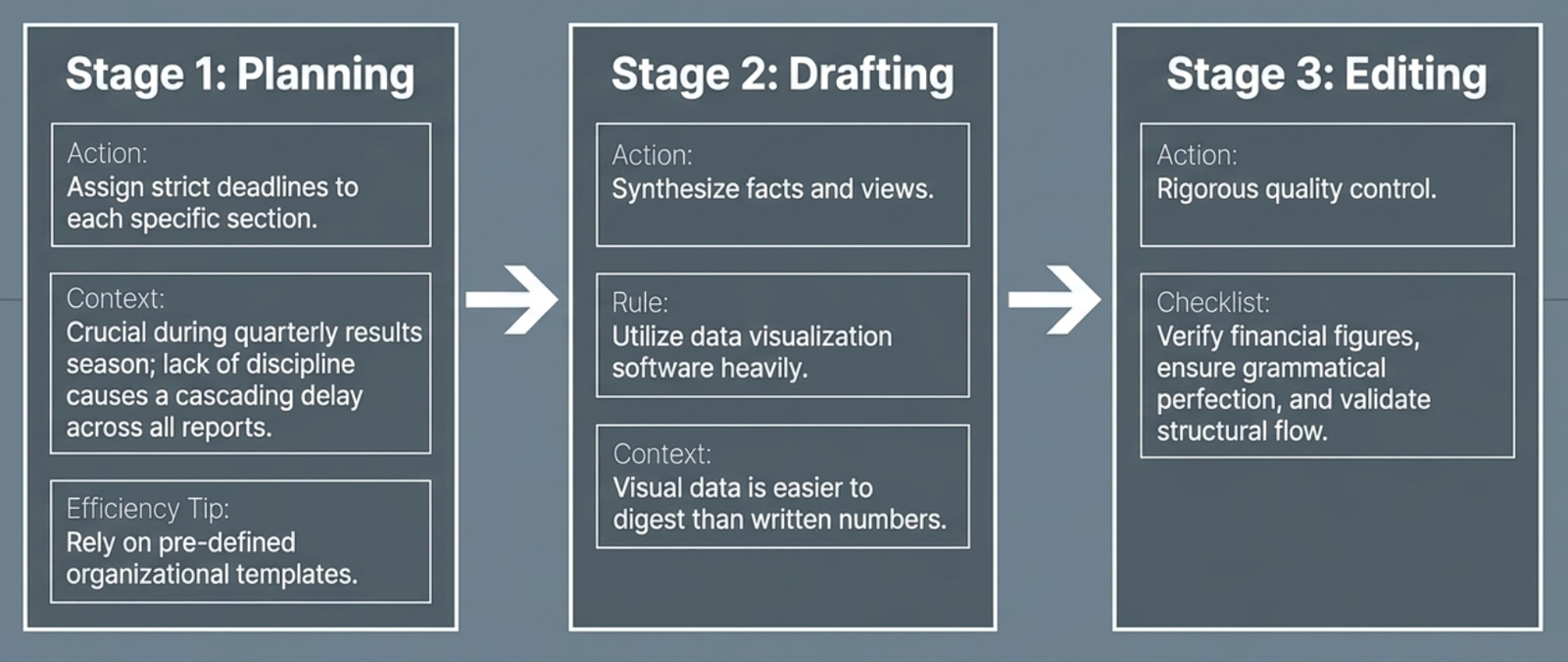

Writing a good research report - Planning, Drafting and Editing:

Like any other writing projects, compiling research reports also have three important steps - Planning, Drafting and Editing. The major sections of a research report include:

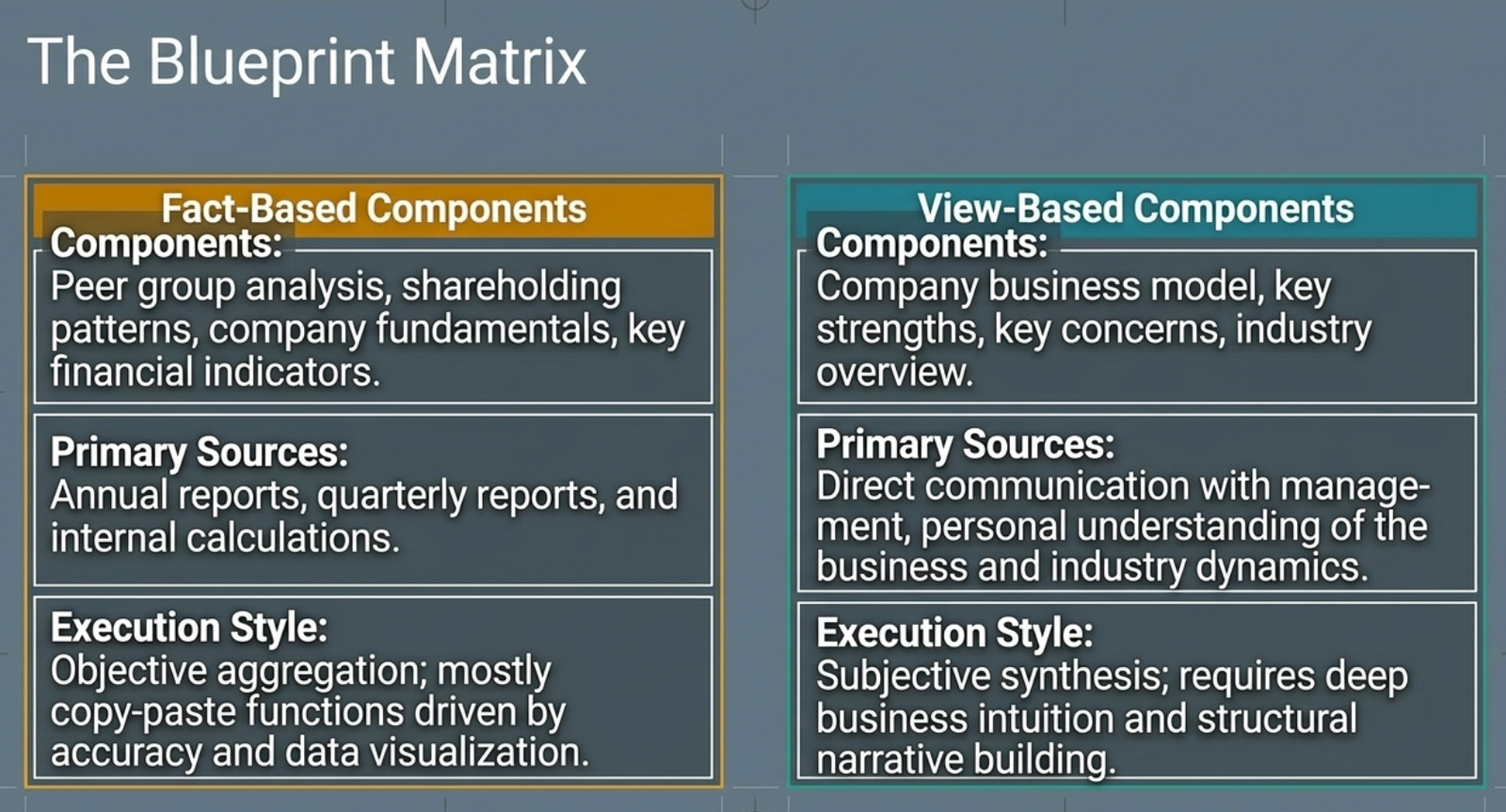

Company business, peer group analysis, shareholding pattern, key strengths, key concerns, industry overview, company fundamentals, key financial indicators and financials.

The writing process has to be planned as to how each section will be approached and assign a deadline to each. As there are many reports to be written and the work load shall be high near quarterly results season, it is important to maintain high levels of discipline otherwise the delay can have a cascading effect on the work.

Once done with the planning, work should begin on each section. Generally, each organization has a template of its own and therefore working on a pre-defined structure makes the work a little bit easier. Almost all the sections of a research report are fact based and therefore filling them is more of a copy-paste function but certain important sections require understanding of the business and thorough communication with management.

Fact-based sections in research report:

Peer group analysis, shareholding pattern, company fundamentals, key financial indicators and financials.

Source of information: Annual reports, quarterly reports, calculations.

View-based section in research report:

Company Business, Key Strengths, Key concerns, Industry Overview.

Source of information: Communication with management, Personal Understanding of the business and industry.

It is also suggested to make use of data visualization software's and prepare visual charts to present the data. Visual data is easier to understand than written numbers.

Once a draft is ready it should be rechecked for financial figures, spell-checks and grammatical errors and edited accordingly.

Things to watch-out:

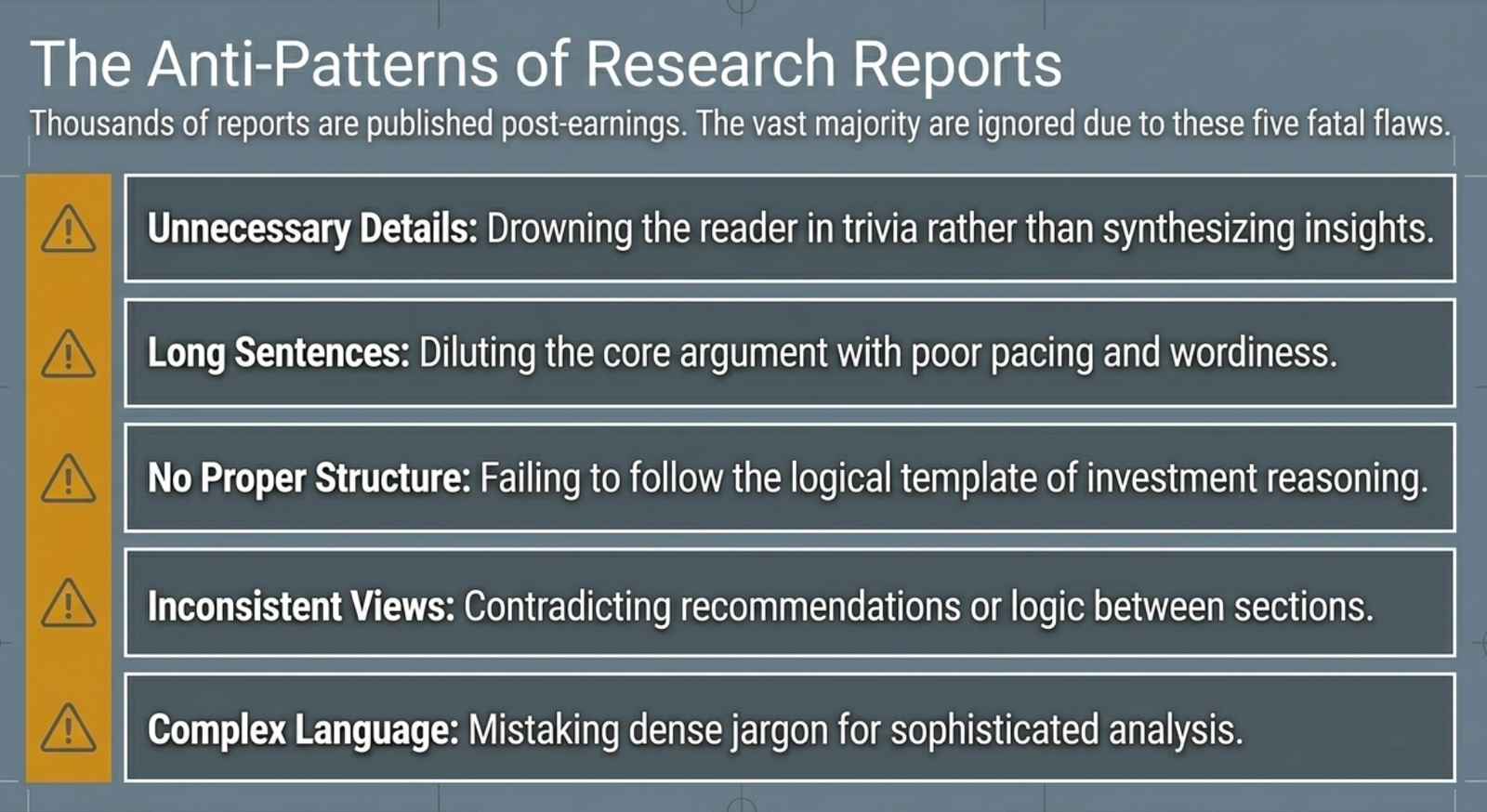

There are thousands of reports prepared after every results season and only a few of them get the attention. What makes the other reports fail? After observation of many years, the following are a few reasons that are listed out for failure of a research report:

- Unnecessary details

- Long sentences

- No proper structure

- Inconsistent views

- Complex language

Rating Conventions

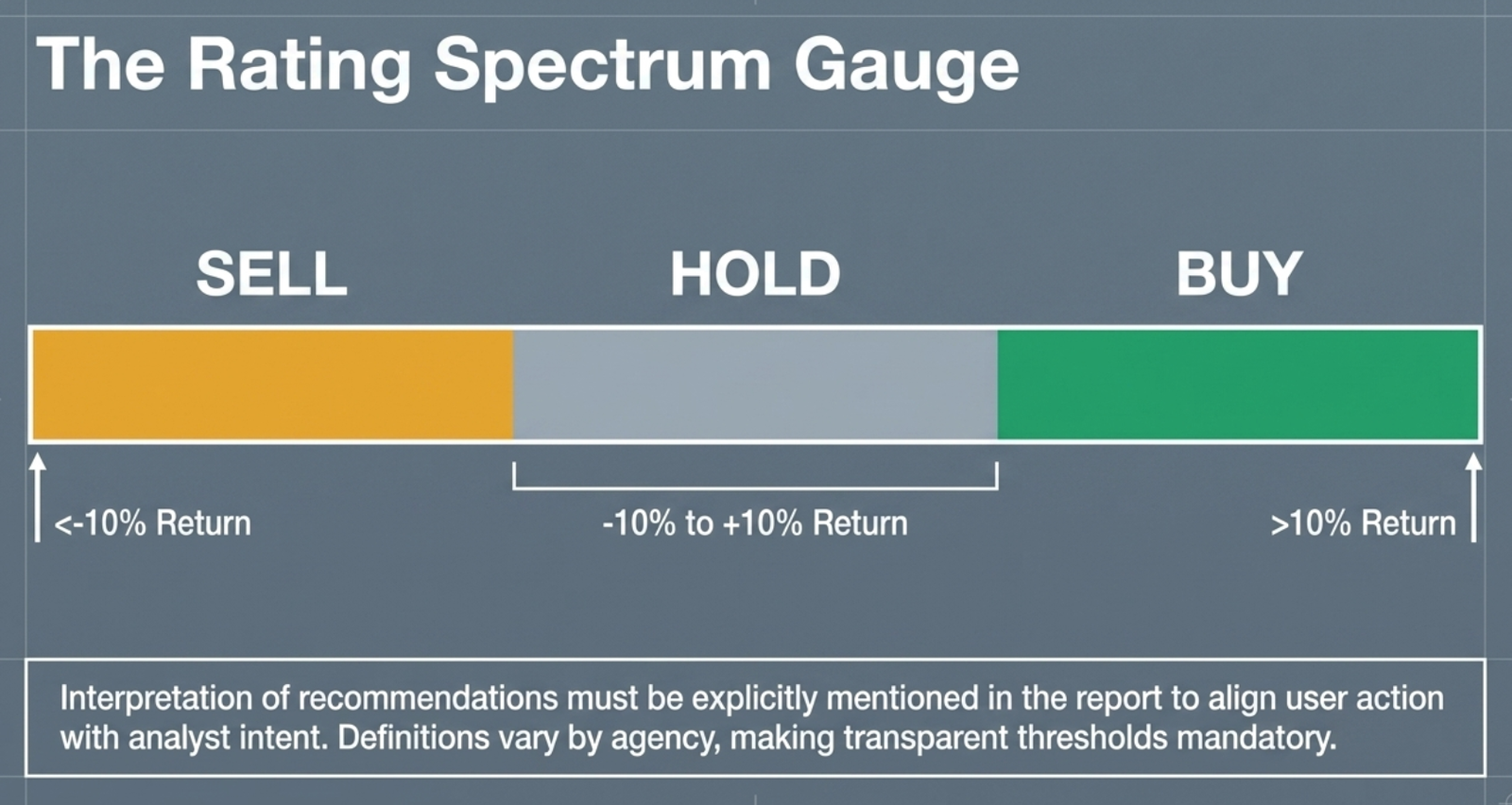

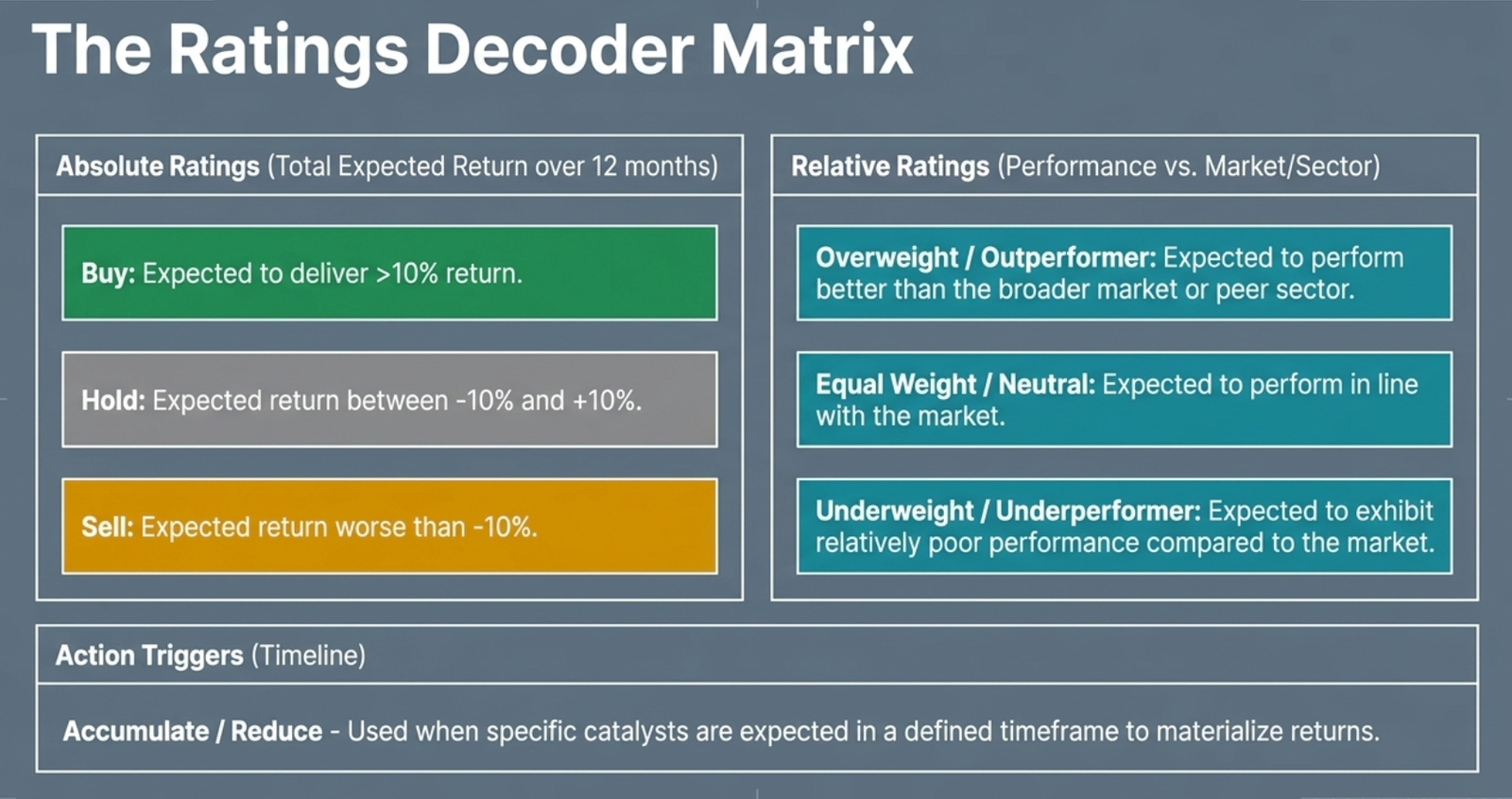

In financial markets, while rating stocks, various conventions are used by the research analysts. The prevalent recommendations include: "buy", "overweight", "hold", "underweight" and "sell". These recommendations are typically made to reflect the analyst's view on the total returns that the security will make over a specified time horizon, or the returns of the security relative to the returns of the market or to the peer group. Different research agencies may have different definitions for each term. The interpretation of the recommendation is also typically mentioned in the research report for the immediate reference of the user.

For example, a 'buy' may indicate an expectation that the stock will deliver more than 10% returns over the next 12-month period, 'hold' may indicate that the stock's return is expected to range between -10% and 10% over the next 12-month period and a 'sell' recommendation may indicate an expected return of less than -10% over the period.

Analysts also use recommendations such as 'accumulate' and 'reduce' to reflect a view that triggers for the stock's performance is expected in the defined time frame, which will result in the returns materialising.

'Outperformer', 'performer or neutral' and 'underperformer' indicate the expectation of the stock's returns relative to the sector or market. The analyst may even indicate the expected level of out/underperformance.

'Overweight', 'equal weight' and 'underweight' are ratings used to describe a stock or sectors performance relative to the market. An 'overweight' rating indicates the expectation that the stock or sector will perform better than the market, while 'underweight' indicates a relatively poor performance and 'equal weight' indicates performance in line with the market.

12.2 Checklist Based Approach to the Research Reports

In the era of information overload, it is easy to drown in the ocean of information around. Also, sometimes, information available at different places is contradictory. To ensure consistency in the decision making process, it becomes imperative to note down important decision drivers in a disciplined and committed manner. Please remember that market rewards disciplined investing and often punishes emotional, distracted and disorganized approaches.

Accordingly, checklists could be a great way for analysts to stay disciplined and methodical when it comes to researching new ideas, maintaining an existing portfolio and exiting positions. Just as airline and military pilots have used checklists for decades to eliminate avoidable accidents and produce better results, so too can investors use checklists to develop better and more consistent investment behaviours.

Obvious advantages of checklist approach are:

- Checklist helps avoid lazy mistakes or short-cuts.

- Checklist ensures than an analyst always does what he or she intends to do in a disciplined manner.

- Checklists help in objective and facts based decisions.

- Checklists leave a decision-making trail that can be modified and corrected with time.

In a popular book "The Checklist Manifesto", author, Dr. Atul Gawande makes a distinction between errors of ignorance (mistakes made out of ignorance), and errors of ineptitude (mistakes made because of incorrect use of knowledge). He argues that errors of second type can be avoided to a large extent by following a checklist approach to literally everything in life.

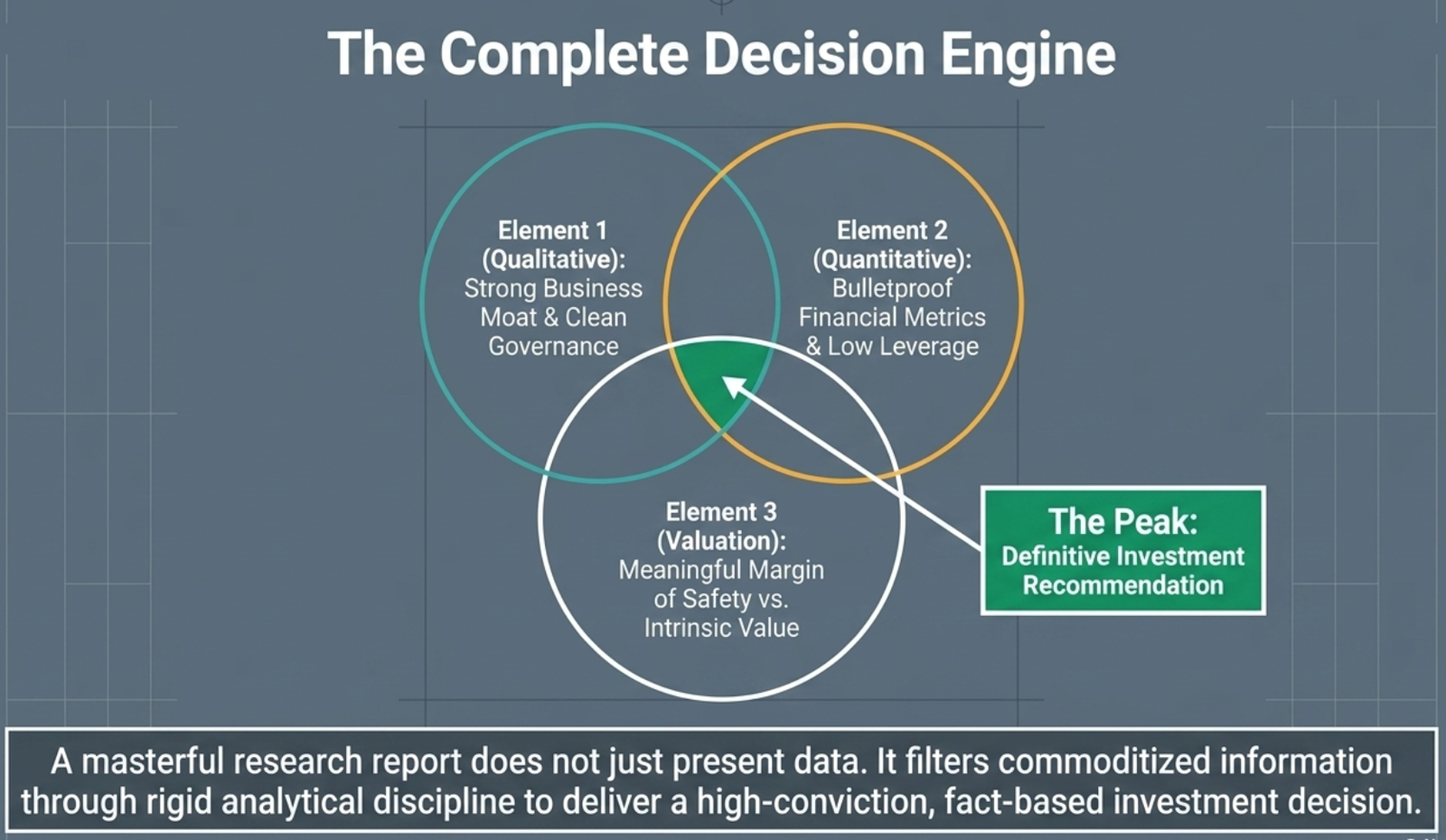

12.3 A Sample Checklist for Investment Research Reports

Here is a sample checklist for investment research. We must state that the questions given in the checklist are only indicative in nature and readers may add/delete/edit the questions to the checklist as per their requirements. Financial parameters taken in the quantitative section are also indicative only for reference purpose.

Qualitative Parameters

| Parameter | Check |

|---|---|

| Do I understand the business | ☐ |

| Details of technology collaboration, if any | ☐ |

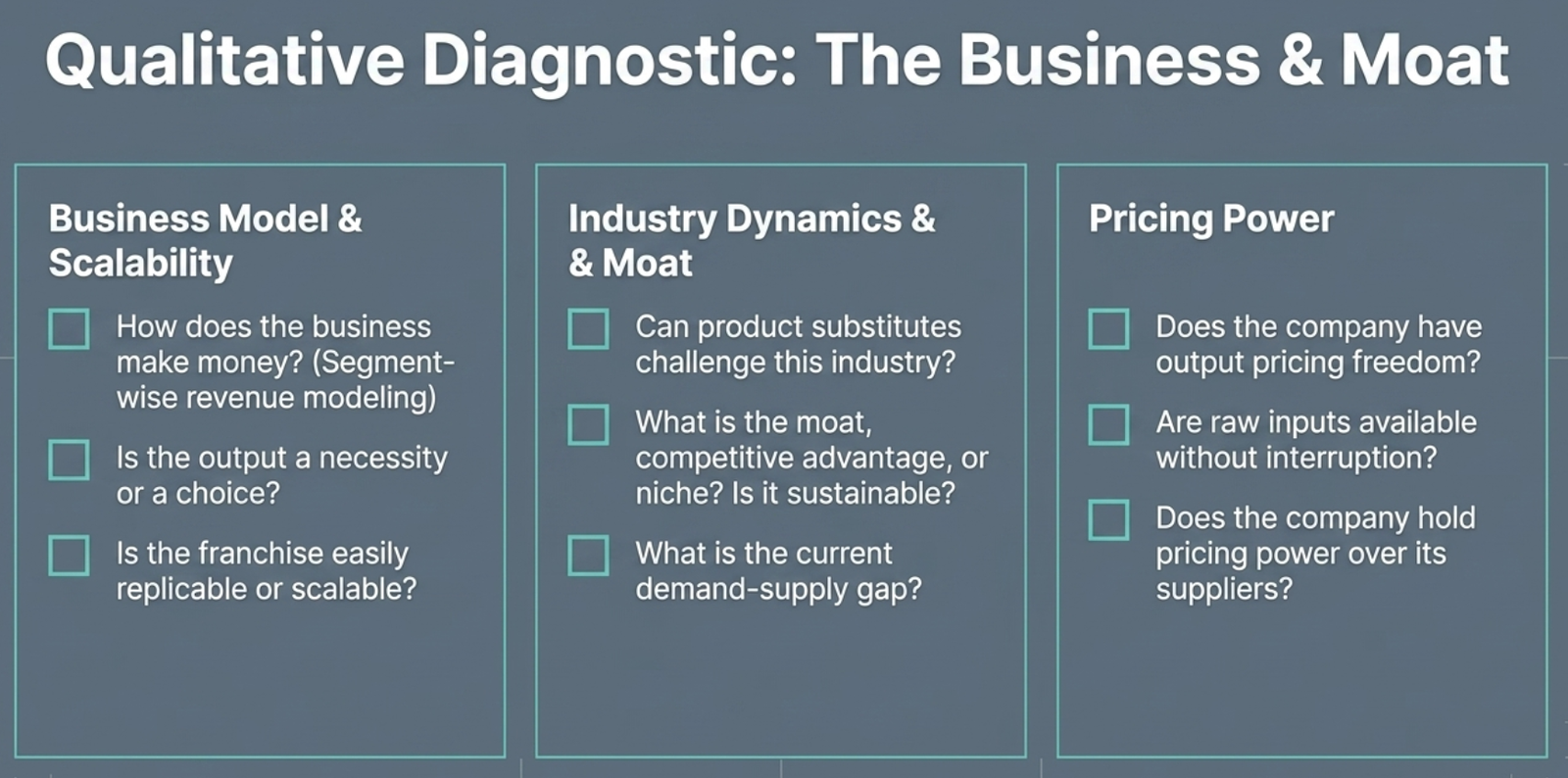

| What is the revenue model – how does business make money. What is segment wise revenue contribution and how it is supposed to change going forward. | ☐ |

| Output is a necessity or a choice | ☐ |

| Can other industry/business challenge this industry/business (is there a product substitute). If yes, which and to what extent | ☐ |

| What are distribution channels (marketing infrastructure) | ☐ |

| Is the business replicable/scalable/good franchise business | ☐ |

| What is Demand – Supply gap in the industry and sustainability of its gap | ☐ |

| How does business look like a decade down the line? Would it be existing and be more valuable | ☐ |

| What is the moat/competitive advantage/niche/differentiation of company and sustainability of these characteristics | ☐ |

| What is downside /Risks in the business/company/industry | ☐ |

| Does the company has output pricing freedom/ability and sustainability of this pricing power | ☐ |

| Are inputs available without interruption? Pricing power of company on inputs and sustainability of this pricing power | ☐ |

| What is the level of competition in business (major competitors and company's position vis a vis competitors). Are entry barriers in business significantly strong? | ☐ |

| What is the quality of management – able, honest and with good integrity | ☐ |

| What is promoter's stake? What are insiders doing (buying/selling by promoters and top mgmt.). Any pledge of shares by promoters. | ☐ |

| Any buy back by the company in last three years. | ☐ |

| Any major observation from corporate governance report | ☐ |

| Present shareholding pattern. Changes in SH pattern over last 5 yrs. List of top 10 shareholders (with % shareholding). | ☐ |

| Is there a catalyst in business | ☐ |

| Can a fool/idiot run this business (Business is simple, output is a necessity and competition is not tough) | ☐ |

| Strengths of company | ☐ |

| Weaknesses of company and how company is handling them | ☐ |

| Opportunities to company and how company is tapping them | ☐ |

| Threats to company and how company is handling them | ☐ |

Quantitative Parameters

| Parameter | Check |

|---|---|

| Equity History and important points | ☐ |

| Has the revenues been growing consistently. Do we have visibility of revenues going forward | ☐ |

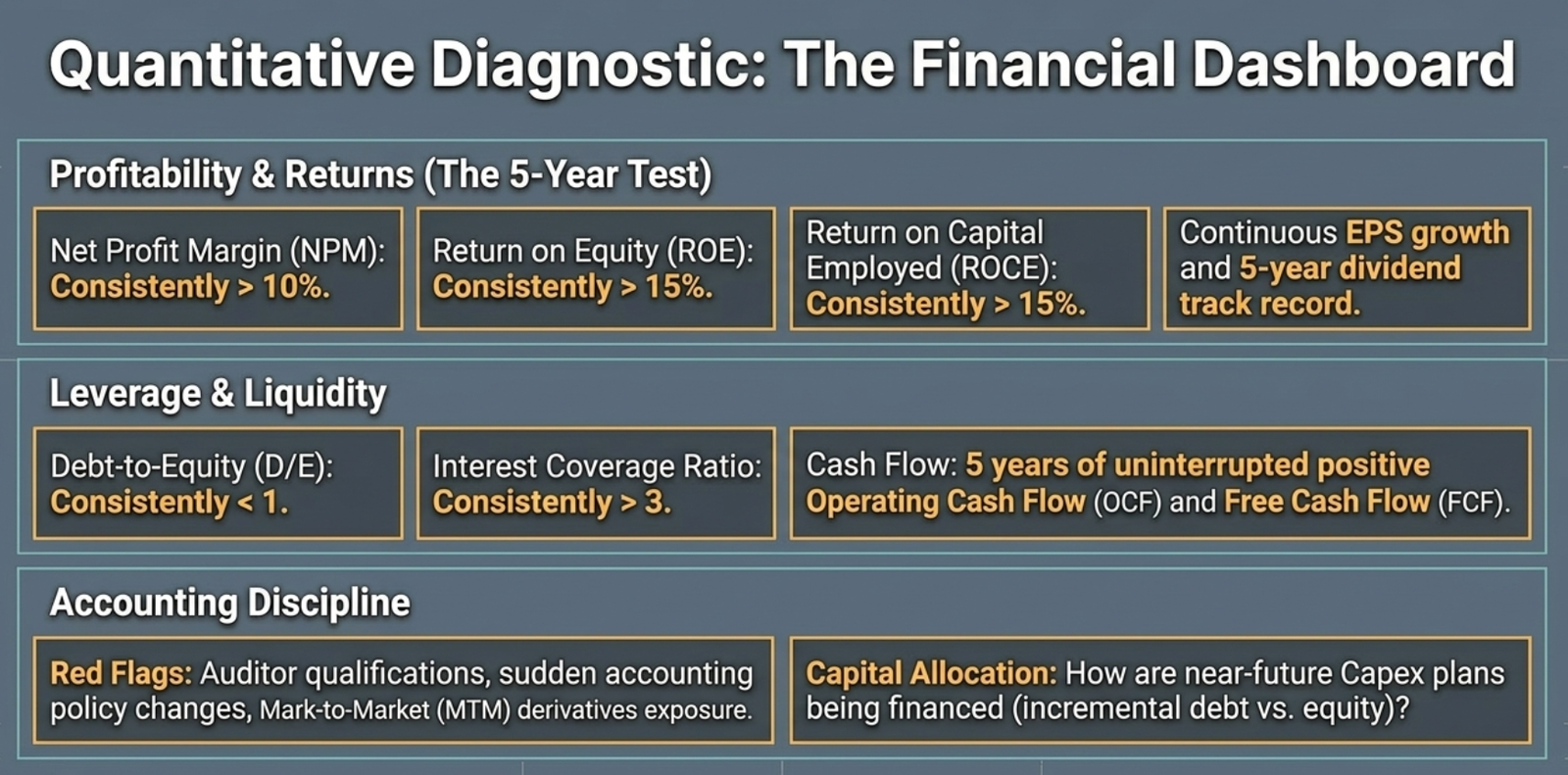

| Whether business has stable and growing profitability (NPM > 10% and growth in EPS continuously over last 5 years) | ☐ |

| Whether business has low leverage (D/E<1 continuously and interest coverage > 3 continuously over last 5 years) | ☐ |

| Whether company has stable and growing return track record (ROE> 15% and ROCE > 15% continuously over last 5 years) | ☐ |

| Whether company has stable and growing min. 5 years dividend track record | ☐ |

| Whether company has good cash flows (positive operating cash flows and positive free cash flows continuously over last 5 years). | ☐ |

| Any important/notable auditors' qualification | ☐ |

| Any important observation from notes to accounts (intangibles, MTMs on outstanding derivatives and guarantees etc.). Any change in the accounting policy with impact on P/L and B/S. | ☐ |

| What are company's capex plans in near future and how does co. propose to finance that. | ☐ |

| Incremental capital – equity and/or debt planned? | ☐ |

| Is the company financially disciplined? Am I buying this business for quality of assets, earnings and cash flows? | ☐ |

Valuation Parameters

| Parameter | Check |

|---|---|

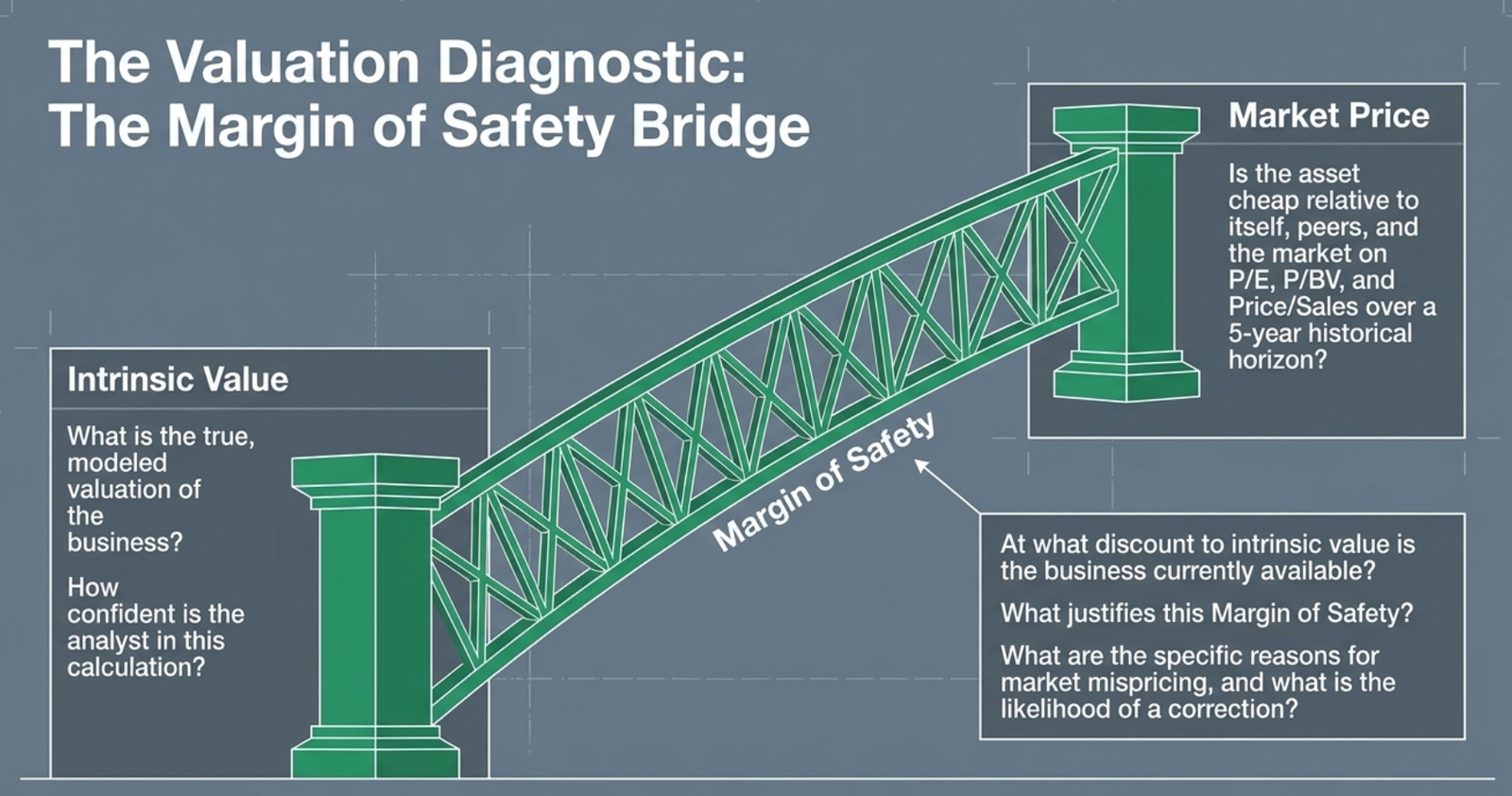

| What is Valuation/intrinsic value of the business? How confident I am on valuation | ☐ |

| Is business cheap relative to itself, peers and market on various valuation parameters (Price, P/E, P/BV, Price/Sales etc.) over a period of time (Last 5 years) | ☐ |

| What justifies Margin of Safety (MOS). Business is available at what discount to its intrinsic value | ☐ |

| Reasons of market mispricing and likelihood of correction. | ☐ |

Final Decision Parameters

☐

Sample Research Reports:

🃏 Flashcards

48 cards · click to reveal the answer · use search to focus on a topic

Sample Questions

1. For analysts, which is the authentic source to check facts on a Company?

a. Annual Reports

b. Research reports and opinions of Research Analysts

c. Media reports

d. Business Portals

2. Leverage ratio is a part of __________ parameter of business analysis.

a. Qualitative

b. Quantitative

c. Descriptive

d. Behavioural

3. Which of the following is not a valuation parameter for business analysis?

a. Intrinsic Value

b. P/BV Ratio

c. P/E Ratio

d. Demand & Supply of Securities in the market

4. If a stock has exceeded its Target Price, an analyst may recommend __________.

a. Buy

b. Sell

c. Hold

Continue Your Learning Journey

You've completed Chapter 13! Here's what comes next: