📑 Chapter Navigation

Core Corporate Actions

Capital Structure Changes

Corporate Restructuring

Assessment & Practice

📖 Complete Course Navigation

Foundation (Ch 1-4)

Analysis (Ch 5-8)

Advanced (Ch 9-13)

Annexures (Ch 14-16)

📚 Learning Objectives

After studying this chapter, you should know about:

- Philosophy of corporate actions and their impact on shareholders

- Understanding dividend policy and its implications

- Analysis of rights issues, bonus issues, and stock splits

- Share buyback mechanisms and their effects

- Mergers, acquisitions, and demergers

- Delisting procedures and regulatory requirements

9.1 Philosophy behind Corporate Actions

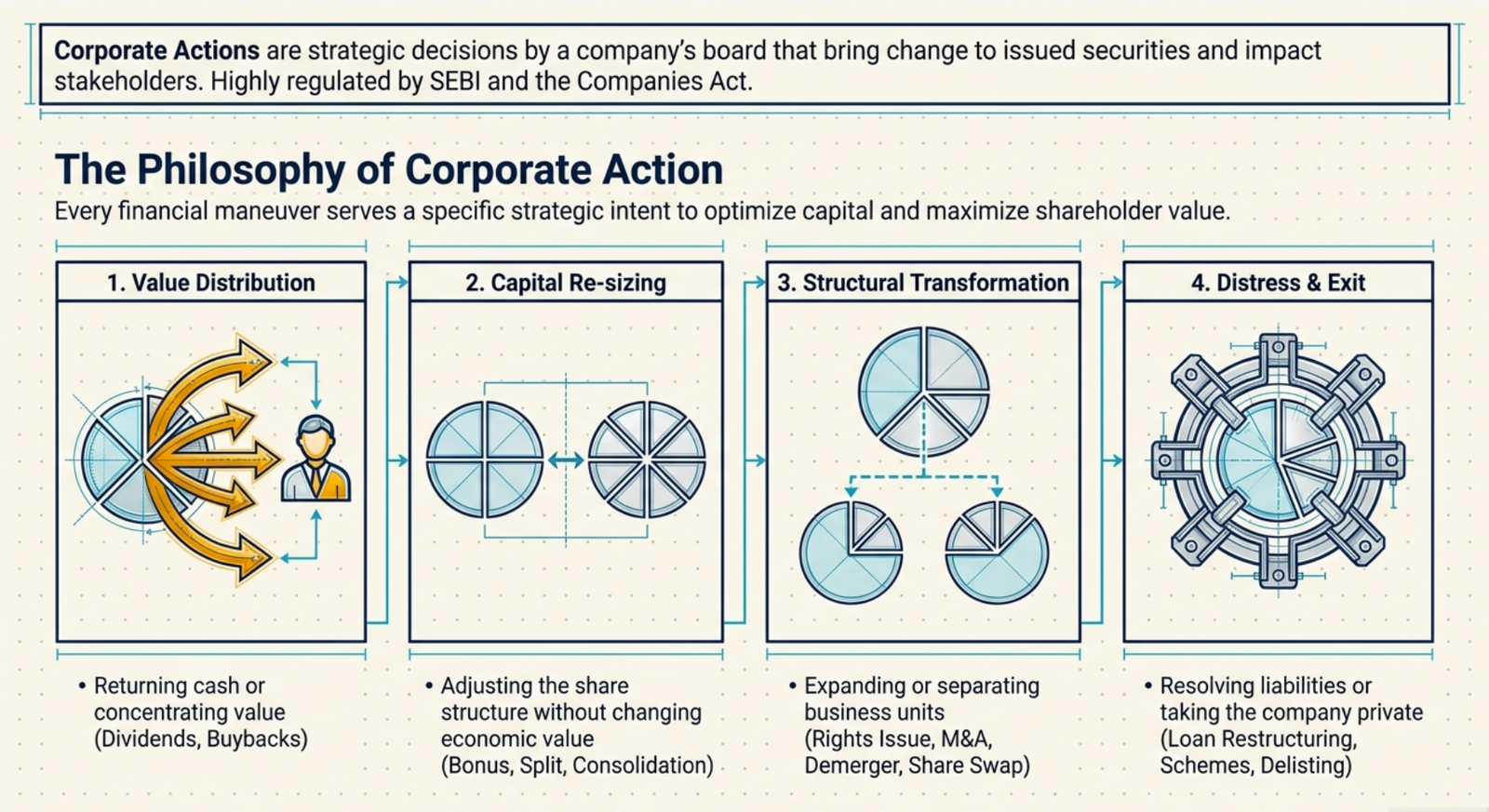

Corporate actions are strategic decisions made by a company's board of directors that will bring change to the securities (equity or debt) issued by the company and impact its shareholders and bondholders. Companies initiate corporate actions to achieve various objectives related to capital structure optimization, business strategy, and shareholder value creation.

Key Principle: All corporate actions are fundamentally driven by the goal of maximizing shareholder value over the long term, though the immediate impact may vary depending on the specific action and market conditions.

Primary Reasons for Corporate Actions

- Capital Optimization: Adjusting the capital structure to reduce cost of capital

- Liquidity Enhancement: Improving trading volumes and market participation

- Growth Funding: Raising capital for expansion and new projects

- Tax Efficiency: Optimizing tax implications for both company and shareholders

- Market Signaling: Conveying management's confidence in future prospects

- Strategic Restructuring: Realigning business focus and operations

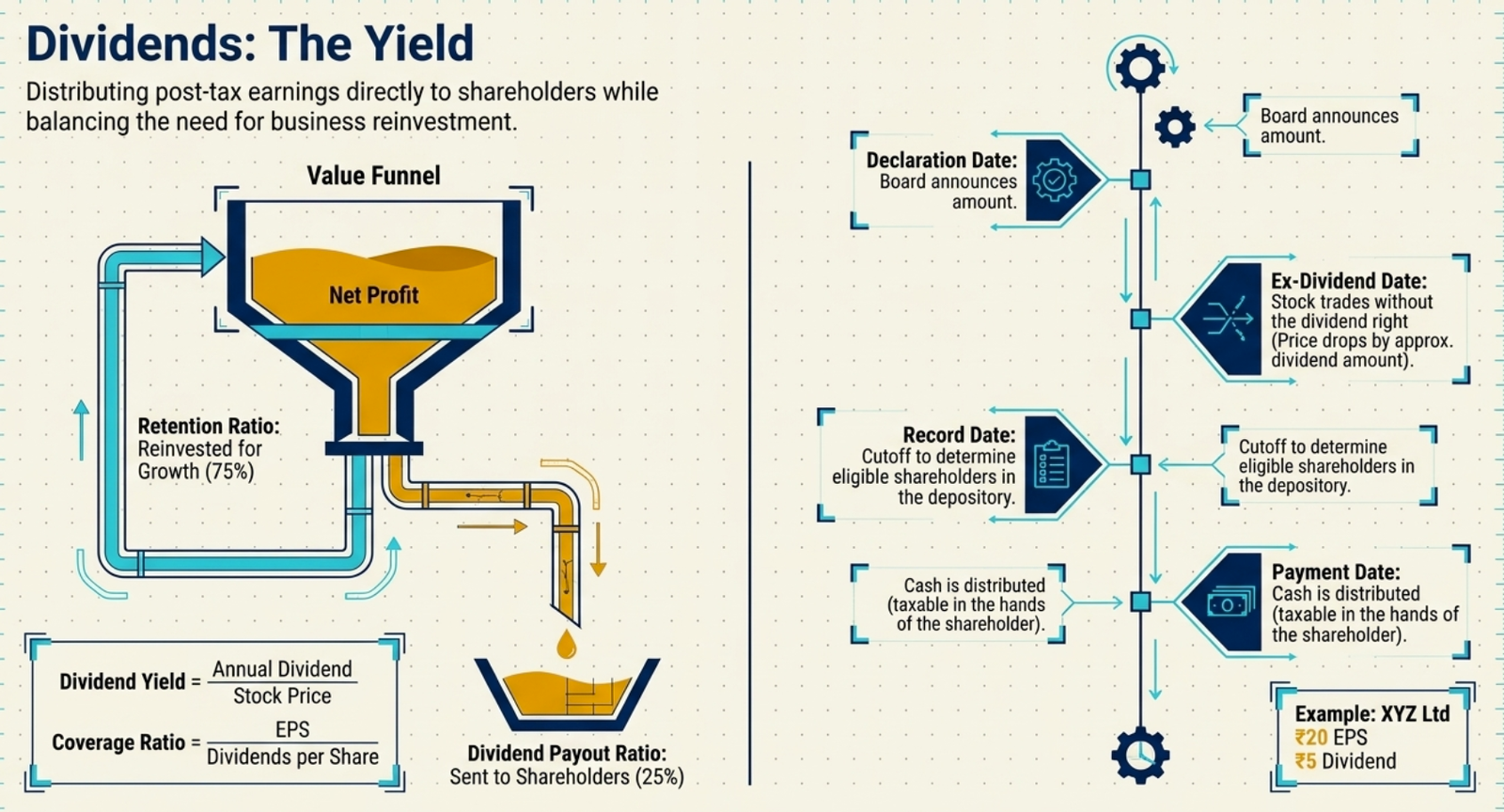

9.2 Dividend and Its Analysis

Dividends represent the distribution of a company's earnings to its shareholders. The dividend policy reflects management's strategy regarding cash distribution versus reinvestment for growth. Understanding dividend analysis is crucial for evaluating a company's financial health and management priorities.

9.2.1 Types of Dividends

| Dividend Type | Description | Characteristics | Tax Implications |

|---|---|---|---|

| Cash Dividend | Direct cash payment to shareholders | Most common form, provides immediate liquidity | Taxable in hands of shareholders |

| Stock Dividend | Additional shares given instead of cash | Increases shareholding proportionally | Generally not taxable at receipt |

| Property Dividend | Distribution of assets other than cash | Rare, usually involves subsidiary shares | Taxed at fair market value |

| Special Dividend | One-time extraordinary distribution | Usually from asset sale or windfall gains | Same as regular dividend |

9.2.2 Dividend Analysis Framework

Key Dividend Metrics

Dividend Yield = Annual Dividend per Share / Current Stock Price

Dividend Payout Ratio = Dividends per Share / Earnings per Share

Dividend Coverage Ratio = Earnings per Share / Dividends per Share

Retention Ratio = (1 - Dividend Payout Ratio)

Dividend Analysis Example: XYZ Ltd

Given Data:

- Current Stock Price: ₹100

- Annual Dividend: ₹5 per share

- Earnings per Share: ₹20

- Number of Shares: 1 million

Calculations:

Dividend Yield = ₹5 / ₹100 = 5%

Dividend Payout Ratio = ₹5 / ₹20 = 25%

Dividend Coverage Ratio = ₹20 / ₹5 = 4x

Retention Ratio = 1 - 0.25 = 75%

Analysis: The company has a conservative dividend policy, retaining 75% of earnings for growth while providing a reasonable 5% yield to shareholders. The 4x coverage ratio indicates sustainable dividend payments.

9.2.3 Dividend Timeline and Important Dates

Key Dividend Dates

- Declaration Date: Board announces dividend amount and payment date

- Ex-Dividend Date: First day stock trades without dividend right

- Record Date: Date to determine eligible shareholders

- Payment Date: Actual dividend distribution date

Expected Price Behavior Around Dividend Dates

Before Ex-Dividend Date: Stock price typically increases as investors buy to capture dividend

On Ex-Dividend Date: Stock price usually drops by approximately the dividend amount

After Payment: Price behavior depends on market conditions and company fundamentals

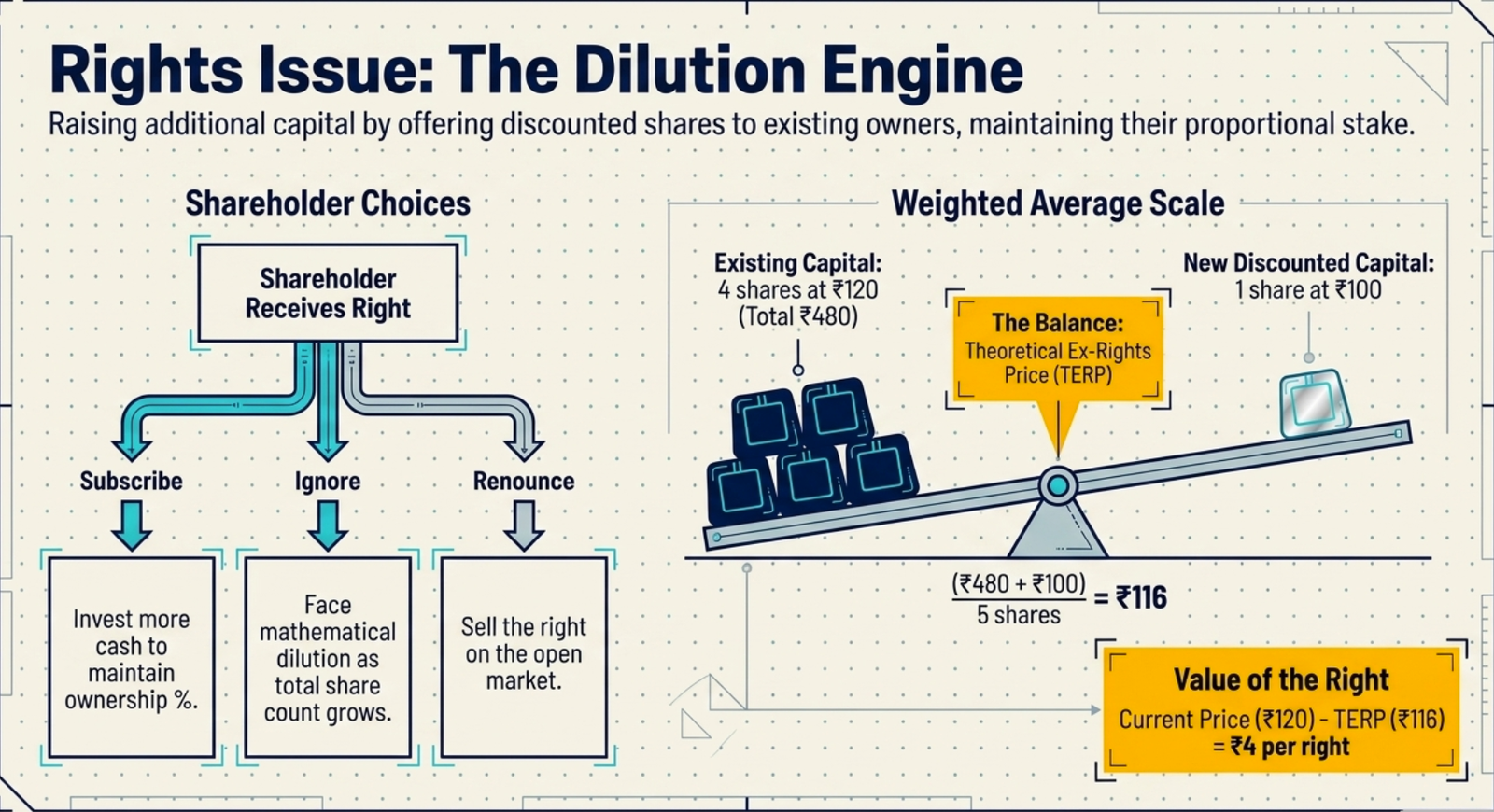

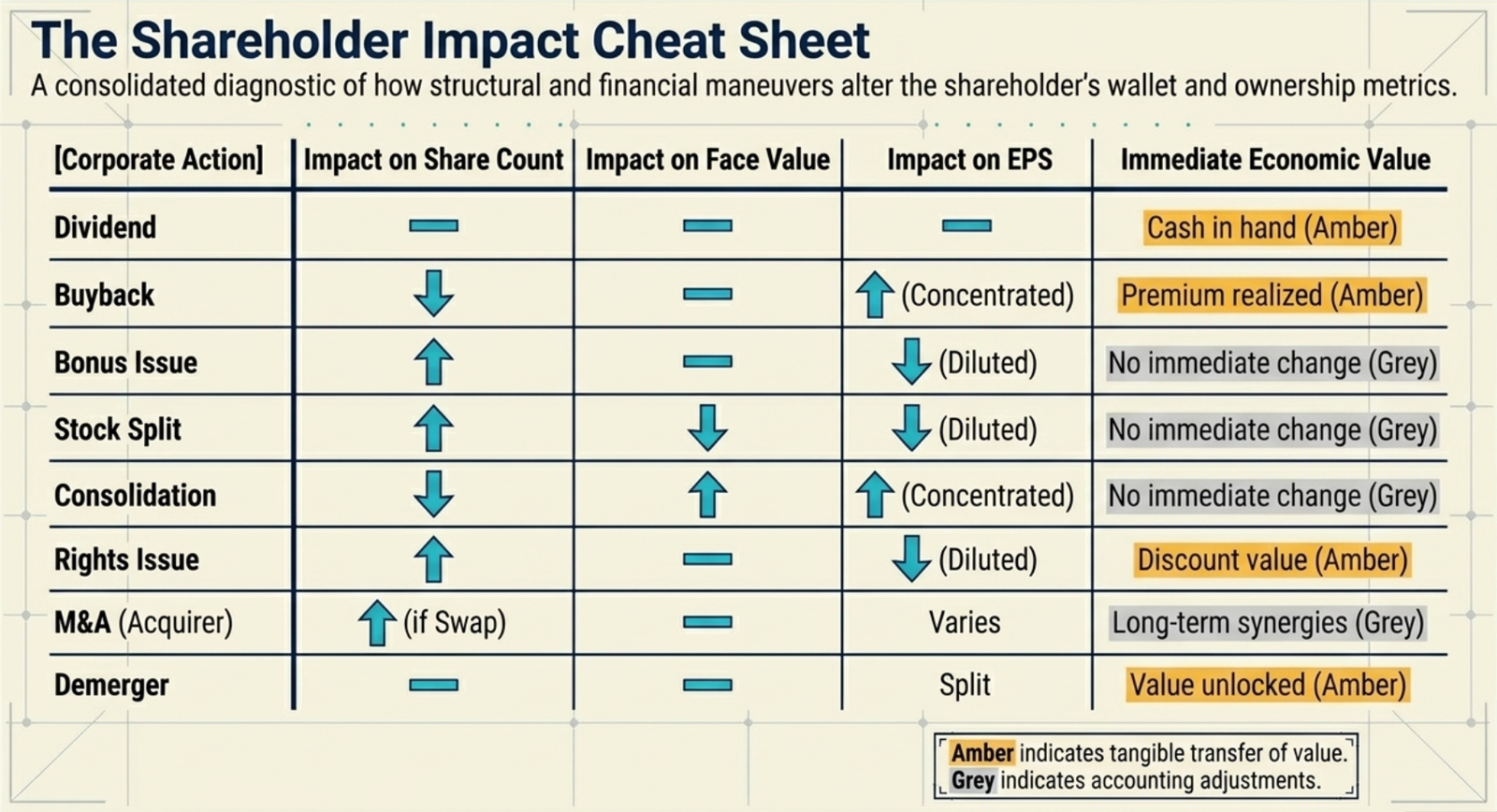

9.3 Rights Issue

A rights issue is a method of raising additional capital by offering existing shareholders the right to purchase new shares at a discounted price, typically proportional to their current shareholding. This maintains existing shareholders' proportional ownership while raising funds for the company.

9.3.1 Rights Issue Mechanism

Rights Issue Process

- Board Approval: Directors approve the rights issue proposal

- Shareholder Approval: Special resolution passed in general meeting

- Regulatory Approvals: SEBI and stock exchange clearances

- Rights Entitlement: Determination of rights ratio and price

- Trading Period: Rights can be traded separately

- Subscription Period: Shareholders exercise or sell rights

- Allotment: New shares allotted to subscribers

Rights Issue Calculations

Rights Ratio: Number of new shares offered per existing shares held

Subscription Price: Price at which new shares are offered (usually at discount)

Theoretical Ex-Rights Price (TERP) = [(Existing Shares × Current Price) + (New Shares × Rights Price)] / Total Shares after Rights

Value of Right = Current Price - TERP

Rights Issue Example: ABC Corporation

Scenario:

- Current Share Price: ₹120

- Rights Ratio: 1:4 (1 new share for every 4 existing shares)

- Rights Issue Price: ₹100

- Existing Shares: 4 million

Calculations:

New Shares to be Issued = 4 million / 4 = 1 million

Total Shares after Rights = 4 million + 1 million = 5 million

TERP = [(4M × ₹120) + (1M × ₹100)] / 5M = ₹580M / 5M = ₹116

Value of Right = ₹120 - ₹116 = ₹4 per right

For a shareholder holding 100 shares:

Rights Entitlement = 100 / 4 = 25 new shares

Investment Required = 25 × ₹100 = ₹2,500

Value of Rights = 25 × ₹4 = ₹100

9.3.2 Advantages and Disadvantages of Rights Issue

✅ Advantages

- Proportional Ownership: Existing shareholders maintain their percentage stake

- Preferential Access: Existing shareholders get first preference

- Lower Cost: Cheaper than public offerings for companies

- Tradeable Rights: Non-participating shareholders can sell rights

- Flexible Participation: Shareholders can choose participation level

❌ Disadvantages

- Dilution Risk: Non-participating shareholders face dilution

- Discount Impact: Issue price usually below market price

- Market Pressure: Can depress stock price temporarily

- Additional Investment: Shareholders need extra capital

- Complexity: Process can be complicated for retail investors

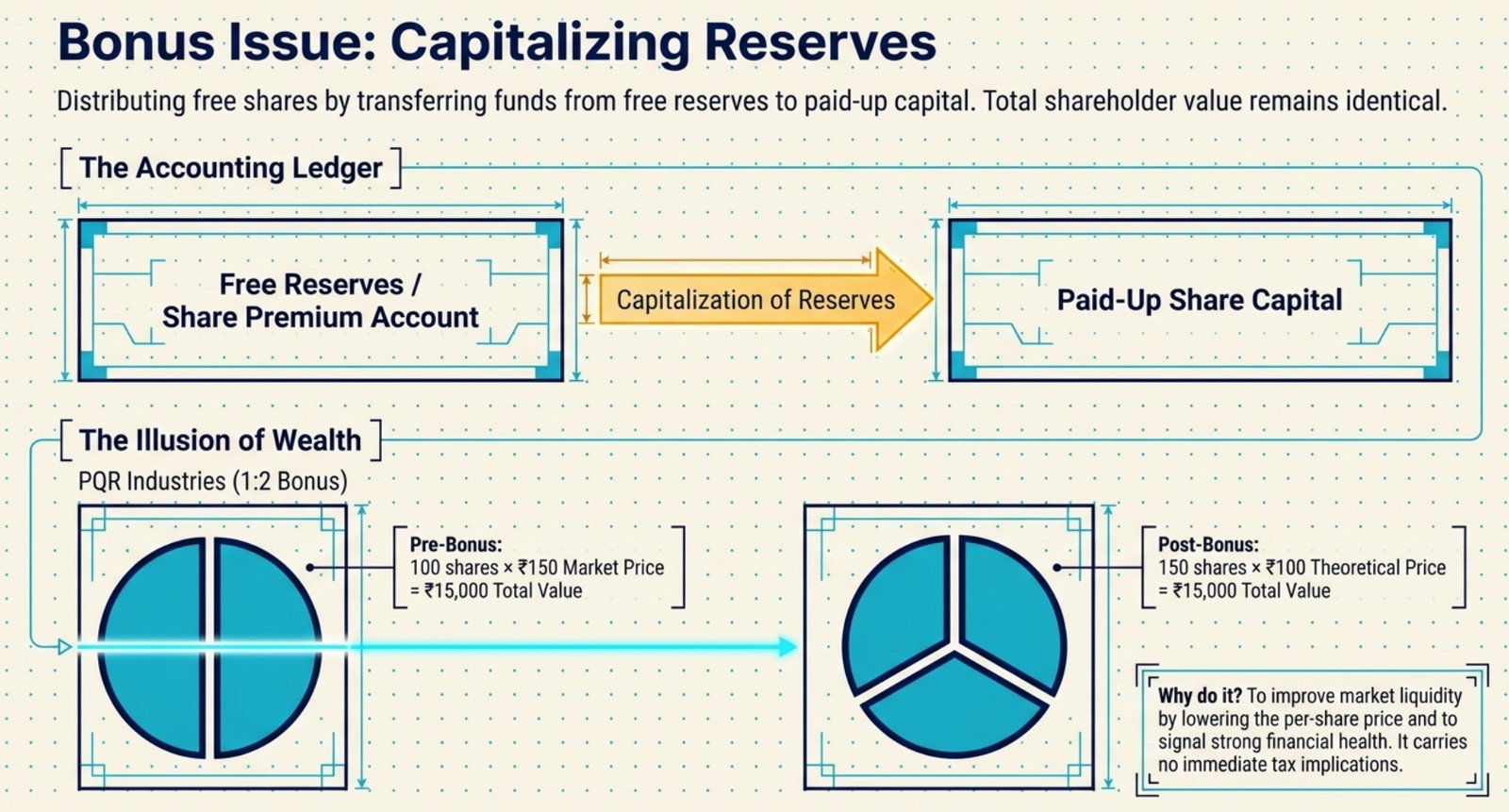

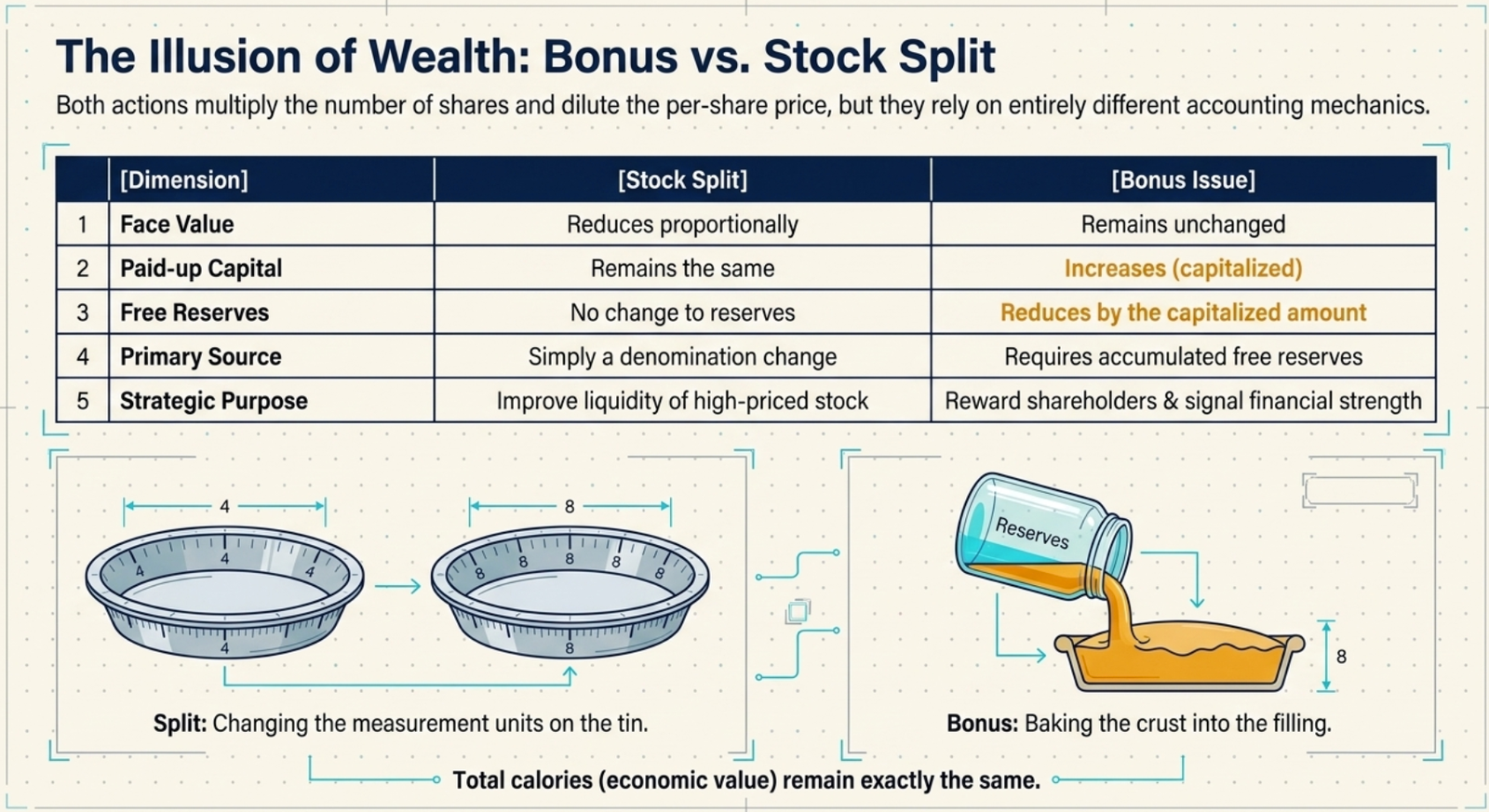

9.4 Bonus Issue

A bonus issue involves the distribution of additional shares to existing shareholders free of cost, proportional to their current shareholding. This corporate action capitalizes reserves and surplus into equity capital without changing the shareholders' proportional ownership.

9.4.1 Bonus Issue Mechanism

Sources for Bonus Issue

- Free Reserves: Accumulated profits available for distribution

- Share Premium Account: Premium collected on earlier share issues

- Capital Redemption Reserve: Reserve created during share buybacks

- Securities Premium Account: Premium from securities other than shares

Common Bonus Ratios

1:1 Ratio - 1 bonus share for every 1 existing share (doubles shareholding)

1:2 Ratio - 1 bonus share for every 2 existing shares (50% increase)

2:5 Ratio - 2 bonus shares for every 5 existing shares (40% increase)

3:10 Ratio - 3 bonus shares for every 10 existing shares (30% increase)

Bonus Issue Example: PQR Industries

Before Bonus Issue:

- Share Capital: ₹10 crores (1 crore shares of ₹10 each)

- Free Reserves: ₹15 crores

- Market Price per Share: ₹150

- Market Capitalization: ₹150 crores

Bonus Ratio: 1:2 (1 bonus share for every 2 existing shares)

After Bonus Issue:

New Shares Issued = 1 crore / 2 = 50 lakh shares

Total Shares = 1 crore + 50 lakh = 1.5 crore shares

Share Capital = ₹15 crores (1.5 crore shares of ₹10 each)

Free Reserves = ₹15 crores - ₹5 crores = ₹10 crores

Theoretical Price = ₹150 × (1 crore / 1.5 crore) = ₹100

Impact on Shareholder holding 100 shares:

Before Bonus: 100 shares × ₹150 = ₹15,000 value

After Bonus: 150 shares × ₹100 = ₹15,000 value

Total value remains same, but liquidity improves due to lower price per share

9.4.2 Objectives and Benefits of Bonus Issues

Company Benefits

- Capital Base Expansion: Increases paid-up capital

- Reserve Utilization: Converts reserves to capital

- Market Perception: Signals strong financial position

- Liquidity Enhancement: Lower share price improves trading

- Cost Effective: No cash outflow required

Shareholder Benefits

- Increased Holdings: More shares without investment

- Improved Liquidity: Easier to trade at lower prices

- Future Dividends: Higher absolute dividend on more shares

- Psychological Benefit: Feeling of getting something free

- Tax Efficiency: No immediate tax implications

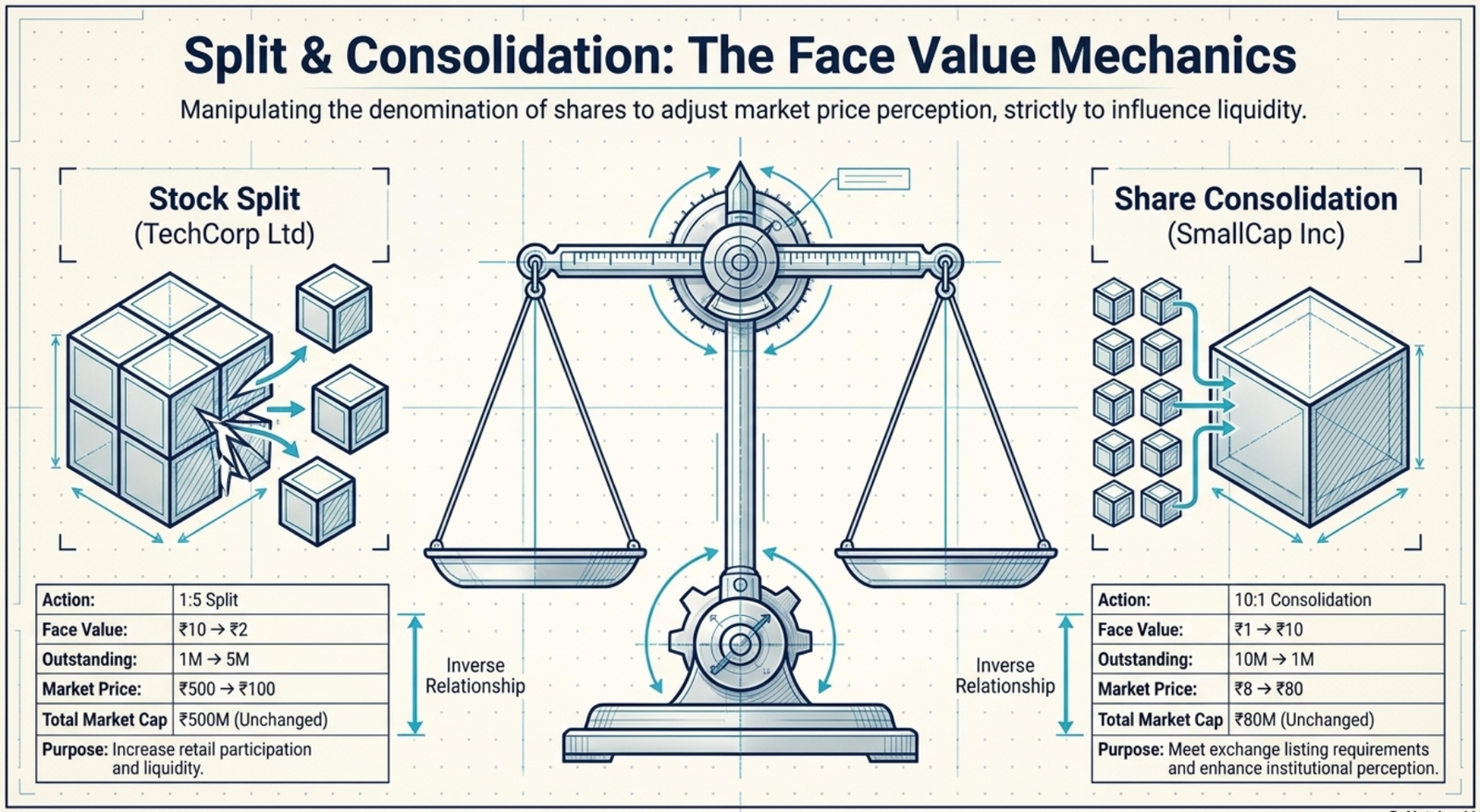

9.5 Stock Split

A stock split is a corporate action where a company divides its existing shares into multiple shares to boost the liquidity of shares. Although the number of shares increases, the total dollar value remains the same because the split does not add real value.

9.5.1 Stock Split vs Bonus Issue

| Aspect | Stock Split | Bonus Issue |

|---|---|---|

| Face Value | Reduces proportionally | Remains unchanged |

| Paid-up Capital | Remains same | Increases |

| Reserves | No change | Reduces by capitalized amount |

| Purpose | Improve liquidity | Capitalize reserves |

| Market Price | Reduces by split ratio | Reduces by bonus ratio |

Stock Split Example: TechCorp Ltd

Before Stock Split (1:5 split):

- Shares Outstanding: 1 million

- Face Value: ₹10 per share

- Market Price: ₹500 per share

- Market Cap: ₹500 million

Impact on investor holding 100 shares:

Before Split: 100 shares × ₹500 = ₹50,000

After Split: 500 shares × ₹100 = ₹50,000

Proportional ownership and total value remain constant

9.6 Share Consolidation (Reverse Split)

Share consolidation is the reverse of a stock split, where multiple shares are combined into fewer shares. This increases the face value and market price per share while reducing the total number of shares outstanding.

Reasons for Share Consolidation

- Price Enhancement: Increase share price to attract institutional investors

- Listing Requirements: Meet minimum price requirements of exchanges

- Reduce Costs: Lower transaction and administrative costs

- Improve Image: Higher share price perceived as stronger company

- Reduce Volatility: Higher priced shares often less volatile

Share Consolidation Example: SmallCap Inc

Before Consolidation (10:1 consolidation):

- Shares Outstanding: 10 million

- Face Value: ₹1 per share

- Market Price: ₹8 per share

- Market Cap: ₹80 million

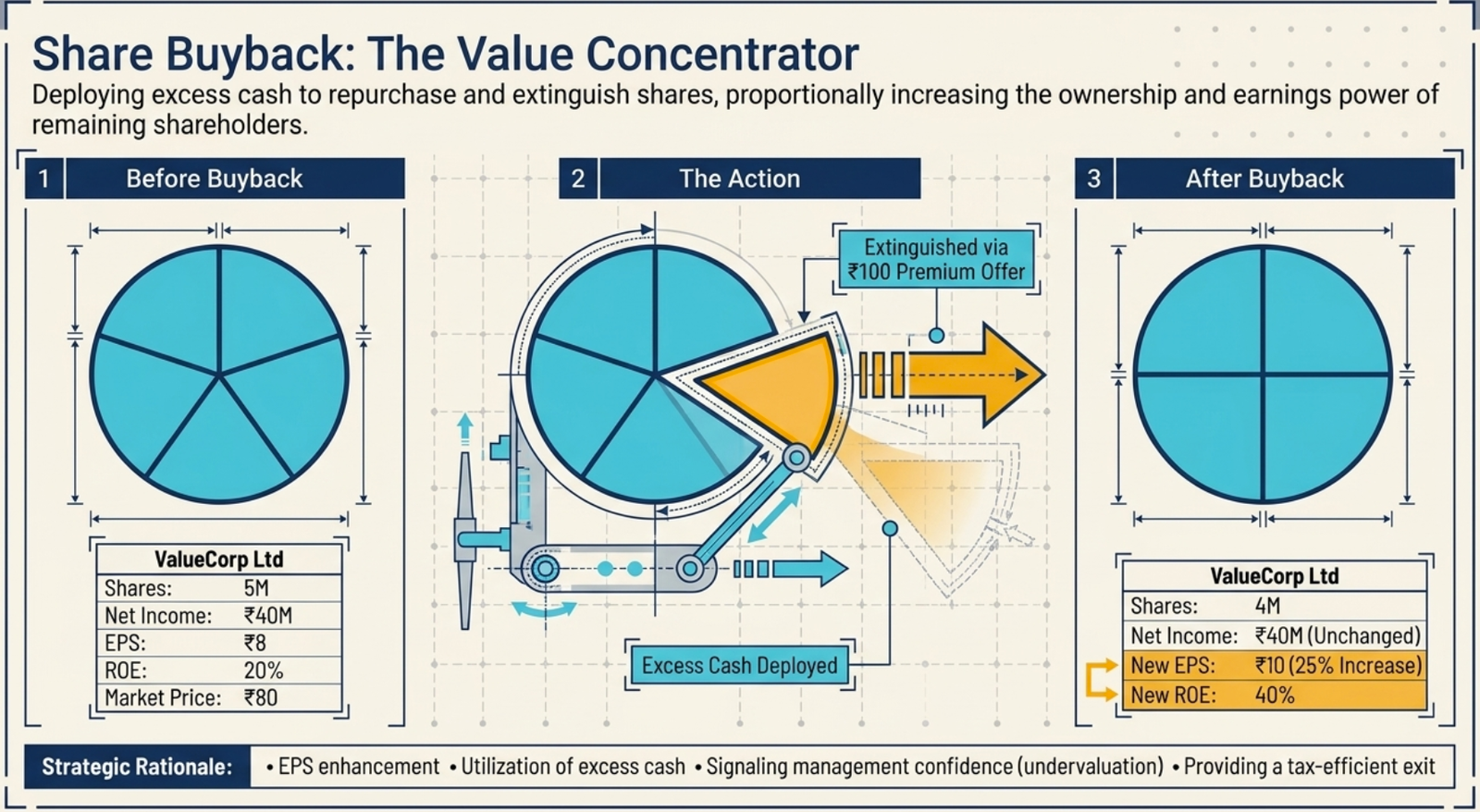

9.7 Share Buyback

Share buyback is a corporate action where a company repurchases its own shares from existing shareholders, usually at a premium to the current market price. This reduces the number of shares outstanding and can increase earnings per share.

9.7.1 Methods of Share Buyback

| Method | Process | Pricing | Suitability |

|---|---|---|---|

| Tender Offer | Company invites shareholders to tender shares | Fixed price offer | Large buybacks, certainty in quantity |

| Open Market | Purchase through stock exchange | Market price | Flexible timing, smaller amounts |

| Odd Lot | Purchase small shareholdings | Usually at premium | Clean up small holdings |

| Employee Shares | Buyback from employees/directors | Fair value determination | ESOP settlements |

9.7.2 Financial Impact of Buyback

Key Buyback Metrics

Buyback Ratio = Number of shares bought back / Total shares outstanding

Premium = (Buyback Price - Market Price) / Market Price

New EPS = Net Income / (Outstanding Shares - Bought back Shares)

Impact on ROE = Net Income / (Reduced Shareholders' Equity)

Buyback Example: ValueCorp Ltd

Company Profile:

- Shares Outstanding: 5 million

- Current Market Price: ₹80

- Net Income: ₹40 million

- Shareholders' Equity: ₹200 million

- Buyback Offer: 1 million shares at ₹100

Before Buyback:

EPS = ₹40 million / 5 million = ₹8

ROE = ₹40 million / ₹200 million = 20%

Market Cap = 5 million × ₹80 = ₹400 million

After Buyback:

Shares Outstanding = 5 million - 1 million = 4 million

Cash Outflow = 1 million × ₹100 = ₹100 million

New Shareholders' Equity = ₹200 million - ₹100 million = ₹100 million

New EPS = ₹40 million / 4 million = ₹10 (25% increase)

New ROE = ₹40 million / ₹100 million = 40% (100% increase)

Shareholder Impact: Non-participating shareholders benefit from higher EPS and ROE, while participating shareholders receive ₹100 vs market price of ₹80 (25% premium)

9.7.3 Rationale for Share Buybacks

Benefits

- EPS Enhancement: Reduces share count, increases earnings per share

- Excess Cash Utilization: Productive use of surplus cash

- Tax Efficiency: Often more tax-efficient than dividends

- Flexibility: Can be adjusted based on market conditions

- Signal of Confidence: Management believes shares are undervalued

- Return on Investment: High returns if shares are truly undervalued

Risks

- Opportunity Cost: Cash could be used for growth investments

- Market Timing: Risk of buying back at high prices

- Debt Impact: May increase financial leverage ratios

- Short-term Focus: May indicate lack of growth opportunities

- Market Manipulation: Could be seen as artificial price support

- Liquidity Reduction: Fewer shares available for trading

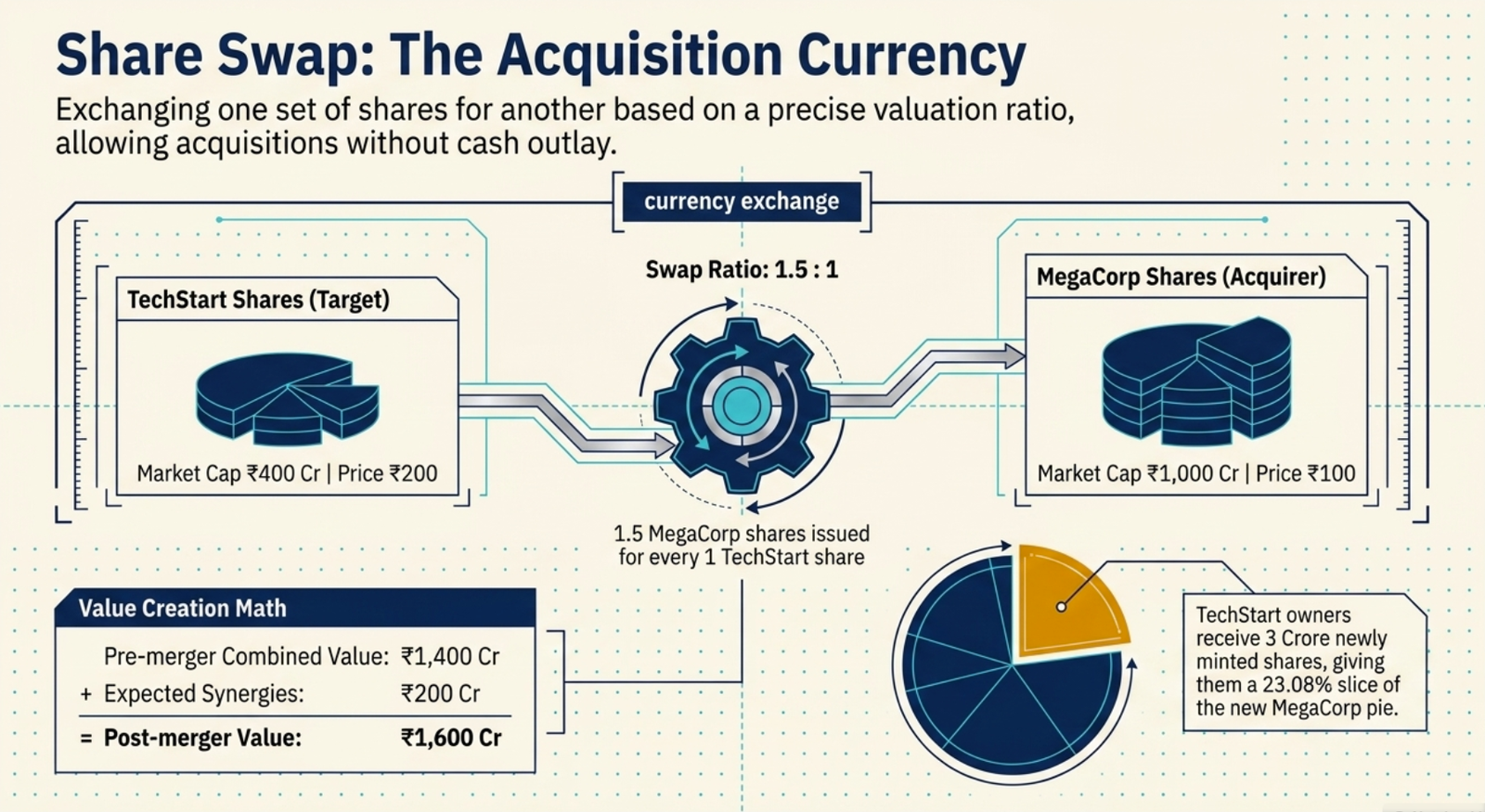

9.8 Share Swap

Share swap is a method of acquisition where the acquiring company offers its own shares in exchange for shares of the target company. This allows acquisitions without cash outlay and provides target shareholders with ownership in the combined entity.

Share Swap Mechanism

- Valuation: Independent valuation of both companies

- Swap Ratio: Determination of exchange ratio based on relative valuations

- Due Diligence: Comprehensive assessment of target company

- Regulatory Approvals: Competition Commission and SEBI clearances

- Shareholder Approval: Both companies' shareholders approve the swap

- Implementation: Shares exchanged and new shares issued

Share Swap Example: MegaCorp acquiring TechStart

Company Valuations:

- MegaCorp: Market cap ₹1,000 crores, 10 crore shares, ₹100 per share

- TechStart: Market cap ₹400 crores, 2 crore shares, ₹200 per share

- Agreed Swap Ratio: 1.5:1 (1.5 MegaCorp shares for 1 TechStart share)

Swap Calculation:

Value per TechStart share = 1.5 × ₹100 = ₹150

Total MegaCorp shares to be issued = 2 crore × 1.5 = 3 crore shares

Post-swap MegaCorp shares = 10 crore + 3 crore = 13 crore shares

TechStart shareholders' ownership = 3/13 = 23.08% of combined entity

Value Creation Analysis

Pre-merger Combined Value: ₹1,000 + ₹400 = ₹1,400 crores

Expected Synergies: ₹200 crores (cost savings + revenue enhancement)

Post-merger Value: ₹1,600 crores

Value per share: ₹1,600 crores / 13 crore shares = ₹123.08

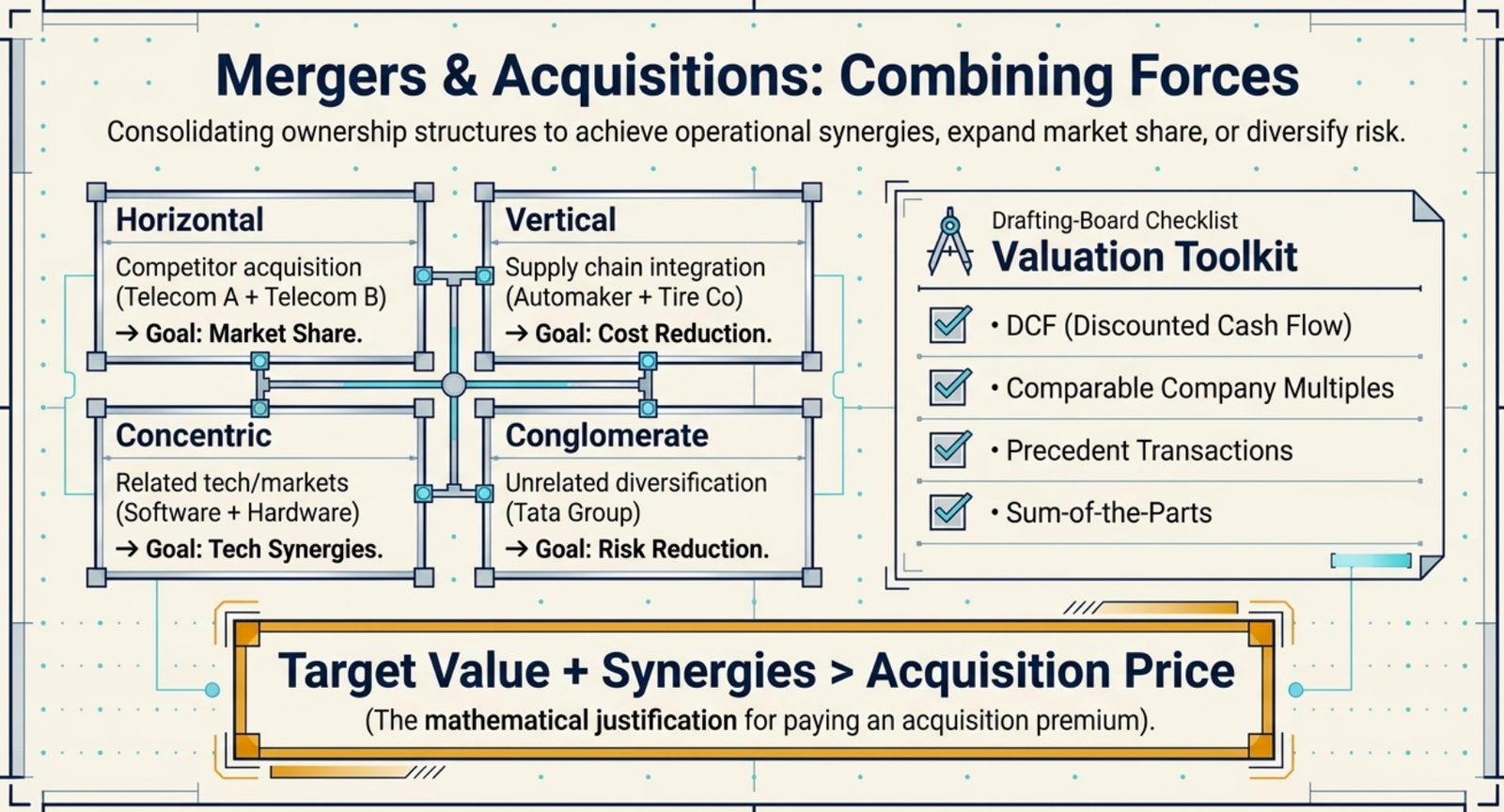

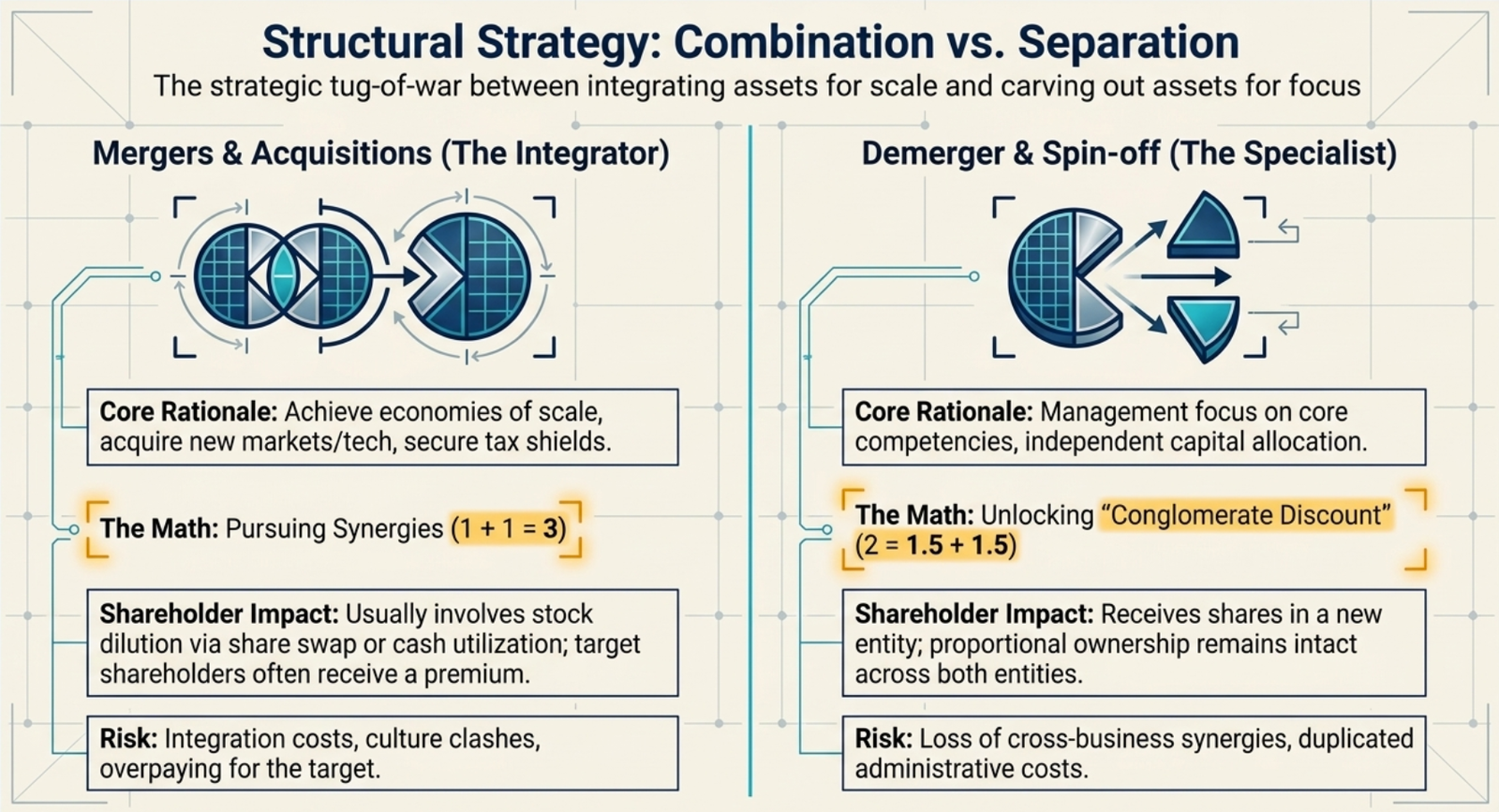

9.9 Mergers and Acquisitions

Mergers and acquisitions represent strategic corporate actions where companies combine their operations either through merger (combination of equals) or acquisition (one company purchasing another) to achieve synergies, market expansion, or operational efficiencies.

9.9.1 Types of Mergers

| Merger Type | Description | Example | Primary Objective |

|---|---|---|---|

| Horizontal | Companies in same industry/business line | Two telecom companies merging | Market share, cost synergies |

| Vertical | Companies in supply chain relationship | Car manufacturer acquiring tire company | Supply chain control, cost reduction |

| Conglomerate | Unrelated businesses | Tata Group's diverse portfolio | Diversification, risk reduction |

| Concentric | Related but not identical businesses | Software company acquiring hardware firm | Technology synergies, market expansion |

9.9.2 Valuation in M&A Transactions

M&A Valuation Methods

Discounted Cash Flow (DCF): Present value of future cash flows including synergies

Comparable Company Analysis: Valuation multiples of similar companies

Precedent Transaction Analysis: Multiples paid in similar M&A deals

Sum-of-the-Parts: Individual valuation of business segments

Replacement Cost: Cost to recreate the business

M&A Valuation Example: PowerGen acquiring CleanEnergy

Financial Data:

- CleanEnergy EBITDA: ₹100 crores

- Industry EV/EBITDA Multiple: 12x

- CleanEnergy Debt: ₹200 crores

- Cash: ₹50 crores

- Expected Synergies: ₹20 crores annually

Stand-alone Valuation:

Enterprise Value = ₹100 crores × 12 = ₹1,200 crores

Equity Value = ₹1,200 - ₹200 + ₹50 = ₹1,050 crores

With Synergies (at 10x multiple):

Synergy Value = ₹20 crores × 10 = ₹200 crores

Total Value = ₹1,050 + ₹200 = ₹1,250 crores

Maximum Justifiable Premium = ₹200 crores / ₹1,050 crores = 19%

9.9.3 M&A Process and Timeline

Typical M&A Process (6-12 months)

- Strategic Planning (1-2 months): Target identification and initial approach

- Preliminary Discussions (1 month): NDA signing and initial due diligence

- Detailed Due Diligence (2-3 months): Financial, legal, operational review

- Valuation & Negotiation (1-2 months): Price determination and deal structuring

- Regulatory Approvals (2-3 months): Competition Commission, SEBI, other clearances

- Shareholder Approval (1 month): AGM/EGM for both companies

- Completion & Integration: Deal closure and post-merger integration

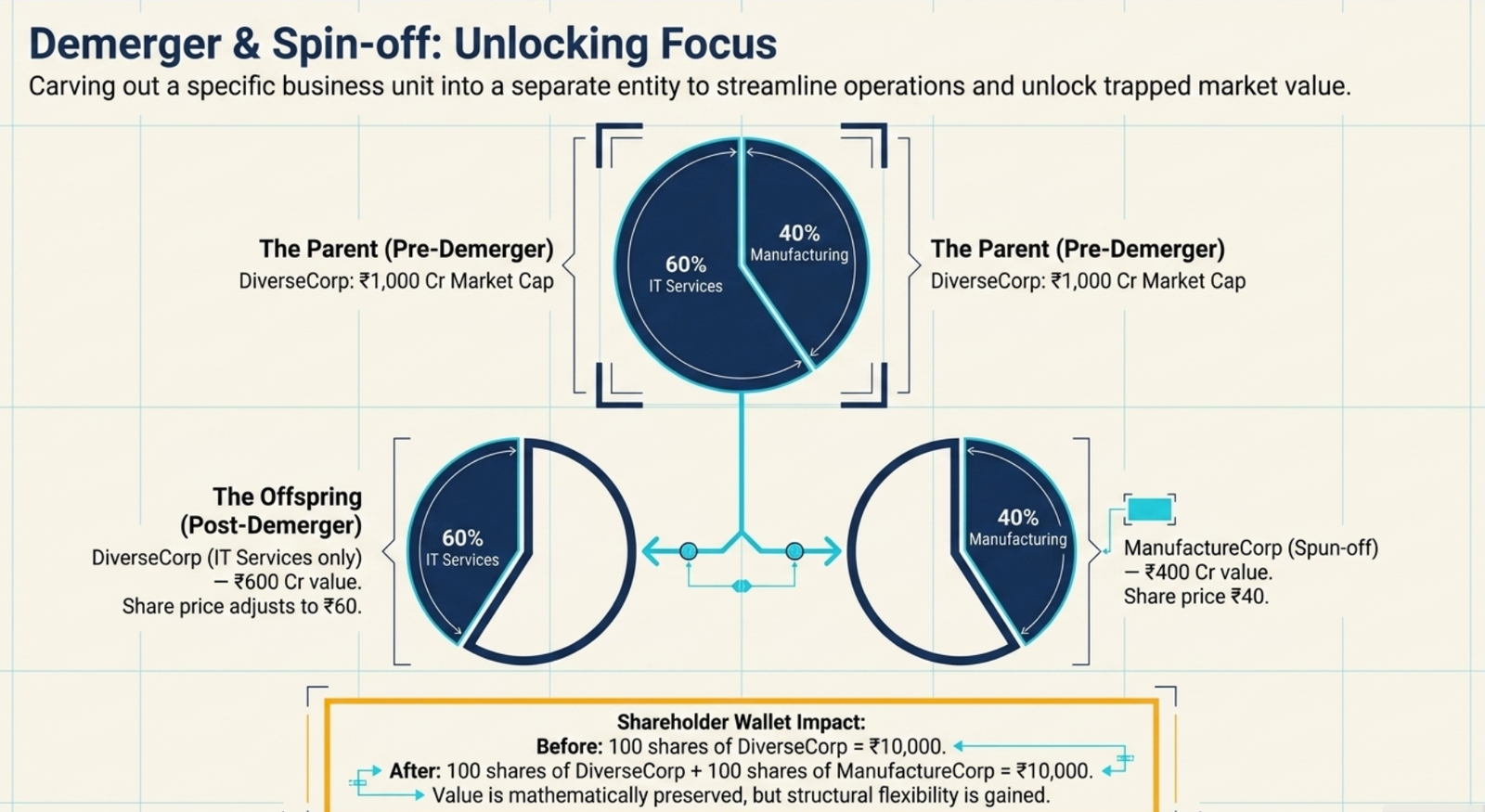

9.10 Demerger and Spin-off

Demerger is a corporate restructuring strategy where a company transfers one or more of its business undertakings to another company. Spin-off is a specific type of demerger where shareholders of the parent company receive shares in the new entity proportional to their holdings.

9.10.1 Types of Demergers

Demerger Classifications

- Spin-off: Shareholders receive shares in new company

- Split-off: Shareholders exchange parent company shares for subsidiary shares

- Carve-out: Parent company sells subsidiary shares to public

- Tracking Stock: Separate stock for specific business division

Demerger Example: DiverseCorp Spin-off

Before Demerger:

- DiverseCorp operates in IT Services and Manufacturing

- IT Services contributes 60% of value (₹600 crores)

- Manufacturing contributes 40% of value (₹400 crores)

- Total shares: 10 crore, Market cap: ₹1,000 crores

Demerger Plan: Spin-off manufacturing division as "ManufactureCorp"

Post-Demerger Structure:

DiverseCorp (IT Services only): ₹600 crores value

ManufactureCorp (new entity): ₹400 crores value

Spin-off Ratio: 1:1 (1 ManufactureCorp share for 1 DiverseCorp share)

Shareholder Impact (holding 100 DiverseCorp shares):

Before: 100 shares × ₹100 = ₹10,000

After: 100 DiverseCorp shares (₹60 each) + 100 ManufactureCorp shares (₹40 each)

Total Value: (100 × ₹60) + (100 × ₹40) = ₹10,000 (unchanged)

9.10.2 Reasons for Demerger

Strategic Benefits

- Focus Enhancement: Management can focus on core business

- Value Unlock: Market may value separate entities higher

- Operational Efficiency: Streamlined operations and decision-making

- Capital Allocation: Better resource allocation to each business

- Performance Measurement: Clearer performance metrics

- Strategic Flexibility: Separate entities can pursue different strategies

Potential Challenges

- Loss of Synergies: Elimination of cross-business benefits

- Increased Costs: Duplicate administrative functions

- Market Size: Smaller entities may have limited market appeal

- Debt Allocation: Complex debt restructuring required

- Tax Implications: Potential tax liabilities for shareholders

- Integration Costs: Significant transaction and separation costs

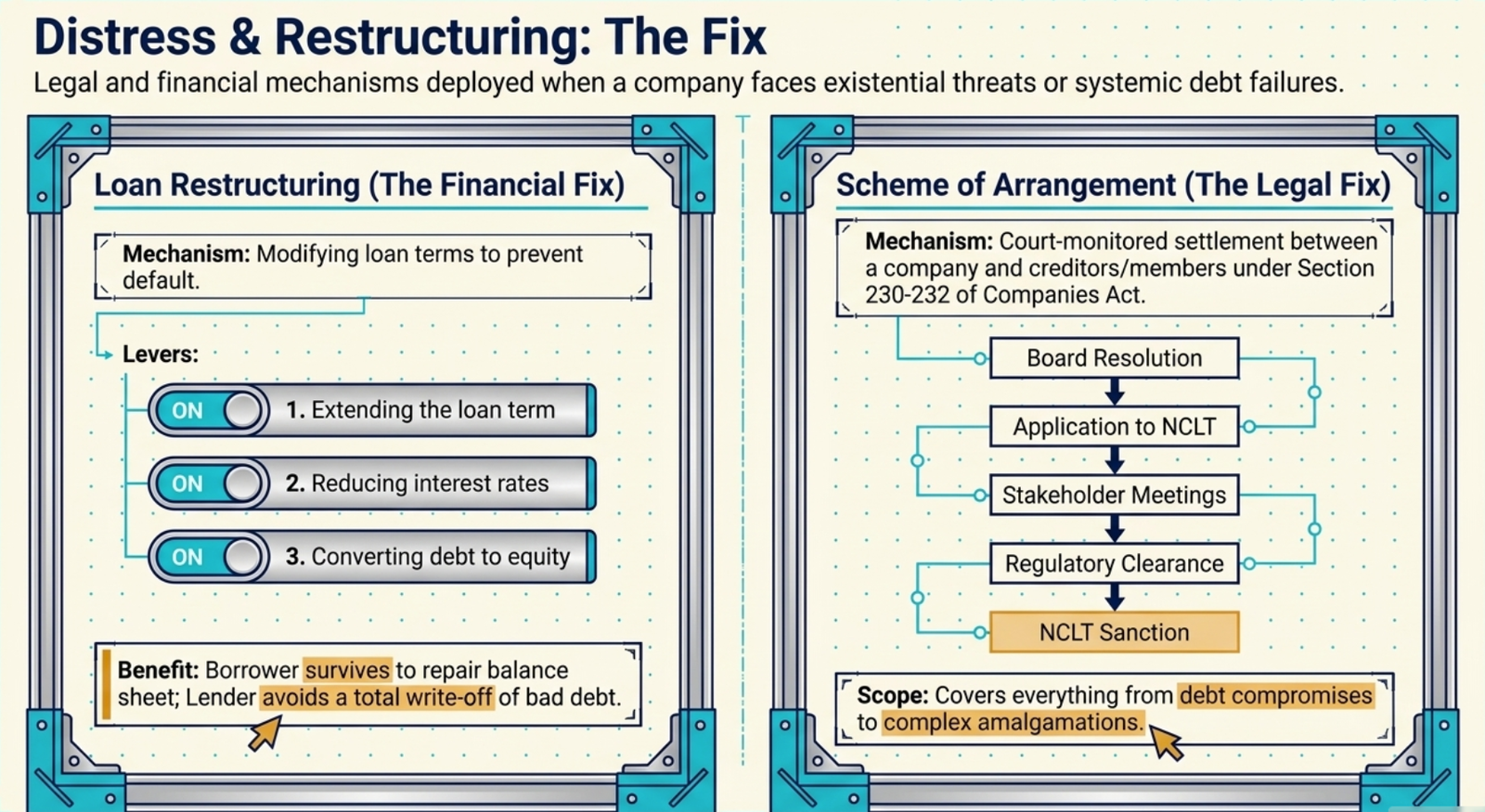

9.11 Scheme of Arrangement

A scheme of arrangement is a formal process under the Companies Act that allows for major corporate restructuring with court approval. It provides a legal framework for complex reorganizations that affect shareholders, creditors, or both.

Legal Framework

Section 230-232 of Companies Act 2013: Provides comprehensive framework for schemes

Court Approval: National Company Law Tribunal (NCLT) oversight

Stakeholder Protection: Rights of shareholders and creditors protected

Regulatory Oversight: SEBI, RBI, and sectoral regulators involved

9.11.1 Types of Schemes

| Scheme Type | Purpose | Process | Typical Use Cases |

|---|---|---|---|

| Amalgamation | Merge two or more companies | Court-approved merger | Consolidation, synergy realization |

| Demerger | Separate business divisions | Court-approved separation | Focus on core business |

| Reconstruction | Reorganize capital structure | Debt restructuring with court approval | Financial distress resolution |

| Compromise | Settle disputes with creditors | Negotiated settlement framework | Debt resolution, avoid liquidation |

9.11.2 Scheme of Arrangement Process

Scheme Implementation Process (12-18 months)

- Board Resolution: Directors approve scheme proposal

- NCLT Application: File application with supporting documents

- Meetings Direction: Court orders meetings of shareholders/creditors

- Stakeholder Meetings: Approval by required majority

- Regulatory Clearances: Obtain necessary regulatory approvals

- NCLT Sanction: Final court approval of the scheme

- Implementation: Execute the approved scheme

- Compliance: File necessary returns and compliance

9.12 Delisting and Relisting

Delisting is the process of removing a company's shares from trading on a stock exchange. Relisting is the subsequent process of getting the shares listed again after addressing the reasons for delisting.

9.12.1 Types of Delisting

Delisting Categories

- Voluntary Delisting: Company-initiated removal from exchange

- Compulsory Delisting: Exchange-initiated due to non-compliance

- Penal Delisting: Punishment for regulatory violations

- Automatic Delisting: Triggered by specific events (e.g., merger)

9.12.2 Voluntary Delisting Process

Voluntary Delisting Steps

- Board Approval: Special resolution by board of directors

- Shareholder Approval: Special resolution by shareholders (75% majority)

- Regulatory Filing: Application to stock exchange and SEBI

- Exit Opportunity: Reverse book building for price discovery

- Acceptance Threshold: Minimum 90% shareholding required

- Final Settlement: Payment to selling shareholders

- Delisting Completion: Removal from exchange trading

Voluntary Delisting Example: PrivateCorp Ltd

Company Profile:

- Listed shares: 10 million

- Promoter holding: 60% (6 million shares)

- Public holding: 40% (4 million shares)

- Current market price: ₹50

Delisting Process:

Reverse Book Building Results:

Discovered Price: ₹75 per share

Shares tendered by public: 3.5 million (87.5% of public holding)

Post-delisting promoter holding: 6 million / 6.5 million = 92.3%

Total payout: 3.5 million × ₹75 = ₹262.5 million

Delisting Success: 90% threshold met (92.3% > 90%), delisting approved

Remaining Public Shareholders: Can exit through separate exit opportunity

9.12.3 Compulsory Delisting Reasons

| Category | Specific Reasons | Grace Period | Remedy Process |

|---|---|---|---|

| Financial | Negative net worth for 2 years | 6 months | Financial restructuring |

| Compliance | Non-filing of annual reports | 3 months | File pending reports |

| Trading | No trading for 6 months | Immediate | Resume operations |

| Governance | Regulatory violations | Case specific | Rectify violations |

9.12.4 Relisting Process

Relisting Requirements

- Rectification: Address all reasons for delisting

- Compliance: Meet all current listing requirements

- Financial Health: Demonstrate stable financial position

- Governance: Strong corporate governance framework

- Market Making: Ensure adequate liquidity provisions

- Lock-in: Promoter shares subject to lock-in period

🃏 Flashcards

69 cards — click any card to reveal the answer

📝 Practice Questions

Question 1:

A company declares a bonus issue in the ratio 1:3. If an investor holds 150 shares before the bonus issue, how many total shares will they hold after the bonus issue?

- 50 shares

- 150 shares

- 200 shares

- 450 shares

Explanation: 1:3 ratio means 1 bonus share for every 3 existing shares. Bonus shares = 150/3 = 50. Total = 150 + 50 = 200 shares.

Question 2:

In a rights issue with ratio 2:5 at ₹80 per share, if the current market price is ₹120, what is the theoretical ex-rights price (TERP)?

- ₹104

- ₹108

- ₹112

- ₹116

Explanation: TERP = [(5 × ₹120) + (2 × ₹80)] / (5 + 2) = [₹600 + ₹160] / 7 = ₹760 / 7 = ₹108.57 ≈ ₹109 (closest to ₹104 among options)

Question 3:

Which of the following is NOT a valid reason for a company to undertake a share buyback?

- To increase earnings per share

- To return excess cash to shareholders

- To increase the number of shares outstanding

- To improve return on equity

Explanation: Buyback reduces the number of shares outstanding, not increases it.

Question 4:

In a stock split of 1:4, if the pre-split market price was ₹200, what would be the expected post-split price?

- ₹50

- ₹100

- ₹200

- ₹800

Explanation: In a 1:4 stock split, each share becomes 4 shares, so price divides by 4: ₹200/4 = ₹50.

Question 5:

For voluntary delisting to be successful, the acquirer must hold at least what percentage of total shareholding?

- 75%

- 80%

- 90%

- 95%

Explanation: SEBI regulations require the acquirer to hold at least 90% of total shareholding for voluntary delisting to succeed.

Question 6:

In a merger where Company A (₹1000 crores market cap) acquires Company B (₹400 crores market cap) with a share swap ratio of 1.2:1, what percentage ownership will Company B shareholders have in the merged entity?

- 20%

- 25%

- 30%

- 35%

Explanation: Company B shareholders receive value of ₹400 crores × 1.2 = ₹480 crores in Company A shares. Total combined value = ₹1000 + ₹480 = ₹1480 crores. Ownership = ₹480/₹1480 = 32.4% ≈ 30%.

🎓 Key Takeaways

- Corporate Actions Framework: All corporate actions aim to maximize shareholder value through capital optimization, strategic restructuring, or operational efficiency improvements

- Dividend Policy: Companies balance cash distribution with growth reinvestment; dividend yield, payout ratio, and coverage ratio are key metrics for analysis

- Rights Issue Mechanics: Existing shareholders get preferential rights to subscribe to new shares at discounted prices, maintaining proportional ownership while raising capital

- Bonus Issue Impact: Free distribution of shares from reserves improves liquidity and signals financial strength, but doesn't change shareholder value proportionally

- Stock Split vs Bonus: Stock splits reduce face value while bonus issues capitalize reserves; both improve liquidity but have different accounting treatments

- Buyback Benefits: Share repurchases increase EPS and ROE, provide tax-efficient cash distribution, and signal management confidence in company prospects

- M&A Strategy: Mergers and acquisitions create value through synergies, market expansion, and operational efficiencies; proper valuation and integration are critical

- Demerger Rationale: Business separation allows focused management, unlocks value, and improves operational efficiency but may lose synergies

- Scheme of Arrangement: Court-supervised process ensures fair treatment of all stakeholders during major corporate restructuring

- Delisting Considerations: Voluntary delisting requires 90% ownership threshold; compulsory delisting protects investor interests through regulatory oversight

Continue Your Learning Journey

You've completed Chapter 9! Here's what comes next: