Security markets enable investors to deploy their surplus funds in investment instruments that are pre-defined for their features, issued under regulatory supervision, and in most cases liquid in the secondary markets. There are two broad types of securities that are issued by seekers of capital from investors: Equity and Debt.

When a business needs capital to fund its operations and expansion, it makes a choice between these two types of securities.

📑 Chapter Navigation

📖 Complete Course Navigation

Foundation (Ch 1-4)

Analysis (Ch 5-8)

Advanced (Ch 9-13)

Annexures (Ch 14-16)

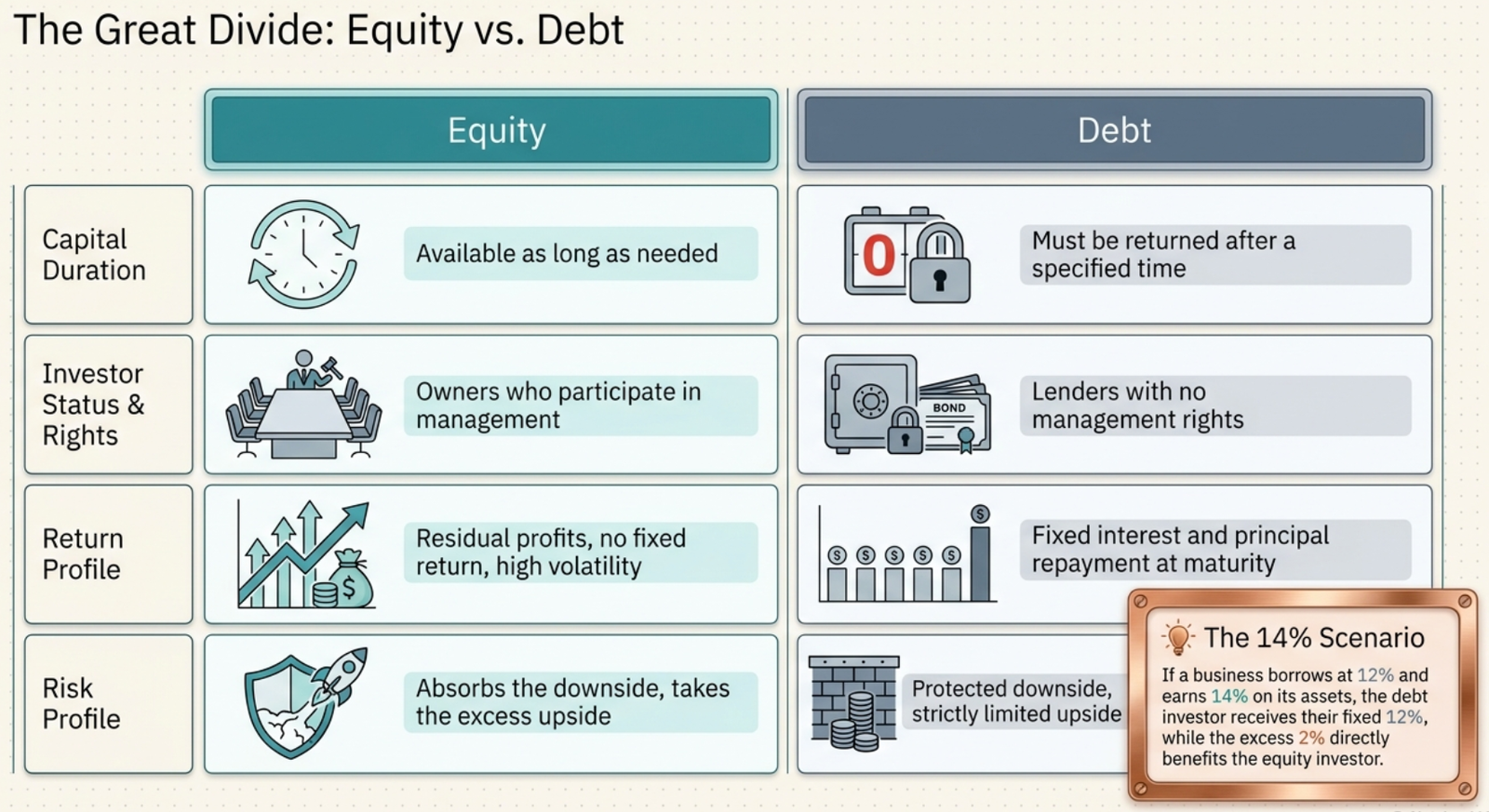

Fundamental Differences: Equity vs Debt

| Aspect | Equity | Debt |

|---|---|---|

| Capital Duration | Available as long as needed | Must be returned after specified time |

| Returns | No fixed return or principal guarantee | Fixed interest rate and principal repayment at maturity |

| Investor Status | Owners of the business | Lenders to the business |

| Management Rights | Participate in management | Do not participate |

| Residual Profits | Belong to equity investors | Limited to fixed coupons and principal |

| Risk Profile | Risky, long-term, growth oriented, high volatility | Lower risk, steady, income-oriented |

| Return Potential | Higher returns possible but uncertain | Steady return but limited upside |

If a business borrows at 12% and earns 14% on assets:

- Debt investor receives only 12% as promised

- Excess 2% benefits equity investor

- If return falls below 12%, equity investor bears the loss

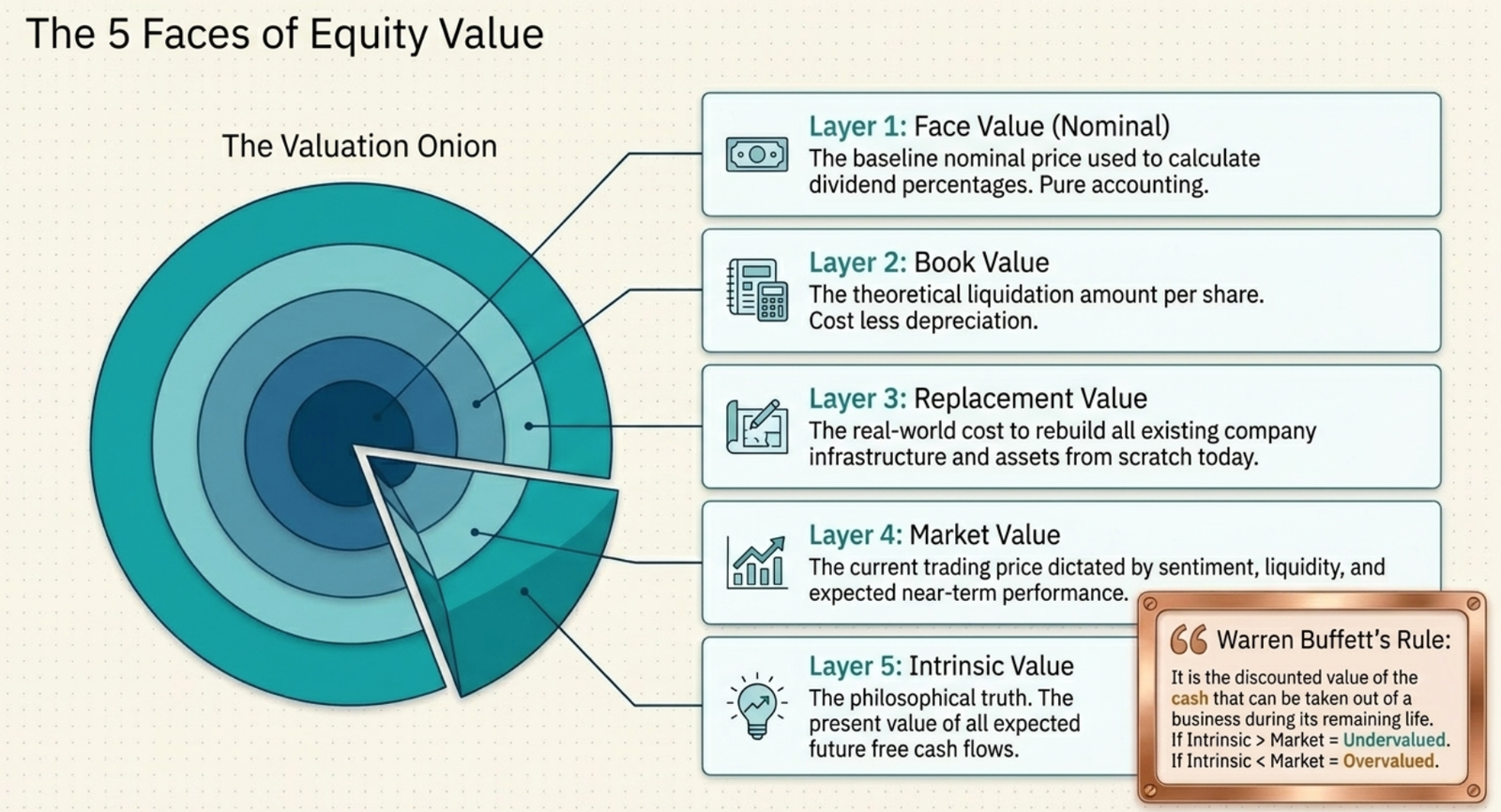

3.1 Terminology in Equity Market

3.1.1 Face Value (FV)

The nominal price of a share is known as its face value. This is a fundamental concept in equity markets.

Shares may be issued:

- At Par: Equal to face value

- At Premium: Higher than face value

- At Discount: Lower than face value

Face Value Changes: Stock Splits and Consolidation

• Before Split: 1 share of Rs. 10 FV

• 1:5 Split: 5 shares of Rs. 2 FV each

• Total value remains same, liquidity increases

Dividend Calculation Based on Face Value

• Company A: Rs. 10 FV, 30% dividend = Rs. 3 per share

• Company B: Rs. 2 FV, 30% dividend = Rs. 0.60 per share

Note: Dividend percentage is always calculated on face value, not market price

3.1.2 Book Value

Book Value represents the net-worth of the company as recorded in its books of accounts.

Net-worth = Share Capital + Reserves and Surplus

3.1.3 Market Value

The current trading price of a share in the stock market.

Factors affecting Market Value:

- Expected company performance

- Market sentiments

- Liquidity conditions

- Economic conditions

- Industry trends

- Regulatory changes

3.1.4 Replacement Value

The current market cost required to recreate all assets of an existing company from scratch.

3.1.5 Intrinsic Value

The present value of expected free cash flows from the asset. This is the cornerstone of value investing.

Warren Buffett's Definition: "It is the discounted value of the cash that can be taken out of a business during its remaining life"

Market Value vs Intrinsic Value Analysis

| Scenario | Relationship | Investment Implication |

|---|---|---|

| Intrinsic Value > Market Value | Undervalued | Potential Buy Opportunity |

| Intrinsic Value < Market Value | Overvalued | Potential Sell Opportunity |

| Intrinsic Value = Market Value | Fairly Valued | Hold Decision |

Equity investing combines quantitative analysis with qualitative factors:

- Quality of management

- Marketing strategies

- Financing capabilities

- Competitive positioning

- Behavioral and cognitive factors of market participants

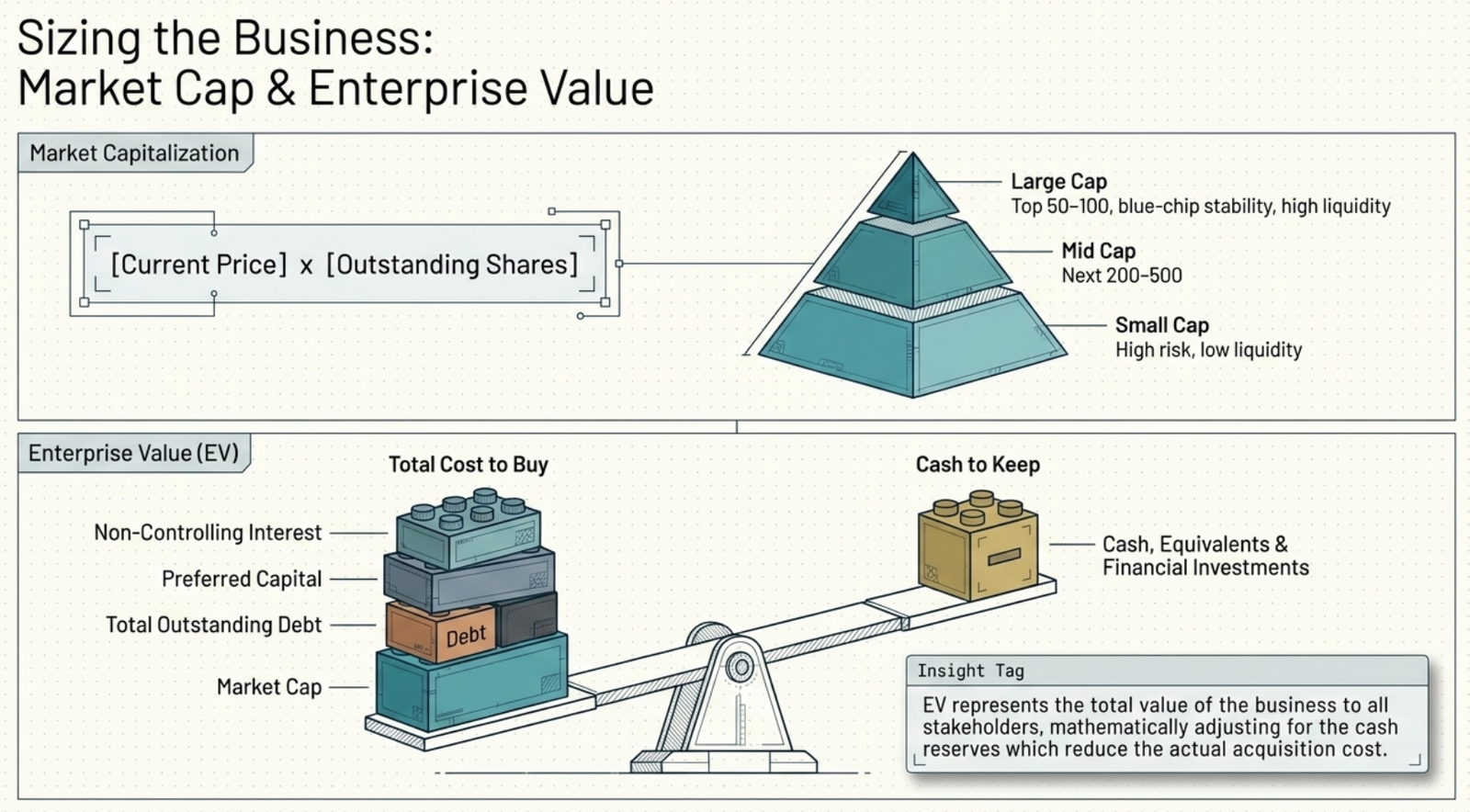

3.1.6 Market Capitalization (Market Cap)

The total value required to buy out an entire company at current market prices.

Market Cap Categories

| Category | Characteristics | Typical Range | Investment Profile |

|---|---|---|---|

| Large Cap/Blue Chip | High liquidity, institutional interest | Top 50-100 companies | Lower risk, stable returns |

| Mid Cap | Good liquidity, medium size | Next 200-500 companies | Moderate risk, growth potential |

| Small Cap | Limited liquidity, smaller size | Remaining companies | Higher risk, high growth potential |

3.1.7 Enterprise Value (EV)

Enterprise Value represents the overall value of the business considering all sources of capital.

Balance Sheet Data:

• Common Equity: Rs. 12.5 crores (10,00,000 shares × Rs. 10 FV)

• Current Market Price: Rs. 340 per share

• Preferred Capital: Rs. 8.5 crores

• Debt Outstanding: Rs. 6.4 crores

• Cash and Equivalents: Rs. 2.5 crores

• Financial Investments: Rs. 1.4 crores

Calculation:

Market Cap = 340 × 10,00,000 = Rs. 34 crores

EV = 34.0 + 8.5 + 6.4 - 2.5 - 1.4 = Rs. 45.0 crores

• Market Cap = Value to equity holders only

• Enterprise Value = Total business value to all capital providers

• EV is preferred for company comparisons and valuations

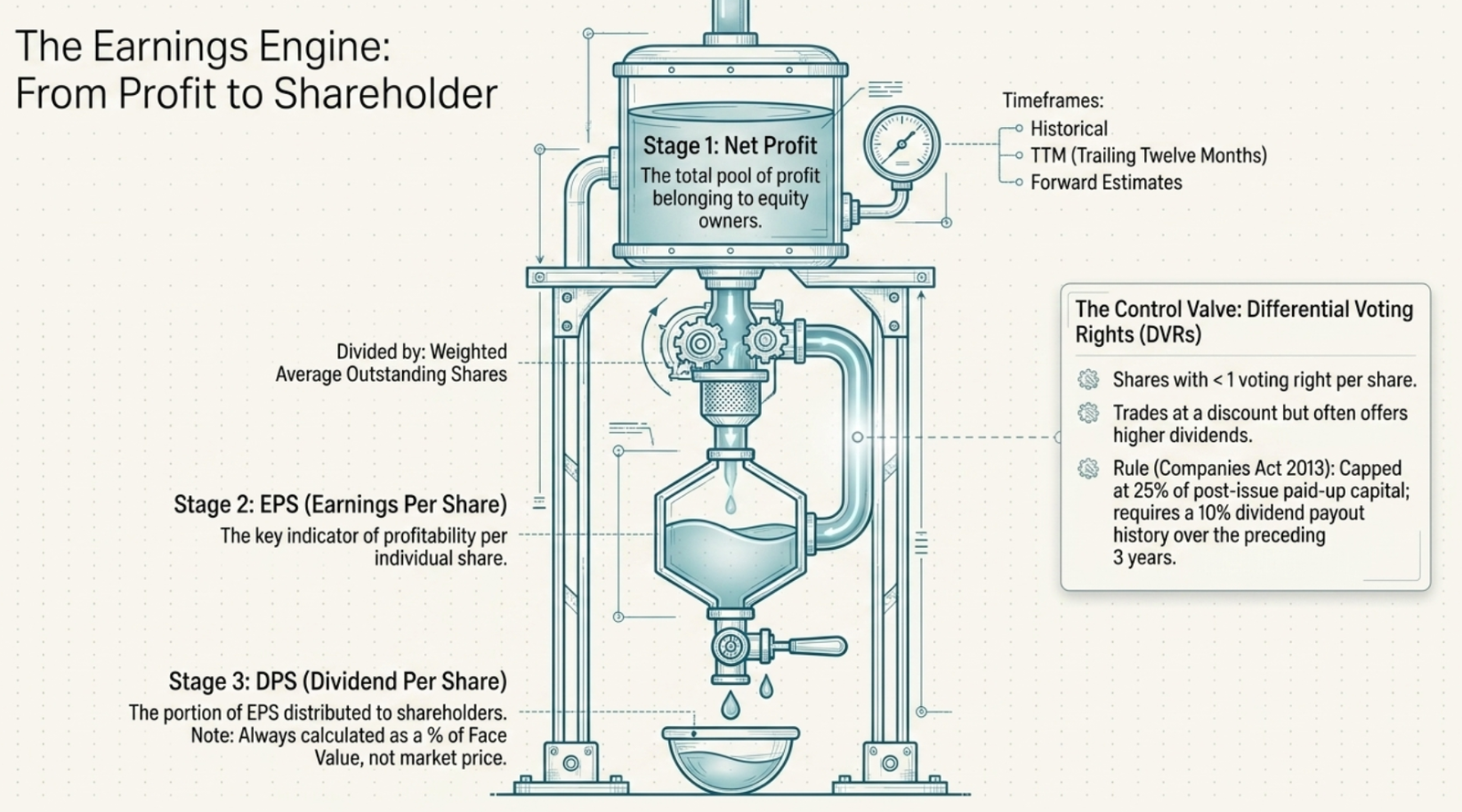

3.1.8 Earnings – Historical, Trailing and Forward

Types of Earnings

| Earnings Type | Definition | Availability |

|---|---|---|

| Net Profits | Profits available to equity owners | Equity holders |

| EBIT | Earnings before Interest and Taxes | Both equity and debt holders |

| EBITDA | Earnings before Interest, Tax, Depreciation, Amortization | Asset replacement and capital providers |

Earnings Time Classifications

- Historical Earnings: Earnings of previous years (already reported)

- Trailing Earnings: Latest four quarters on rolling basis (TTM - Trailing Twelve Months)

- Forward Earnings: Projected future earnings based on estimates

3.1.9 Earnings Per Share (EPS)

Company with Net Profit of Rs. 10 Lakh and 2 Lakh outstanding shares:

EPS = Rs. 10 Lakh ÷ 2 Lakh = Rs. 5 per share

• Higher EPS indicates better profitability per share

• Key variable in determining share price

• Used in PE ratio calculations

• Important for dividend sustainability analysis

3.1.10 Dividend Per Share (DPS)

Dividend is the portion of profits distributed to shareholders, typically declared as a percentage of face value.

Scenario 1: 40% dividend on Rs. 10 face value

DPS = Rs. 10 × 40% = Rs. 4 per share

Scenario 2: Rs. 5 absolute dividend per share

On Rs. 10 face value = 50% dividend

On Rs. 2 face value = 250% dividend

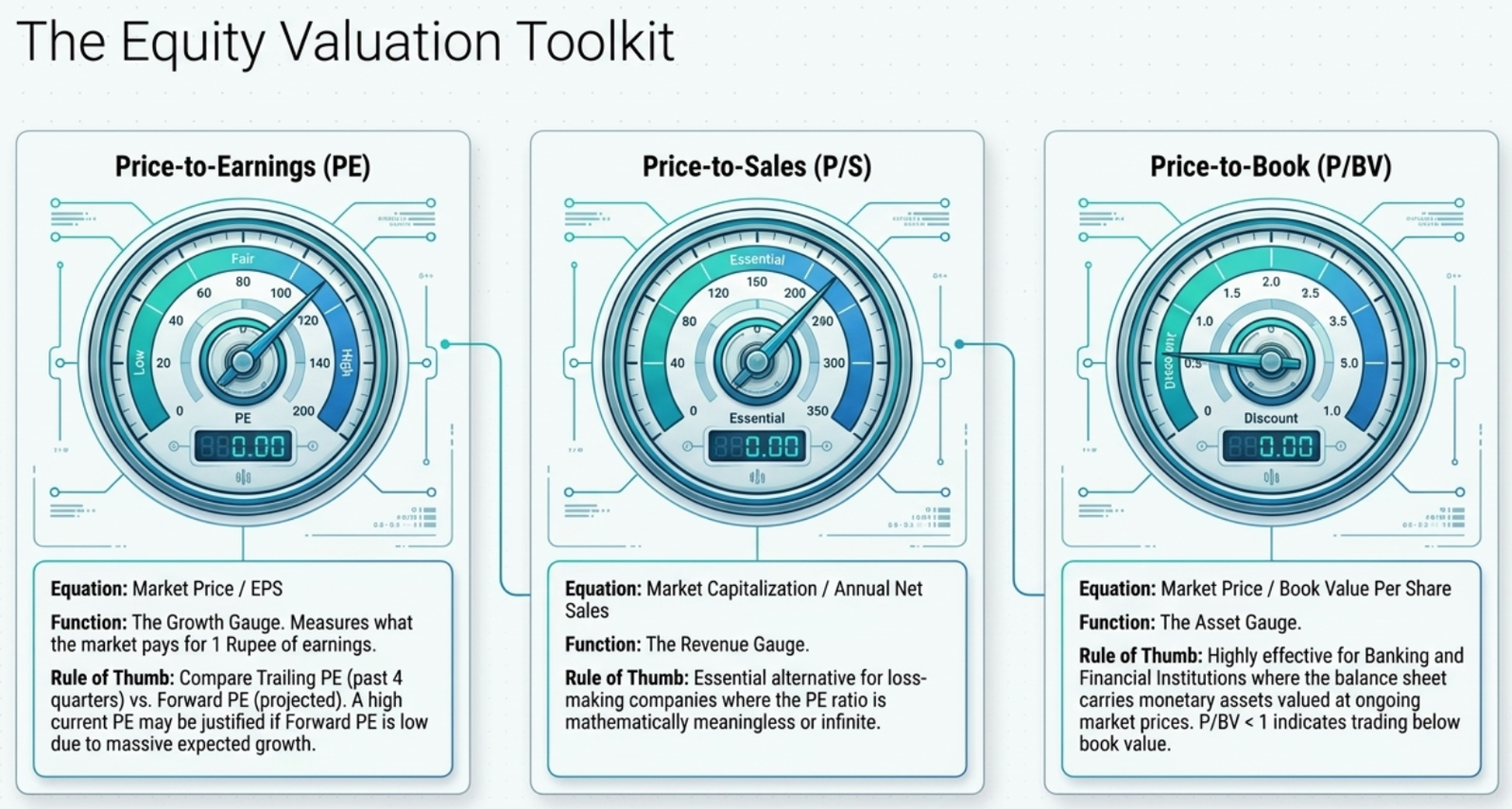

3.1.11 Price to Earnings Ratio (PE Ratio)

PE measures how much the market is willing to pay for each rupee of earnings.

Types of PE Ratios

| PE Type | Based On | Usage | Reliability |

|---|---|---|---|

| Historical PE | Past earnings | Limited value | Lower (stale data) |

| Trailing PE | Last 4 quarters | Current analysis | Moderate |

| Forward PE | Projected earnings | Investment decisions | Higher (forward-looking) |

"XYZ company trades at 20 times 2024 earnings, but only 15 times projected 2025 earnings, given its strong order book."

This indicates expected earnings growth, making the current high PE more justified.

PE Ratio Applications

- Market Valuation: Index PE indicates if market is over/undervalued

- Company Comparison: Relative valuation within sector

- Investment Timing: Value investors prefer low PE periods

- Risk Assessment: Stable companies command higher PE multiples

3.1.12 Price-to-Sales Ratio (P/S)

OR

P/S Ratio = Market Capitalization / Annual Net Sales

• Annual Net Sales: Rs. 1 Crore

• Outstanding Shares: 10 Lakh

• Current Market Price: Rs. 40

Annual Net Sales per Share = Rs. 1 Crore ÷ 10 Lakh = Rs. 10

P/S Ratio = Rs. 40 ÷ Rs. 10 = 4

• Useful for loss-making companies (where PE is meaningless)

• Less volatile than earnings-based ratios

• Good for comparing companies in same industry

• Helpful in revenue-focused business models

3.1.13 Price-to-Book Value Ratio (P/BV)

Book Value per Share = Net-worth / Outstanding Shares

• Equity Capital: Rs. 10 Lakhs

• Reserves & Surplus: Rs. 50 Lakhs

• Outstanding Shares: 6 Lakhs

• Current Market Price: Rs. 20

Net-worth = Rs. 10 Lakhs + Rs. 50 Lakhs = Rs. 60 Lakhs

Book Value per Share = Rs. 60 Lakhs ÷ 6 Lakhs = Rs. 10

P/BV = Rs. 20 ÷ Rs. 10 = 2 times

P/BV Interpretation

| P/BV Range | Interpretation | Caution |

|---|---|---|

| < 1 | Trading below book value | May indicate fundamental problems |

| = 1 | Trading at book value | Consider asset quality |

| > 1 | Premium to book value | Justified by profitability/growth |

• Assets shown at historical cost, not current value

• Not all low P/BV stocks are bargains

• Less relevant for service industries with minimal assets

• More useful for asset-heavy industries like banking

📊 Calculate These Ratios with Live Company Data

You've just learned PE, P/S, P/BV and other valuation ratios. Now calculate them instantly for 71+ companies with real-time data!

⚡ Instant Ratio Calculations

Practice the exact ratios from NISM Chapter 3:

- PE Ratio (Current, Trailing, Forward)

- P/S Ratio with live sales data

- P/BV Ratio with updated book values

- Enterprise Value calculations

🎯 44+ Financial Ratios

Go beyond NISM basics with comprehensive analysis:

- Profitability Ratios (ROE, ROA, ROCE)

- Liquidity Ratios (Current, Quick, Cash)

- Leverage Ratios (Debt-to-Equity, Interest Coverage)

- Activity Ratios (Asset Turnover, Inventory)

Study Tip: Calculate these ratios for different companies and compare with NISM examples to reinforce your learning!

3.1.14 Differential Voting Rights (DVR)

DVR shares carry less than 1 voting right per share, unlike common shares which carry 1 vote per share.

DVR Characteristics

| Aspect | Common Shares | DVR Shares |

|---|---|---|

| Voting Rights | 1 vote per share | < 1 vote per share |

| Dividend Rights | Standard | Same or higher |

| Trading Price | Higher | Discount to common shares |

| Liquidity | Higher | Lower |

Regulatory Framework (Companies Act 2013)

• Company must have paid at least 10% dividend for preceding 3 years

• DVR shares cannot exceed 25% of total post-issue paid-up capital

• Must be listed separately on stock exchanges

• Tata Motors DVR

• Pantaloons DVR (historical)

• Several other companies have issued DVRs for capital raising without diluting control

3.2 Terminology in Debt Market

Debt capital represents funds provided by lenders who expect regular interest payments and principal repayment at maturity.

Debt Capital Creation Methods

| Method | Characteristics | Examples |

|---|---|---|

| Bank/Institution Loans | Single or consortium of lenders | Term loans, working capital loans |

| Debt Securities | Multiple investors, tradeable | Bonds, debentures, notes |

Debt Security Features

- Principal: Amount borrowed

- Coupon: Interest rate

- Maturity: Repayment date

- Security: Asset backing (if any)

Secured vs Unsecured Debt

| Type | Asset Backing | Default Protection | Interest Rate |

|---|---|---|---|

| Secured Debt | Yes | Assets can be sold to repay | Lower |

| Unsecured Debt | No | Only claim on general assets | Higher |

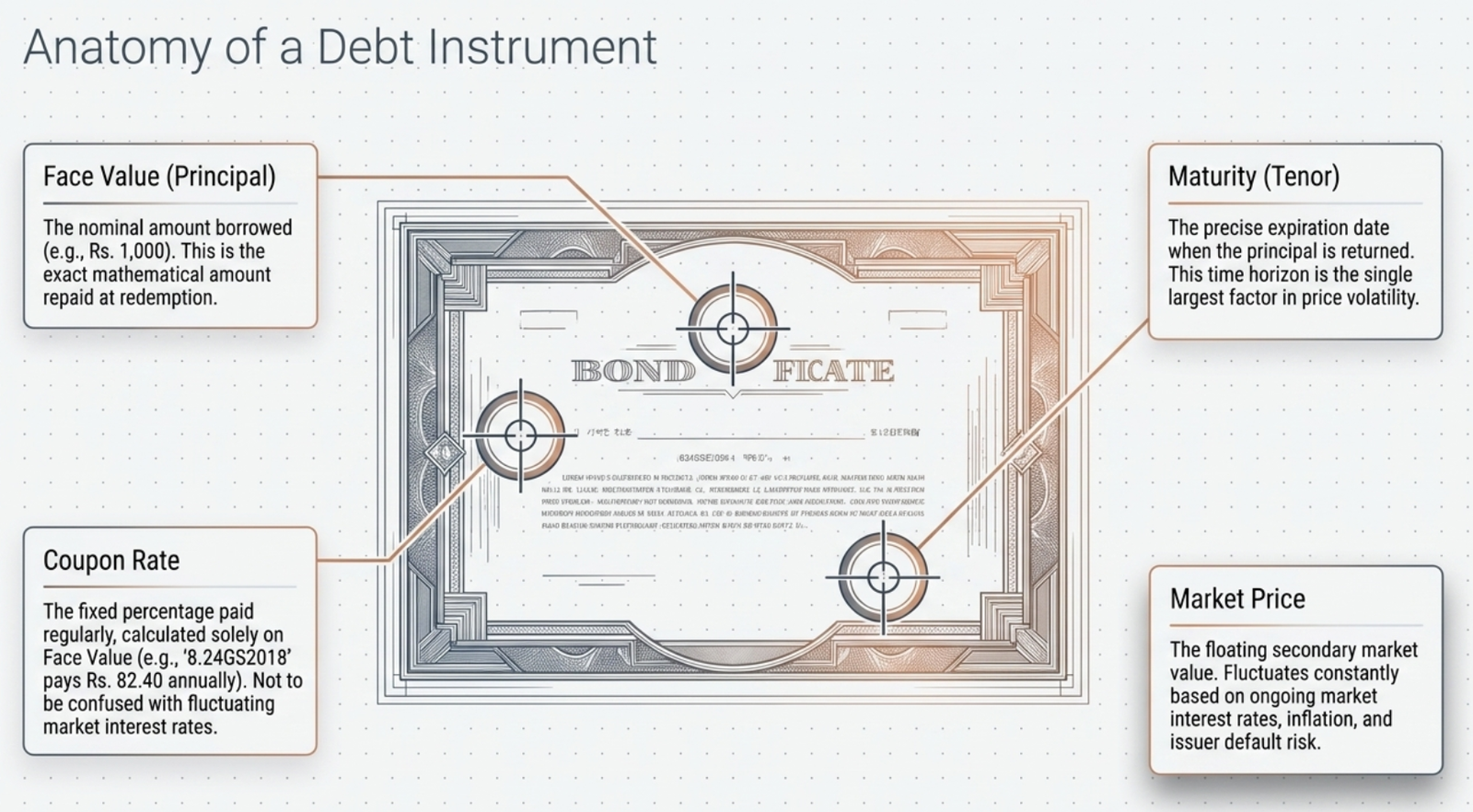

3.2.1 Face Value (Par Value)

The nominal amount of borrowing represented by the debt instrument. Interest is calculated as a percentage of face value.

• Government Securities: Rs. 100, Rs. 1,000

• Corporate Bonds: Rs. 1,000, Rs. 10,000

• Commercial Paper: Rs. 5,00,000 minimum

3.2.2 Coupon Rate

The annual interest rate paid on the face value of the bond.

8.24GS2018 (8.24% Government Security maturing in 2018)

• Face Value: Rs. 1,000

• Annual Coupon: Rs. 1,000 × 8.24% = Rs. 82.40

• Semi-annual Payment: Rs. 82.40 ÷ 2 = Rs. 41.20 every 6 months

3.2.3 Maturity (Tenor)

The time period until the bond expires and principal is repaid.

Maturity Classifications

| Category | Time Period | Examples | Market Segment |

|---|---|---|---|

| Short-term | ≤ 1 year | T-Bills (91, 182, 364 days) | Money Market |

| Medium-term | 1-10 years | Corporate bonds, G-Secs | Bond Market |

| Long-term | > 10 years | Government bonds (up to 30+ years) | Bond Market |

| Perpetual | No maturity | AT1 bonds | Hybrid Market |

3.2.4 Principal

The initial investment amount, represented by face value, which is repaid at maturity regardless of purchase price in secondary market.

• Bond Face Value: Rs. 1,000

• Purchase Price in Secondary Market: Rs. 1,050

• Principal Repaid at Maturity: Rs. 1,000 (not Rs. 1,050)

• Capital Loss: Rs. 50

3.2.5 Redemption of a Bond

The process of bond maturity where the issuer repays principal plus final coupon, terminating the bond contract.

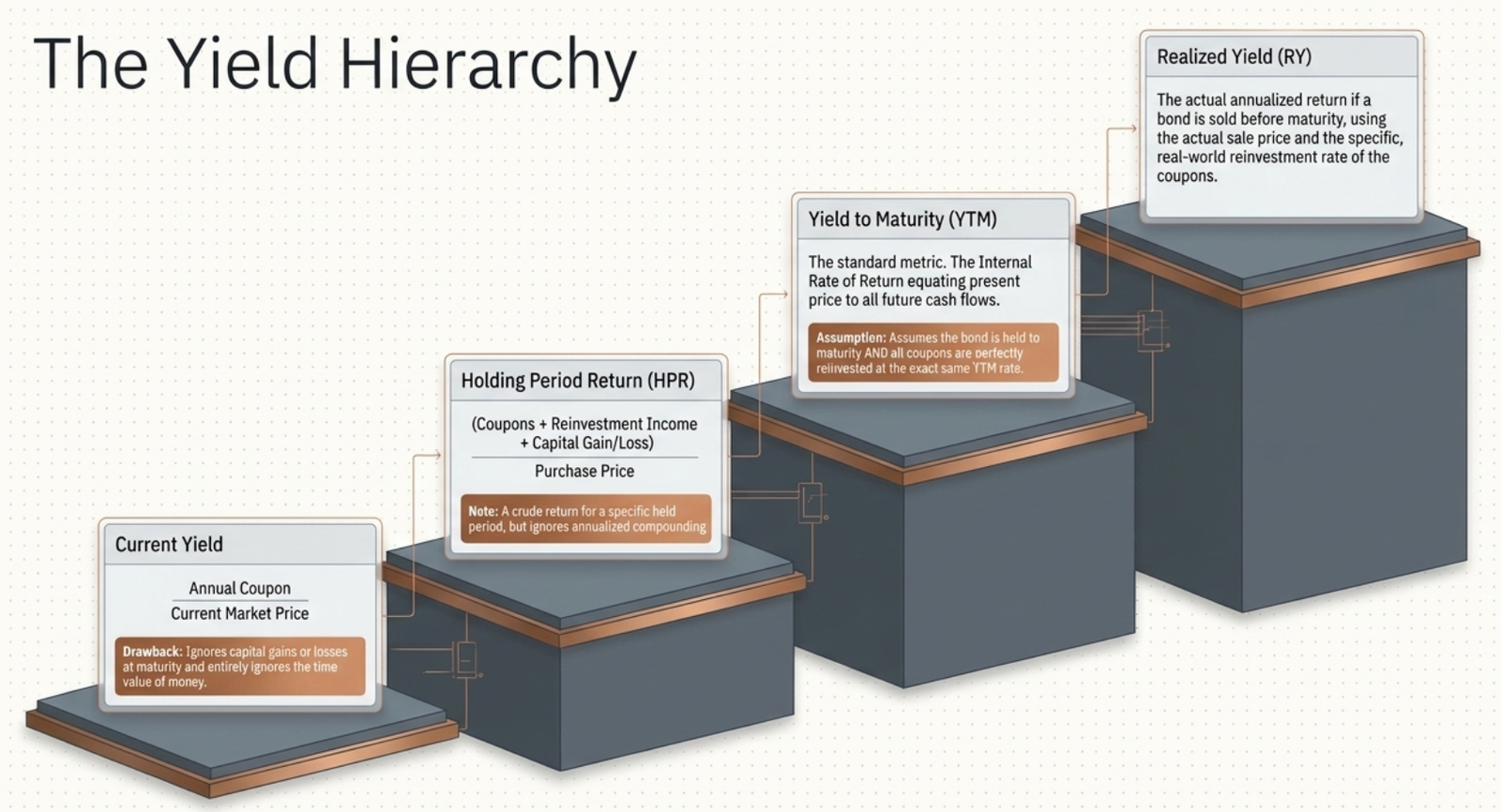

3.2.6 Holding Period Returns (HPR)

Total return earned during the specific period the bond was held by the investor.

• Purchase Price: Rs. 104

• Annual Coupon: Rs. 8

• Reinvestment Rate: 7% for 1 year

• Sale Price: Rs. 110

Coupon Income = Rs. 8

Reinvestment Income = Rs. 8 × 7% = Rs. 0.56

Capital Gain = Rs. 110 - Rs. 104 = Rs. 6

HPR = (8 + 0.56 + 6) / 104 = 14.00%

3.2.7 Current Yield

8.24GS2018 trading at Rs. 104

Current Yield = 8.24 / 104 = 7.92%

• Ignores capital gains/losses at maturity

• Doesn't consider time value of money

• Similar to dividend yield for stocks

• Not widely used for investment decisions

3.2.8 Yield to Maturity (YTM)

The Internal Rate of Return (IRR) of the bond, considering all future cash flows.

(at discount rate = YTM)

YTM Calculation Methods

- Trial and Error: Manually testing different rates

- Excel XIRR Function: Automated calculation

- Financial Calculator: Built-in bond functions

- Mathematical Formula: For bonds with regular coupons

• Bond held until maturity

• All coupons reinvested at YTM rate

• Flat and static yield curve

• No default risk

• Unrealistic reinvestment assumption

• Assumes constant interest rates

• May not reflect actual returns

• Despite limitations, widely used for simplicity

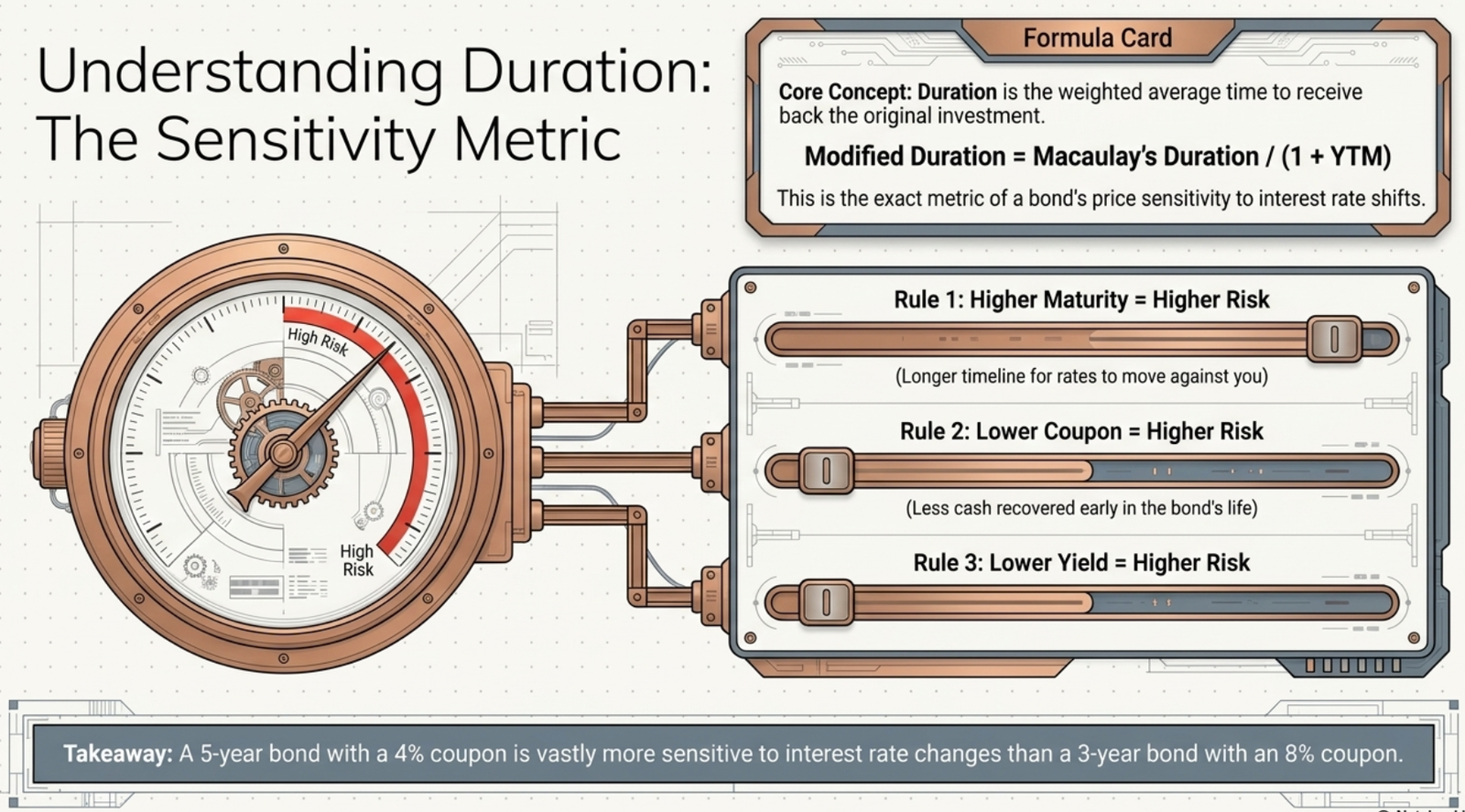

3.2.9 Duration

Duration measures the price sensitivity of bonds to interest rate changes. It's the weighted average maturity using present values as weights.

where t = time period of each cash flow

Factors Affecting Duration

| Factor | Effect on Duration | Effect on Interest Rate Risk |

|---|---|---|

| Higher Maturity | Increases Duration | Higher Risk |

| Lower Coupon Rate | Increases Duration | Higher Risk |

| Lower Yield | Increases Duration | Higher Risk |

• Portfolio immunization strategies

• Interest rate risk management

• Bond portfolio optimization

• Asset-liability matching

Modified Duration

Price Change % ≈ -Modified Duration × Interest Rate Change %

3.3 Types of Bonds

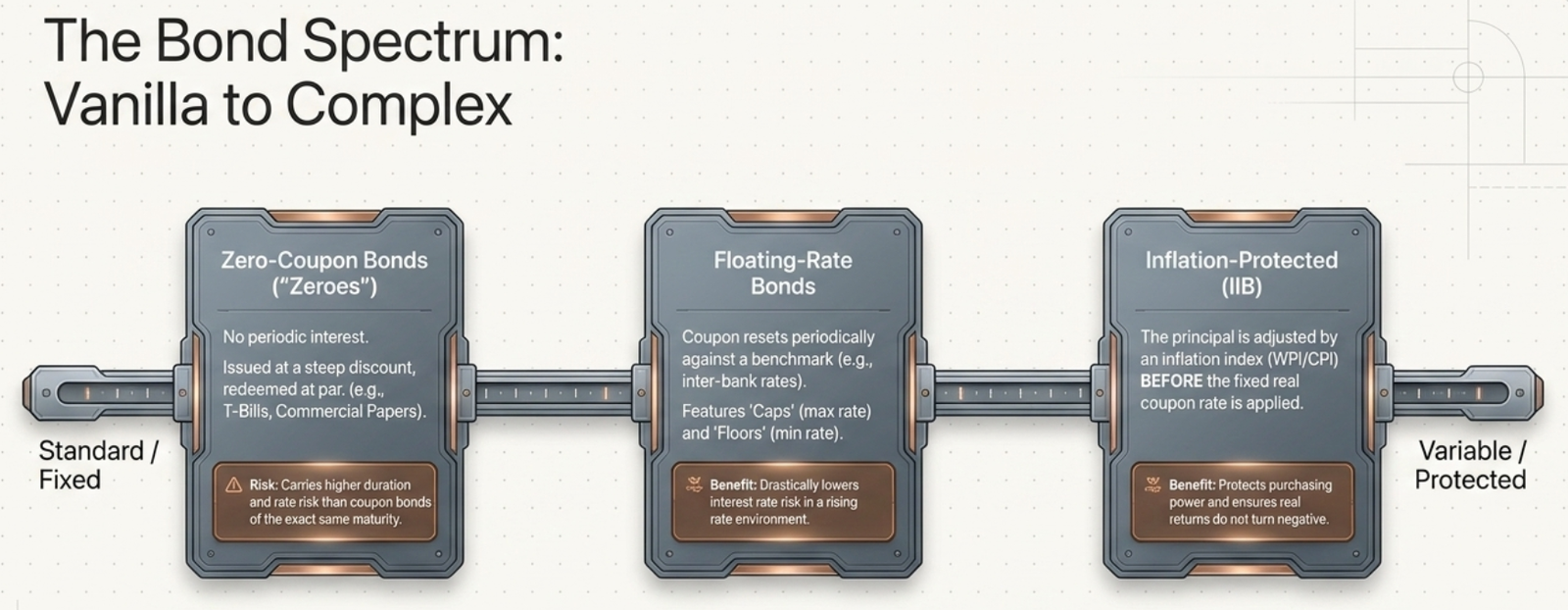

3.3.1 Zero-Coupon Bonds

Bonds that pay no periodic interest but are issued at discount to face value.

Zero-Coupon Bond Characteristics

| Feature | Zero-Coupon Bonds | Regular Bonds |

|---|---|---|

| Coupon Payments | None | Periodic |

| Issue Price | Discount to face value | Par, premium, or discount |

| Return Source | Price appreciation | Coupons + price change |

| Duration | Higher | Lower |

| Interest Rate Risk | Higher | Lower |

Examples of Zero-Coupon Instruments

- Treasury Bills: 91, 182, 364-day government securities

- Commercial Papers: Corporate short-term funding

- Certificate of Deposits: Bank/FI short-term instruments

- Deep Discount Bonds: Long-term zero-coupon bonds

- Kisan Vikas Patra: Government savings scheme

• Issuer: ETHL Communications Holdings Ltd (Essar Group)

• Issue Size: Rs. 4,280 crore

• Series 1: Issue price Rs. 85.80, Maturity value Rs. 100 (July 2011)

• Series 2: Issue price Rs. 82.55, Maturity value Rs. 100 (December 2011)

• Implied rates: 9.15% and 9.25% respectively

• Security: Backed by receivables

3.3.2 Floating-Rate Bonds

Bonds with variable coupon rates that reset periodically based on benchmark rates.

Floating Rate Mechanisms

| Benchmark | Reset Frequency | Typical Users |

|---|---|---|

| Inflation Index | Quarterly/Semi-annually | Government bonds |

| Inter-bank Rates | Monthly/Quarterly | Banking sector |

| Call Money Rates | Daily/Weekly | Short-term instruments |

| Government Security Yields | Semi-annually | Corporate bonds |

Cap and Floor Provisions

• Lower interest rate risk (duration risk)

• Beneficial in rising rate environment

• Automatic adjustment to market conditions

• Popular for long-term funding needs

Inverse Floaters

Advanced instruments where coupon moves inversely to benchmark rates (available in developed markets).

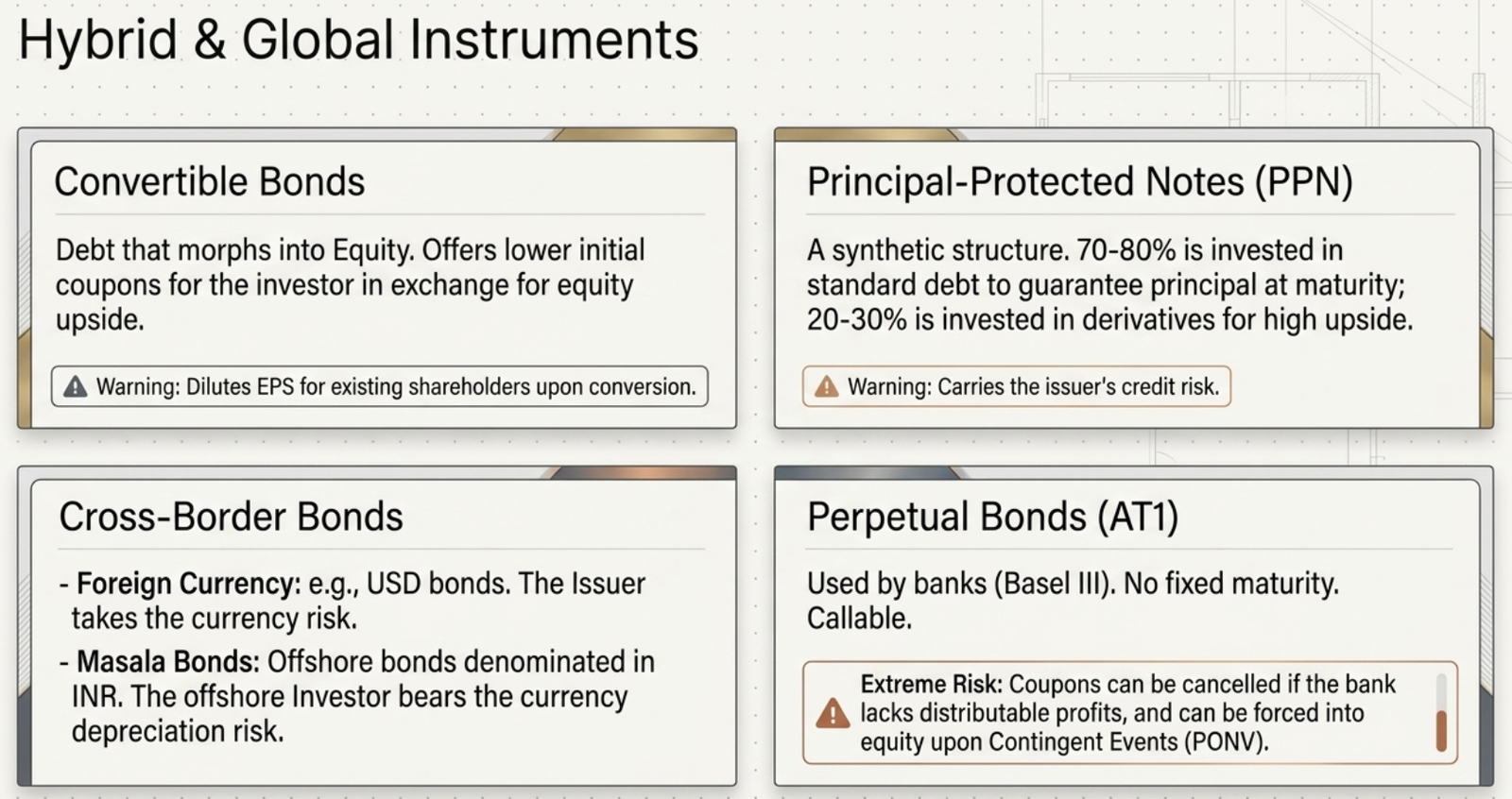

3.3.3 Convertible Bonds

Hybrid securities combining debt and equity features, allowing conversion to equity shares.

Types of Convertible Bonds

| Type | Conversion | Investor Control | Risk Profile |

|---|---|---|---|

| Optionally Convertible Debentures (OCD) | At investor's discretion | High | Lower |

| Compulsory Convertible Debentures (CCD) | Mandatory | None | Higher |

| Fully Convertible Debentures (FCD) | 100% converts to equity | Varies | Equity-like |

| Partly Convertible Debentures (PCD) | Partial conversion | Varies | Hybrid |

Conversion Terms Specification

- Conversion Date/Period: When conversion is allowed

- Conversion Ratio: Number of shares per bond

- Conversion Price: Effective price per share

- Conversion Premium: Discount to market price

- Conversion Proportion: Percentage of bond convertible

Impact of Conversion

| Stakeholder | Benefits | Drawbacks |

|---|---|---|

| Issuer | Lower coupon rate, no repayment obligation | Dilution of existing shareholders |

| Investor | Debt safety + equity upside potential | Lower initial coupon, conversion risk |

| Existing Shareholders | Company access to cheaper capital | Dilution of ownership and EPS |

3.3.4 Principal-Protected Note (PPN)

Structured product combining debt and derivative features to protect principal while offering upside potential.

PPN Structure

• 70-80% invested in debt to grow to principal amount

• 20-30% invested in derivatives/equity for returns

• Principal protection only if held to maturity

• Issuer credit risk remains

Types of PPNs

- Equity Linked Bonds (ELBs): Linked to stock market performance

- Commodity Linked Bonds (CLBs): Linked to commodity prices

- Currency Linked Notes: Linked to foreign exchange rates

- Index Linked Notes: Linked to market indices

• Credit risk of issuer (principal protection depends on issuer solvency)

• Liquidity risk (complex structure, limited secondary market)

• Market risk in derivative component

• Complexity risk (difficult to understand and value)

3.3.5 Inflation-Protected Securities

Bonds designed to protect investors from inflation erosion of purchasing power.

Inflation-Indexed Bonds (IIB) - RBI Issued

Index Ratio = Reference Index on Settlement Date / Reference Index on Issue Date

Coupon Payment = Fixed Real Rate × Inflation Adjusted Principal

• Original Principal: Rs. 1,000

• Fixed Real Rate: 2.5%

• WPI on Issue Date: 200

• WPI on Coupon Date: 210

Index Ratio = 210/200 = 1.05

Adjusted Principal = Rs. 1,000 × 1.05 = Rs. 1,050

Coupon Payment = 2.5% × Rs. 1,050 = Rs. 26.25

Inflation-Indexed National Savings Securities (2013)

- Tenor: 10 years

- Fixed Interest: 1.5% (floor rate)

- Inflation Adjustment: Based on CPI

- Compounding: Every 6 months

- Payment: At maturity (cumulative)

- Eligibility: Retail investors, HUFs, charities

3.3.6 Foreign Currency Bonds

Bonds issued in a currency different from the issuer's home country currency.

Foreign Currency Bond Analysis

| Aspect | Benefits | Risks |

|---|---|---|

| Cost of Capital | Lower interest rates in developed markets | Currency appreciation increases cost |

| Market Access | Broader investor base | Regulatory and compliance complexities |

| Credit Perception | Enhanced global profile | Foreign exchange volatility |

Delhi International Airport Limited (GMR Infrastructure SPV) USD Bond Issue (February 2020)

• Currency: US Dollars

• Benefit: Lower USD interest rates vs INR rates

• Risk: USD appreciation vs INR increases repayment cost

Currency Hedging Considerations

- Natural Hedge: Revenue in same currency as debt

- Financial Hedge: Derivatives to cover exposure

- Cost-Benefit: Hedging cost vs interest rate benefit

- Partial Hedge: Hedge only downside beyond threshold

3.3.7 External Bonds (Euro Bonds and Masala Bonds)

Euro Bonds

Bonds issued in a currency different from the country of issuance.

Indian company issuing USD-denominated bonds in London

• Issue Currency: USD

• Issue Location: London (GBP country)

• Currency Risk: Borne by issuer

Masala Bonds

External bonds denominated in Indian Rupees, transferring currency risk to investors.

| Feature | Foreign Currency Bonds | Masala Bonds |

|---|---|---|

| Currency | Foreign currency | Indian Rupees (INR) |

| Currency Risk | Borne by issuer | Borne by investor |

| Issuer Advantage | Lower rates initially | No currency risk |

| Investor Consideration | Currency gain/loss potential | INR depreciation risk |

• Issuer: International Finance Corporation (IFC)

• Issue Date: November 2014

• Listing: London Stock Exchange

• Denomination: Indian Rupees

• Significance: First offshore INR bond

3.3.8 Perpetual Bonds

Bonds with no stated maturity date, providing issuer with permanent capital.

Perpetual Bond Characteristics

| Feature | Regular Bonds | Perpetual Bonds |

|---|---|---|

| Maturity Date | Fixed | None |

| Principal Repayment | Mandatory at maturity | At issuer's discretion |

| Call Option | May or may not have | Usually callable |

| Coupon | Fixed schedule | Subject to conditions |

AT1 Perpetual Bonds (Basel III Compliance)

Special category of perpetual bonds issued by banks to meet Additional Tier 1 capital requirements.

- No Fixed Maturity: Never mandatory to repay

- Subordination: Rank below deposits, bank loans, other bonds

- Conditional Coupon: Payable only from distributable profits

- Non-Cumulative: Missed coupons are not paid later

- Conversion Trigger: Can convert to equity upon contingent events

AT1 Bond Risk Analysis

| Risk Type | Description | Impact |

|---|---|---|

| Coupon Risk | No payment if bank unprofitable | Income uncertainty |

| Perpetual Risk | No guaranteed principal repayment | Permanent capital loss risk |

| Conversion Risk | Forced conversion to equity at low prices | Significant value loss |

| Subordination Risk | Last to be paid in liquidation | Higher credit risk |

• Bank's capital ratio falls below regulatory minimum

• Point of Non-Viability (PONV) declared by regulator

• Bank faces severe financial distress

• Automatic conversion protects bank's solvency

Embedded Options in Bonds

Callable Bonds

Bonds with embedded call options allowing issuer to redeem before maturity.

Call Option Scenarios

| Interest Rate Environment | Issuer Incentive | Investor Impact |

|---|---|---|

| Rates Decline | High (refinance at lower rates) | Negative (reinvestment at lower rates) |

| Rates Rise | Low (no benefit to call) | Positive (locked in higher rate) |

| Rates Stable | Neutral | Neutral |

Puttable Bonds

Bonds with embedded put options allowing investor to sell back to issuer.

Put Option Benefits

- Interest Rate Protection: Sell if rates rise significantly

- Credit Protection: Exit if issuer credit deteriorates

- Liquidity Enhancement: Guaranteed exit option

- Reinvestment Opportunity: Access to higher yielding alternatives

3.4 Terminology in Commodity Markets

Commodity derivatives use specific terminology that research analysts covering commodity-linked companies and commodity ETFs need to understand.

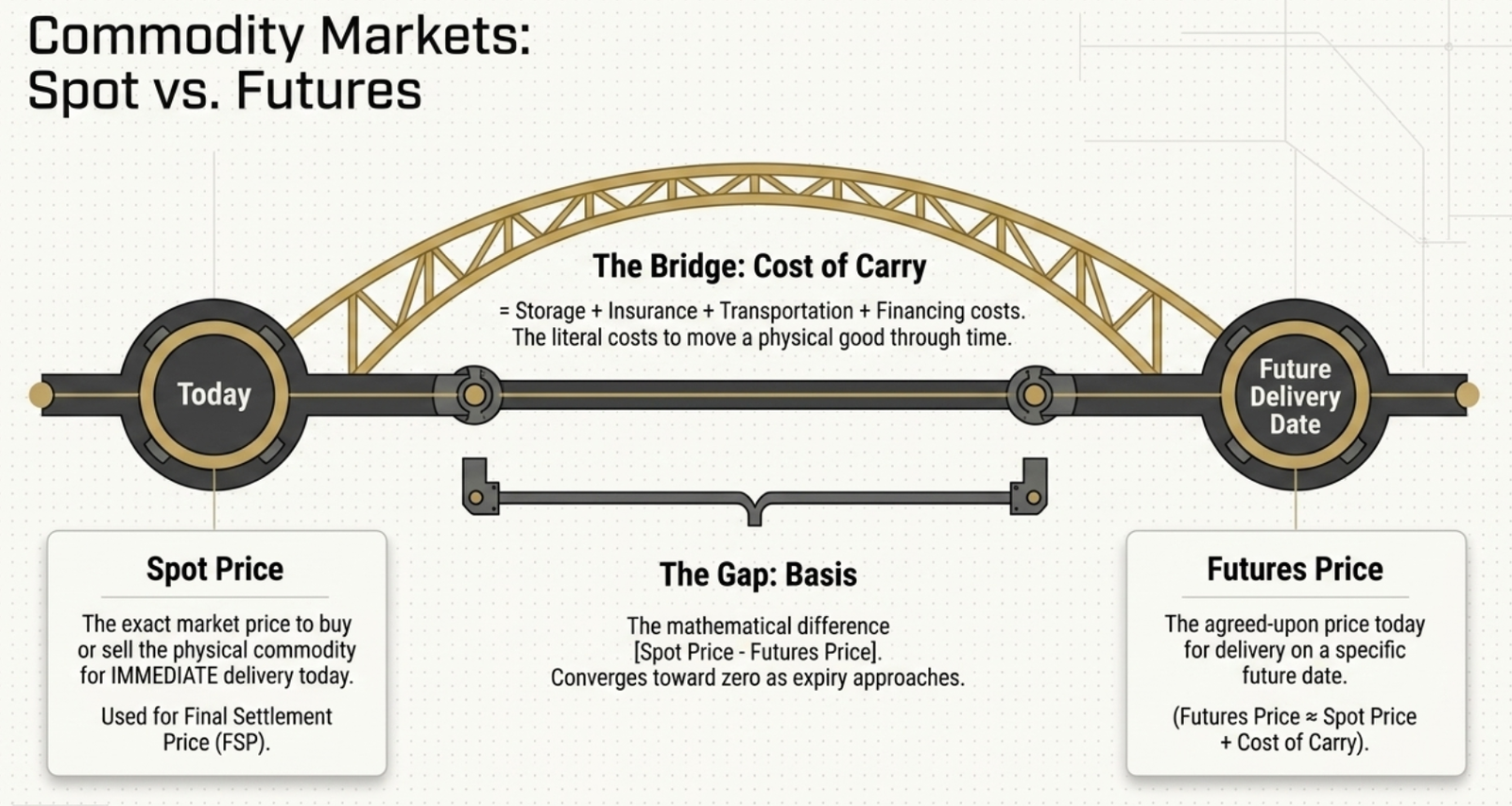

3.4.1 Spot Price

The spot price is the current market price at which a commodity can be bought or sold for immediate delivery. It is derived from the supply and demand of the commodity at any given moment. Commodity derivatives exchanges use spot price information on a daily basis as the basis for futures contracts traded on their platforms. These prices are also used for determining the Final Settlement Price (FSP), which is critical in the case of cash-settled commodity futures or in the event of delivery default by a short seller.

3.4.2 Basis

Basis is the difference between the spot price and the futures price of a commodity:

Since commodity derivatives are built on spot market prices, basis plays an important role in understanding the extent of the relationship between spot and futures prices. Basis can be positive (spot > futures) or negative (spot < futures), and it converges toward zero as the futures contract approaches expiry.

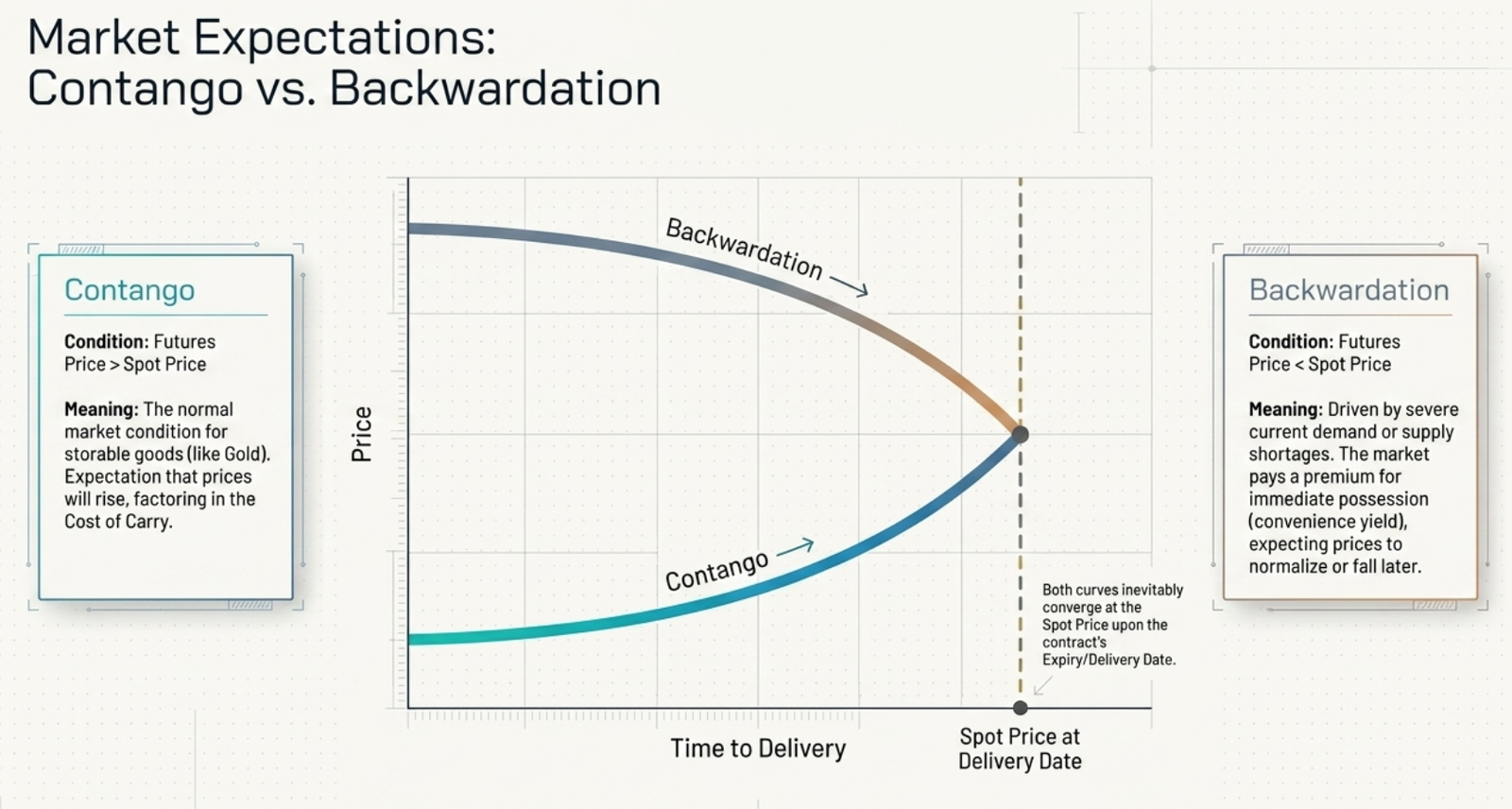

3.4.3 Contango

A commodity derivative is in Contango when the futures price is higher than the spot price. This usually occurs when market participants expect the spot price to rise in the near future, or when the cost of carry (storage + financing) is significant. Contango is the normal condition for most storable commodities (e.g., crude oil, gold). In a contango market, futures curves slope upward.

3.4.4 Backwardation

A commodity derivative is in Backwardation when the futures price is lower than the spot price. This typically occurs when there is strong current demand or a supply shortage, and market participants expect spot prices to fall in the future. Backwardation is common in seasonal agricultural commodities and during supply disruptions in energy markets. In backwardation, futures curves slope downward.

| Condition | Spot vs Futures | Market Expectation | Typical Example |

|---|---|---|---|

| Contango | Futures > Spot | Spot price expected to rise | Gold, crude oil in normal conditions |

| Backwardation | Futures < Spot | Spot price expected to fall | Perishable agri-commodities, supply shocks |

3.4.5 Cost of Carry

Cost of Carry is the total cost involved in holding (carrying) a commodity from the date of purchase in the spot market until the delivery date of the futures contract. It encompasses:

- Storage costs — warehouse fees, insurance

- Financing costs — interest on capital tied up in the commodity

- Transportation costs — moving commodity to delivery location

- Insurance costs — against damage or theft in storage

The cost of carry model explains the relationship between spot and futures prices: Futures Price ≈ Spot Price + Cost of Carry. This is why most storable commodities trade in contango under normal conditions — carrying a commodity forward costs money. For commodities with a convenience yield (like crude oil when refinery supplies are tight), the benefit of physically holding the commodity can outweigh the cost of carry, driving backwardation.

🃏 Flashcards

Click any card to reveal the answer. 64 cards covering the full chapter.

Comprehensive Sample Questions

Question 1: Bond Pricing and Interest Rates

A bond is issued at a face value of Rs.100 and a coupon of 10% p.a. The interest rates in the market have increased subsequently. This bond is likely to quote at:

- At a price above face value

- At the face value

- At a price that reflects its credit risk

- At a price below face value ✓

Answer: d) At a price below face value

Explanation: When market interest rates increase, existing bonds with lower coupon rates become less attractive. Investors can get better returns from new bonds, so the price of existing bonds falls below face value to compensate for the lower coupon rate.

Question 2: Intrinsic Value Definition

The __________ of an equity share is the discounted value of its future benefits to the investors.

- Intrinsic Value ✓

- Replacement value

- Market value

- Face Value

Answer: a) Intrinsic Value

Explanation: Intrinsic value represents the present value of all expected future cash flows from the investment, discounted at an appropriate rate. It's the theoretical "true value" of an asset based on fundamentals.

Question 3: Enterprise Value Calculation

Calculate the Enterprise Value based on the given information: Market Capitalisation = 10 lakhs; Total Debt = 3 lakhs; Cash = 4 lakhs.

- 11 lakhs

- 9 lakhs ✓

- 13 lakhs

- 6 lakhs

Answer: b) 9 lakhs

Enterprise Value = Market Cap + Total Debt - Cash

EV = 10 + 3 - 4 = 9 lakhs

Enterprise Value represents the total value of the business to all stakeholders, adjusting for cash which reduces the acquisition cost.

Question 4: Callable Bonds

Bonds which have embedded call option in them are known as Callable Bonds. State whether True or False.

- True ✓

- False

Answer: a) True

Explanation: Callable bonds contain an embedded call option that gives the issuer the right (but not obligation) to redeem the bond before maturity at specified dates and prices. This option is valuable to issuers, especially in declining interest rate environments.

Question 5: Zero-Coupon Bond Characteristics

Which of the following statements about zero-coupon bonds is TRUE?

- They pay interest semi-annually

- They have lower duration than coupon bonds of same maturity

- They are issued at discount to face value ✓

- They have no interest rate risk

Answer: c) They are issued at discount to face value

Explanation: Zero-coupon bonds pay no periodic interest and are issued at a discount to face value. The return comes from the difference between purchase price and maturity value. They actually have higher duration and interest rate risk than regular bonds.

Question 6: P/BV Ratio Interpretation

A stock trading at P/BV ratio of 0.8 indicates:

- The stock is definitely undervalued

- The stock is trading below its book value ✓

- The company has negative book value

- The stock will definitely appreciate

Answer: b) The stock is trading below its book value

Explanation: P/BV of 0.8 means market price is 80% of book value. While this suggests the stock trades below book value, it doesn't guarantee undervaluation - there may be fundamental reasons for the discount such as poor asset quality or business prospects.

Question 7: DVR Shares Regulation

According to Companies Act 2013, DVR shares cannot exceed what percentage of total post-issue paid-up capital?

- 10%

- 15%

- 20%

- 25% ✓

Answer: d) 25%

Explanation: The Companies Act 2013 restricts DVR shares to maximum 25% of total post-issue paid-up capital. Additionally, the company must have paid at least 10% dividend over the preceding 3 years to be eligible to issue DVR shares.

Question 8: Duration and Interest Rate Risk

Which bond would have the HIGHEST duration?

- 5-year bond with 8% coupon

- 5-year bond with 4% coupon ✓

- 3-year bond with 4% coupon

- 3-year bond with 8% coupon

Answer: b) 5-year bond with 4% coupon

Explanation: Duration increases with maturity and decreases with coupon rate. The 5-year bond with 4% coupon has both longer maturity and lower coupon than the alternatives, resulting in highest duration and interest rate sensitivity.

Key Takeaways for NISM Exam

Critical Concepts Summary

Equity Market Fundamentals:

- Face value is used for dividend calculations, not market valuation

- Intrinsic value vs market value determines investment opportunities

- Enterprise Value provides better comparison metric than market cap

- PE ratios should focus on forward earnings, not historical

- P/BV below 1 doesn't guarantee undervaluation

Debt Market Essentials:

- Bond prices move inversely to interest rates

- YTM is the most comprehensive return measure for bonds

- Duration measures interest rate sensitivity

- Zero-coupon bonds have higher duration and risk

- Floating rate bonds reduce interest rate risk

Advanced Bond Features:

- Convertible bonds offer lower coupons but equity upside

- Callable bonds favor issuers in declining rate environments

- AT1 perpetual bonds carry unique risks for investors

- Masala bonds transfer currency risk to investors

- Embedded options significantly affect bond valuation

Regulatory and Practical Aspects:

- DVR shares limited to 25% of capital with dividend history requirement

- Various bond types serve different investor risk-return profiles

- Understanding calculation methodologies is crucial for analysis

- Market dynamics affect pricing beyond fundamental calculations

Exam Preparation Tips

- Practice Calculations: Master EPS, PE, P/BV, EV, YTM, and duration calculations

- Understand Relationships: Know how interest rates affect bond prices and equity valuations

- Memorize Formulas: Key ratios and bond pricing formulas are frequently tested

- Scenario Analysis: Practice identifying optimal bond types for different market conditions

- Regulatory Knowledge: Remember DVR limits, AT1 features, and other regulatory aspects