📑 Chapter Navigation

Case Analysis

Practical Applications

📖 Complete Course Navigation

Foundation (Ch 1-4)

Market Analysis (Ch 5-8)

Technical Analysis (Ch 9-11)

Advanced (Ch 12-15)

Annexures (1–3)

- Annexure 1: Investor Charter

- Annexure 2: Complaint Data Format

- Annexure 3: Case Studies

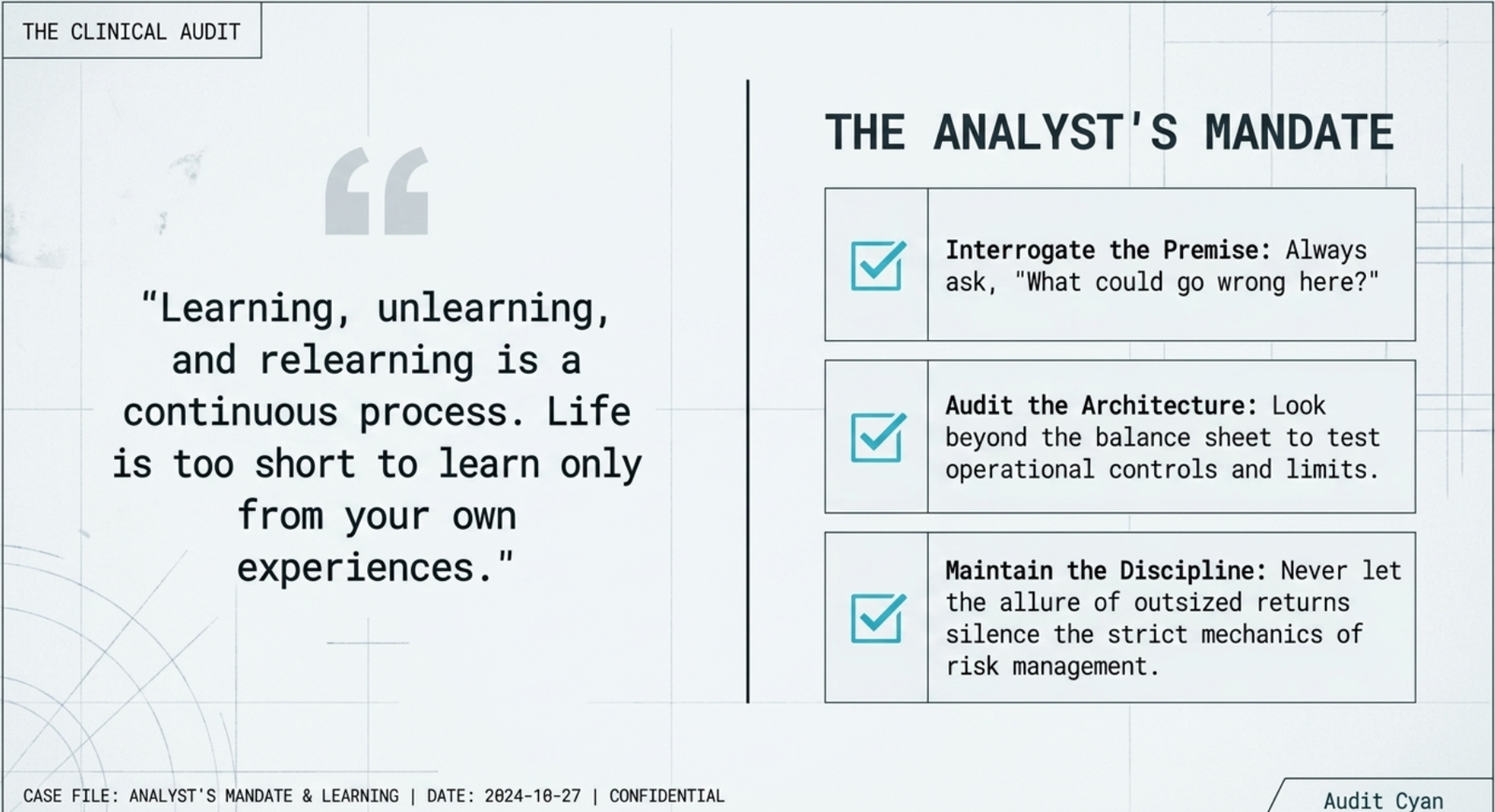

Learning from History: Learning, unlearning and relearning is a continuous process. Further, one can learn from their own experiences or experiences of others. As life is too short to learn everything from one's own experiences and his circle of understanding and influence is anyway very tiny, it is wiser to learn from experiences of others and historical events, which are very well documented in the historical cases.

History, indeed, is a great teacher, especially in the Financial Markets. If one doesn't learn from historical events in Financial Markets, he tends to repeat those mistakes. However, it is also interesting to quote a great philosopher 'Mark Twain' here who stated "We learn from the past that we don't learn from the past."

Couple of cases from the history are captured here for contemplation. Each of them would need a lot more research on the subject, if he/she intends to go into details of them:

Case 1 - Barings Episode

Background

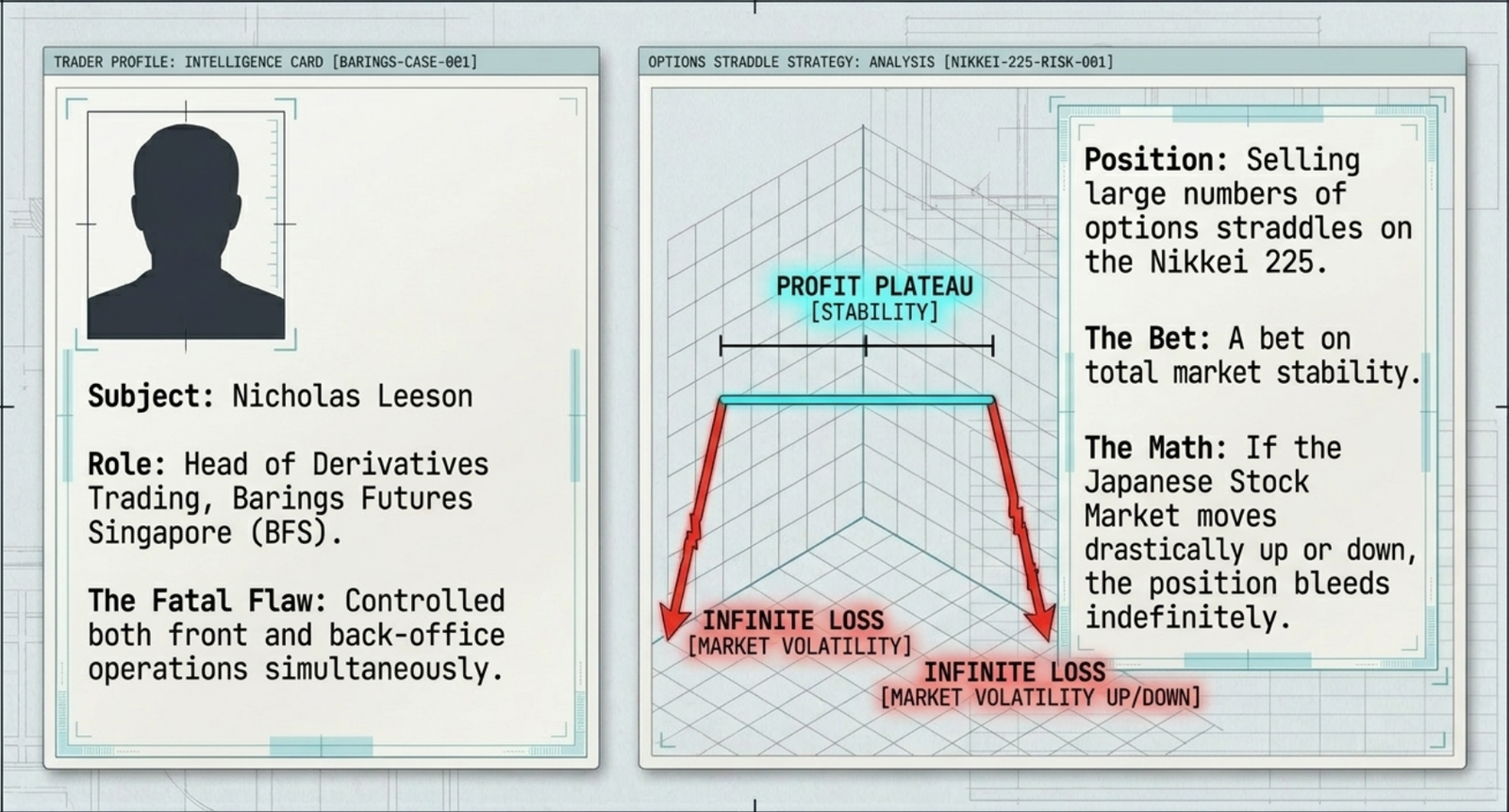

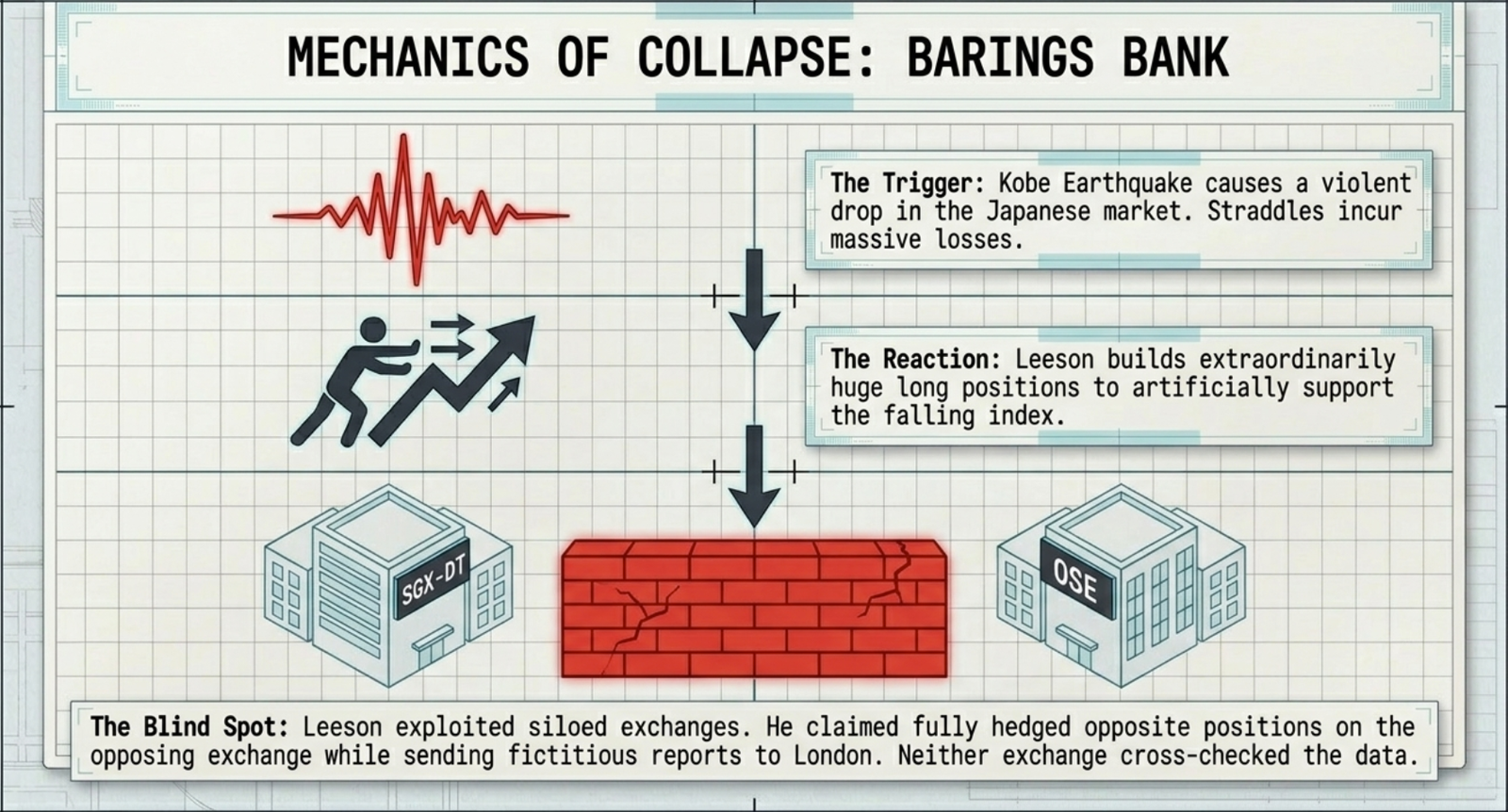

The man behind the debacle, Nicholas Leeson, had well established track record of being a savvy operator in the derivatives market and was the favourite of the top management at the Barings' headquarters at London. He was the head - derivatives trading, responsible for both front and back office, at Barings Futures, Singapore (BFS), a subsidiary of Barings Plc., London.

Leeson engaged himself in proprietary trading on Tokyo Stock Exchange Index, Nikkei 225. He was operating simultaneously on Singapore Exchange – Derivatives Trading Ltd., (SGX – DT) (erstwhile Singapore International Monetary Exchange, SIMEX), Singapore and Osaka Securities Exchange (OSE), Japan in Nikkei 225 futures and options. A major part of Leeson's trading strategy involved the sale of options on Nikkei 225 index futures contracts. He had sold large number of options straddles (a strategy that involves simultaneous sale of both call and put options) on Nikkei 225 index futures. Without going into intricacies, it may be understood that this straddle position results in loss, if market moves in either direction (up or down) drastically. His strategy amounted to a bet that Japanese Stock Market would neither fall nor go up, substantially i.e. he had the stable price perspective towards Japanese Market.

The Crisis

The Japanese stock markets started falling on the news of a violent earthquake in Kobe, Japan. With futures on Nikkei 225 going down, his straddle position started incurring loss. In pursuit of profit from his straddles, he started supporting the index by building up extraordinarily huge long positions in Nikkei 225 futures on both the said exchanges SGX – DT and OSE. However, the management of Barings was made to understand that Leeson was doing Nikkei 225 index futures arbitrage between SGX-DT and OSE.

When OSE authorities raised alarm about his huge long positions on the exchange in Nikkei 225 futures, he claimed that he had built up exactly opposite positions in Nikkei 225 on SGX - DT i.e. if his positions in Nikkei 225 at OSE suffer losses, these losses would get compensated by the profits of his positions at SGX - DT. Similar impression was given to the SGX - DT authorities, when they enquired about Leeson's positions.

Leeson kept giving misleading information to both the exchanges and neither of the exchanges bothered to crosscheck Leeson's positions on the other exchange because they were competing for business in Nikkei 225. Both the exchanges were more concerned about the protection of their financial integrity than anything else and so, allowed even the exceptionally large positions to Leeson after securing adequate margins.

The result is known to everyone. Single operator could not take the market in his desired direction and market fell down drastically. Resultantly, Barings blasted by registering losses on Leeson's both futures and straddle positions. But, we may see that its fire did not touch the financial integrity of either of the markets, SGX – DT or OSE because markets were absolutely safe through proper margining.

Issues behind the debacle & learning from the experience

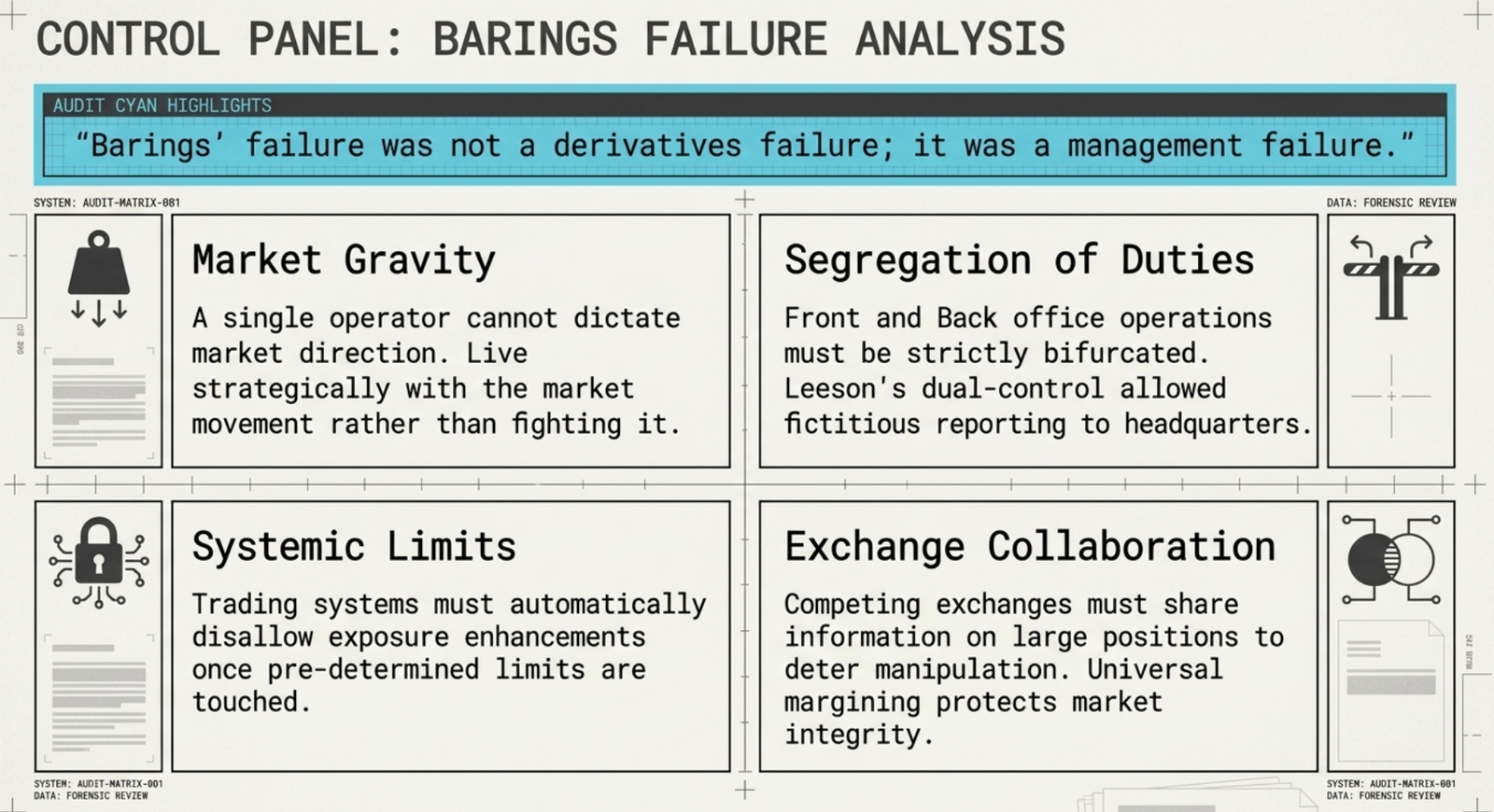

1. Single operator can't move the market:

Leeson was trying to drive the prices in upward direction by buying index futures on Nikkei 225, but could not succeed as market was gripped in the negative sentiments generating from earthquake in Kobe. The point here is that single operator can't change the direction of the market and it is always prudent to live with the market movement, strategically. In the instant case, better strategy for Leeson would have been the dynamic management of his portfolio. For instance, with decreasing value of index, his put leg of the straddle started incurring losses (call was to expire worthless), and he had the choice to square his put options off at the pre-determined level (cut off loss strategy). Leeson, instead of squaring off his short put option position chose to support the index price through buying futures on Nikkei 225 and failed.

2. Traders should have clearly defined and well-communicated position limits:

Position limits mean the limits set by the top management for each trader in the trading organization. These limits are defined in various forms like with regard to a product, a market or trader's total exposure in the market etc. Any laxity at this front may result in unbearable consequences to the trading organization. These limits should be clearly defined and well communicated to all traders in the organization.

3. Meticulous monitoring of the position limits is a must:

One can learn on research that Leeson too had position limits set by the top management, but he crossed all of them. This attempt of outpacing limits by Leeson did not come to the notice of top brass at Barings as he himself was supervising the back office operations at BFS. It is understood that he had sent fictitious reports concerning his trading activities to the Barings' headquarters in London. Had the top management known the real position, probably, the disaster could have been avoided.

Therefore, scrupulous monitoring of the position limits is as important as setting them. Top management's job of monitoring the positions of each dealer in the dealing room may be facilitated by bifurcating the front and back office operations. Different people should be in charge of front and back office operations so that any exposure of dealers, over and above the limits set for them, can be detected immediately. This is the issue of having proper checks and balances at various levels to ensure that everyone in the organization has disciplinary approach and work within the set limits. In fact, trading systems should be capable enough to automatically disallow traders any enhancement in their exposures as soon as they touch their pre-determined limits.

4. Exchanges should share information on large positions:

Both the competing exchanges SGX – DT and OSE were not concerned about checking Barings' position at the other exchange. Well, both the exchanges were safe through margins, but everyone would appreciate that the effect of a big failure, like Barings, goes much beyond the financial integrity of a system. An important point to note is that the Exchanges should compete but at the same time co-operate and share the information, which may shake the entire financial system. Further, it is important from the point of view of deterring any price manipulation effort, which a member of two exchanges can make by using two independent systems.

5. Big Institutions are as prone to risk as individuals:

One broad issue from the overall market's perspective is that big Institutions are as prone to incurring losses in the derivatives market as any other individual. Therefore, irrespective of the entity, margins should be collected by the Clearing Corporation/ house and/ or exchange that too on time. Only, timely collection of the margins can protect the financial integrity of the market as seen in the Barings case.

Above-mentioned points 1 to 3 are relevant to the trading organizations in derivatives market. They have to intelligently work in-house to avoid any miss-happening like Barings at any point in time. Point 4 is relevant to the exchanges and they should work in collaborative manner and improve inter exchange communication and co-ordination. With regard to the point 5, SEBI has done a good job in the Indian derivatives market by making margins universally applicable to all categories of participants including Institutions. This provision will go a long way to create a financially safe derivatives market in India.

Conclusion

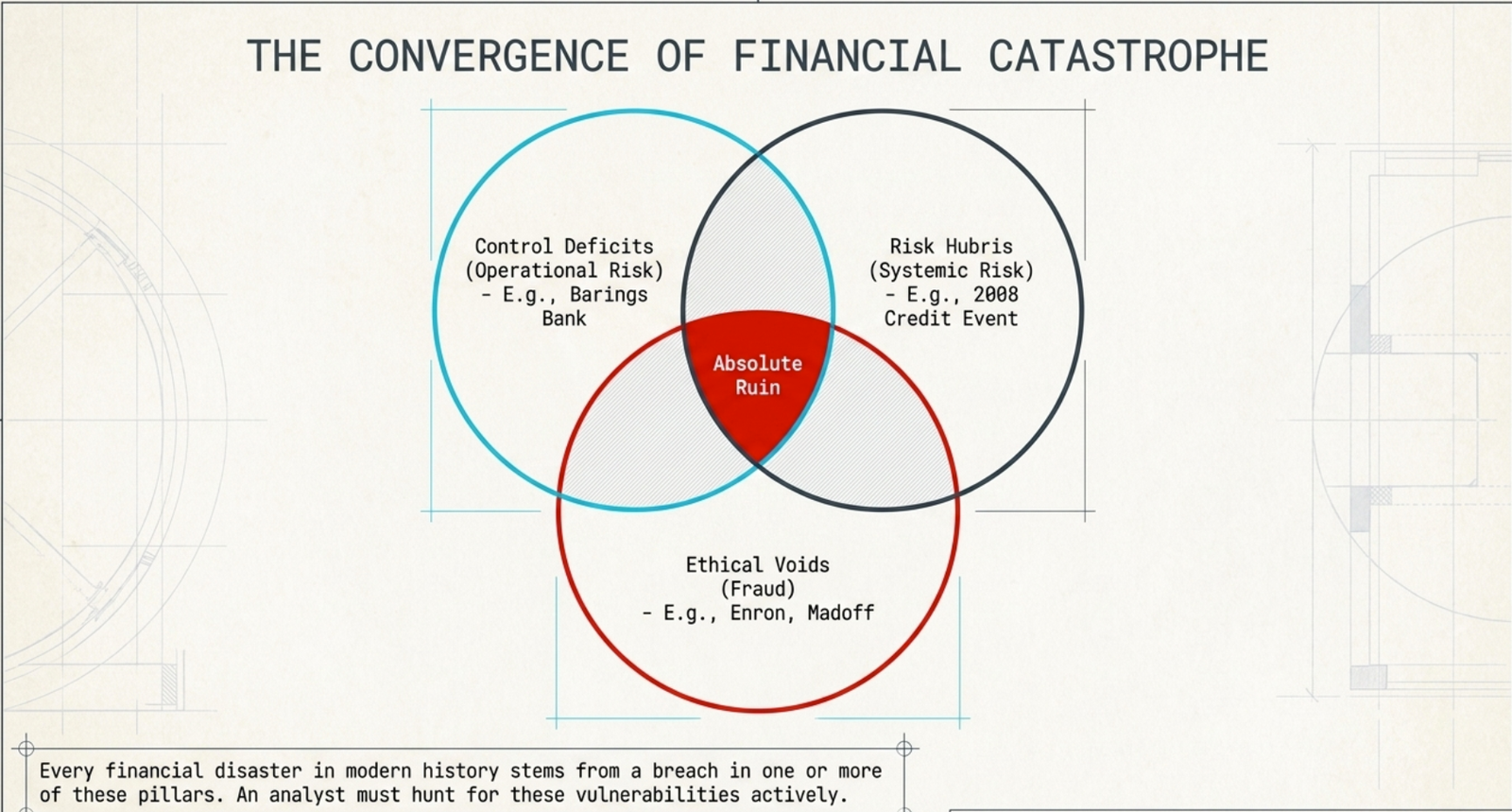

In view of the above, Barings episode may be summarized by stating that "Barings' failure was not the derivatives failure, it was management's failure". After the enquiries in Barings case, the Board of Banking Supervision's report also placed responsibility for the Barings' debacle on poor operational controls (operational risk) at Barings rather than the use of derivatives. Important learning from the entire episode is that we all have to have a disciplinary and self-regulatory approach. The moment, one go against this fundamental rule, this leveraged market may threaten his very existence and reduce him to absolute ashes.

Post Barings episode, operational risk became glaring and financial organizations across the world started clearly demarcating front and back office operations. Further, regulators drove the competing exchanges to work in a close manner and share information, which could threaten the existence of the financial markets. Also, in markets today, all positions, irrespective of the owner, are margined to recognize that institutions are as prone to risk as individuals. In nutshell, Barings episode taught significant stuff on operational risk front to the Financial Markets across the world.

Case 2 - Credit Event of 2008 and impact on Financial Markets

The Setup

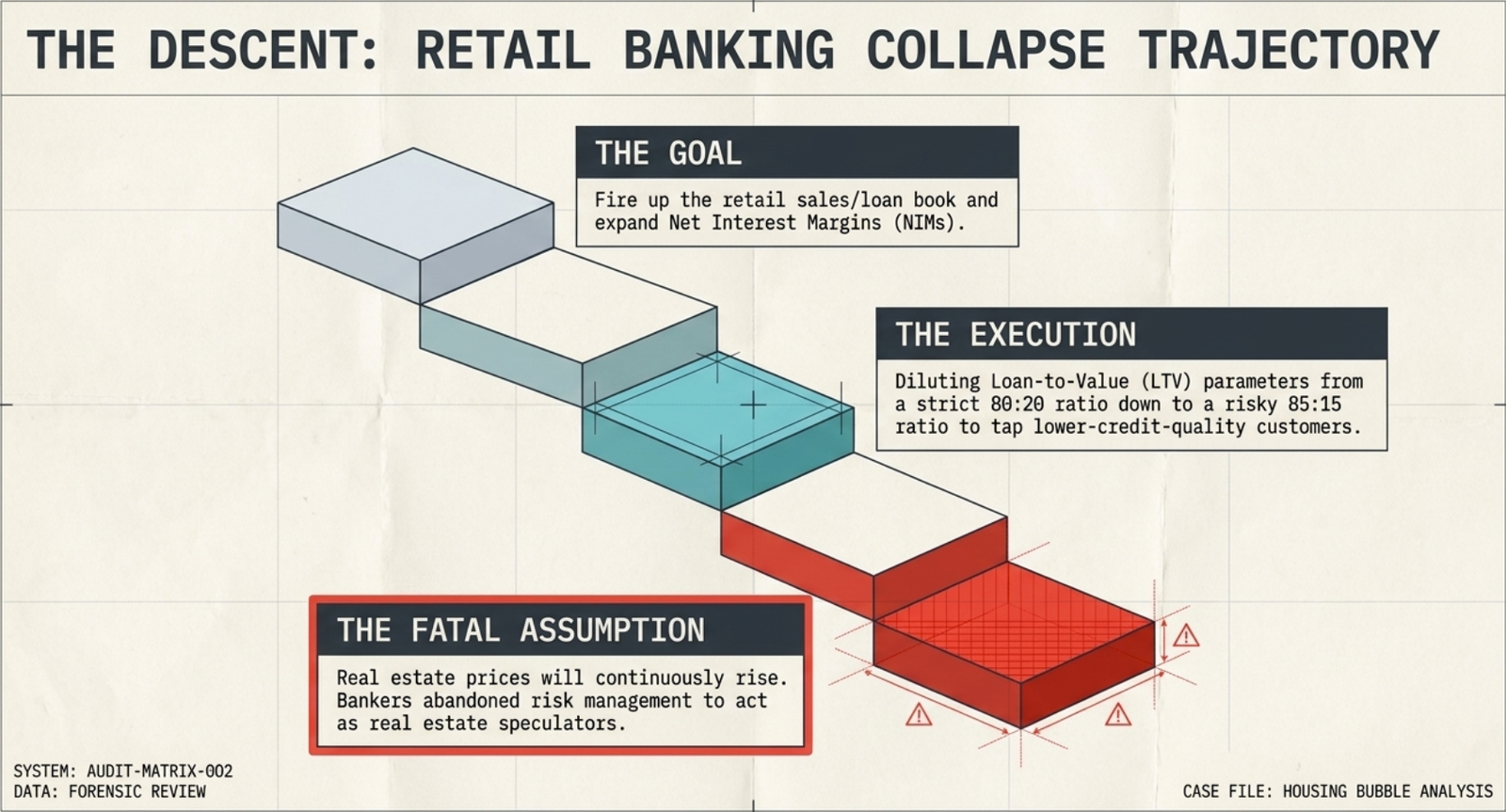

Let us hire a sales person in the Mortgage business in a bank. He has just joined on retail side with responsibility to drive the housing finance book of the bank. He spends time thinking and analyzing the data and recommends the following as strategy to fire up the sales/loan book:

- Bank may approach less credit worthy guys to expand the market.

- Bank may dilute Loan to Value (LTV) parameter to go say from 80:20 to 85:15 rule on lending (80% or 85% being loan amount against the value of asset).

- This could, indeed, expand bank's net interest margins (NIMs) as extending credit to less credit worthy guys would fetch the bank higher interest rates.

Assuming, the bank in pursuit of expanding its loan book, follows his said recommendations. Let's see what happens then.

What Actually Happened

Actually, the banks followed exactly the above thought process starting 2003-2004 to the culmination of credit event in 2008. Competing banks kept diluting their standards on loan to value ratio to tap the further lower credit quality customers. As higher margins were coming in, business looked quite attractive to the bankers. Only thing all bankers were ignoring was the risk of potential default on this loan book.

Whenever bankers were asked about the credit or default risk on the subject, they indicated towards the continuously increasing real estate prices. Argument was simple that if borrowers don't pay, we run little risk of recovery given the continuously rising prices of real estate. They never imagined the situation of real estate prices going down along with defaults on loan. It was a typical case of bankers taking view on real estate, which is not their job. Should we call it going beyond their jobs or call it complete disregard for the risk management on an asset portfolio (mortgage book).

The Securitization Game

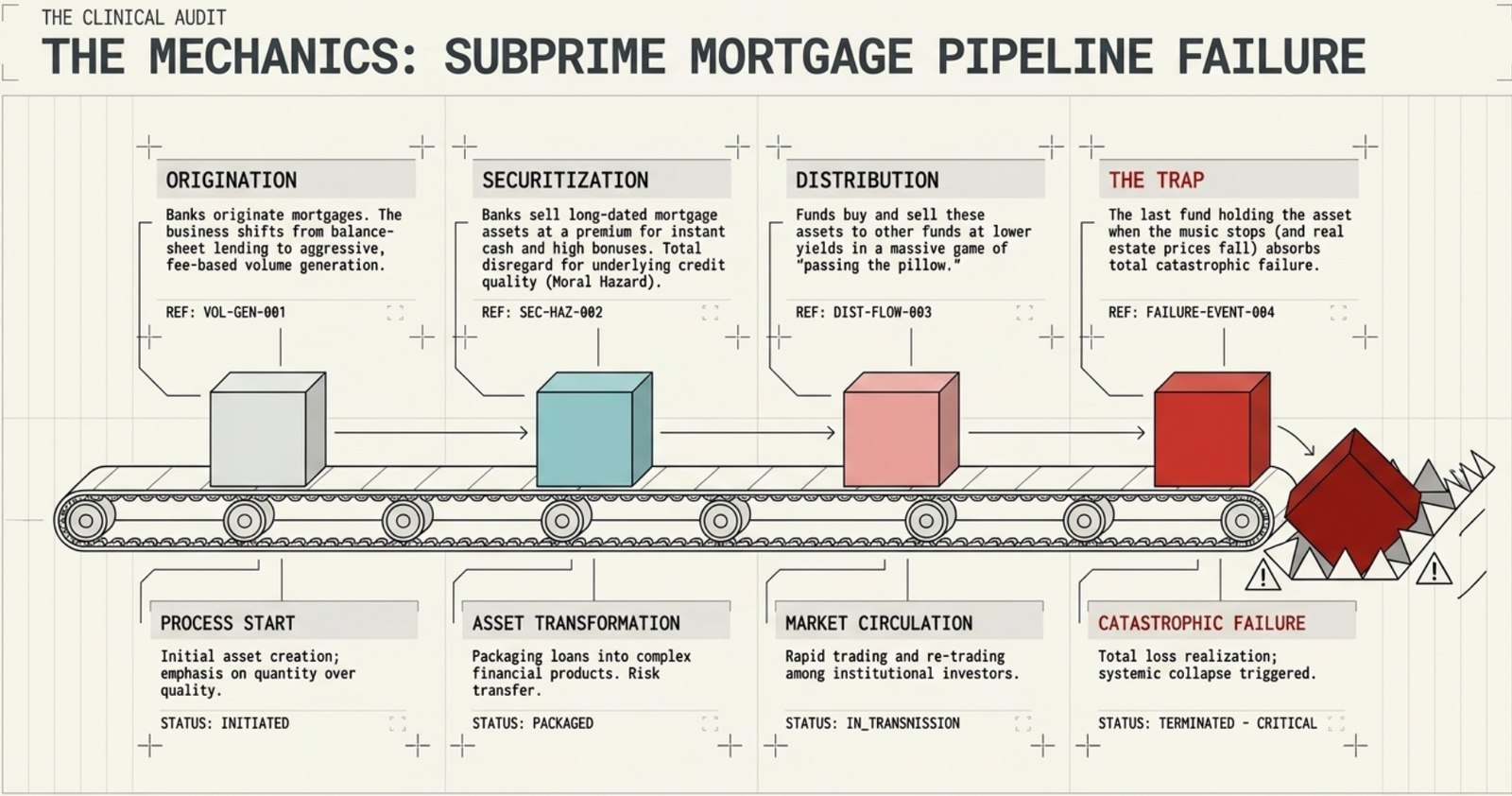

Banking looked quite simple – put the liabilities and put the assets; keep growing the books with increasing Net Interest Margins (NIMs). But, then came the issue of supply of capital. To lend more, one needed to borrow more. Supply of capital became a constraint to the growth. Creative bankers found the solution in terms of selling some assets to get cash, which can be further lent.

Bankers found it interesting to sell long dated mortgage assets to investors at a yield lower than their own yields. This means selling assets at premium to their face value. Good for the bankers as they recognized the profits on sale of long dated assets at the time of sale itself. This also meant higher bonuses for the bankers. Now, bankers found an interesting opportunity to generate assets, sell them at lower yield (book capital gains on that) to generate cash and further lend that cash to grow. Indeed, slowly and slowly they stopped bothering about the credit quality of mortgage buyers as long as there were investors in those originated mortgage assets available - a clear risk of moral hazard. For banks, mortgage business turned to be kind of fee based business from lending (balance sheet based business).

The Borrowers' Perspective

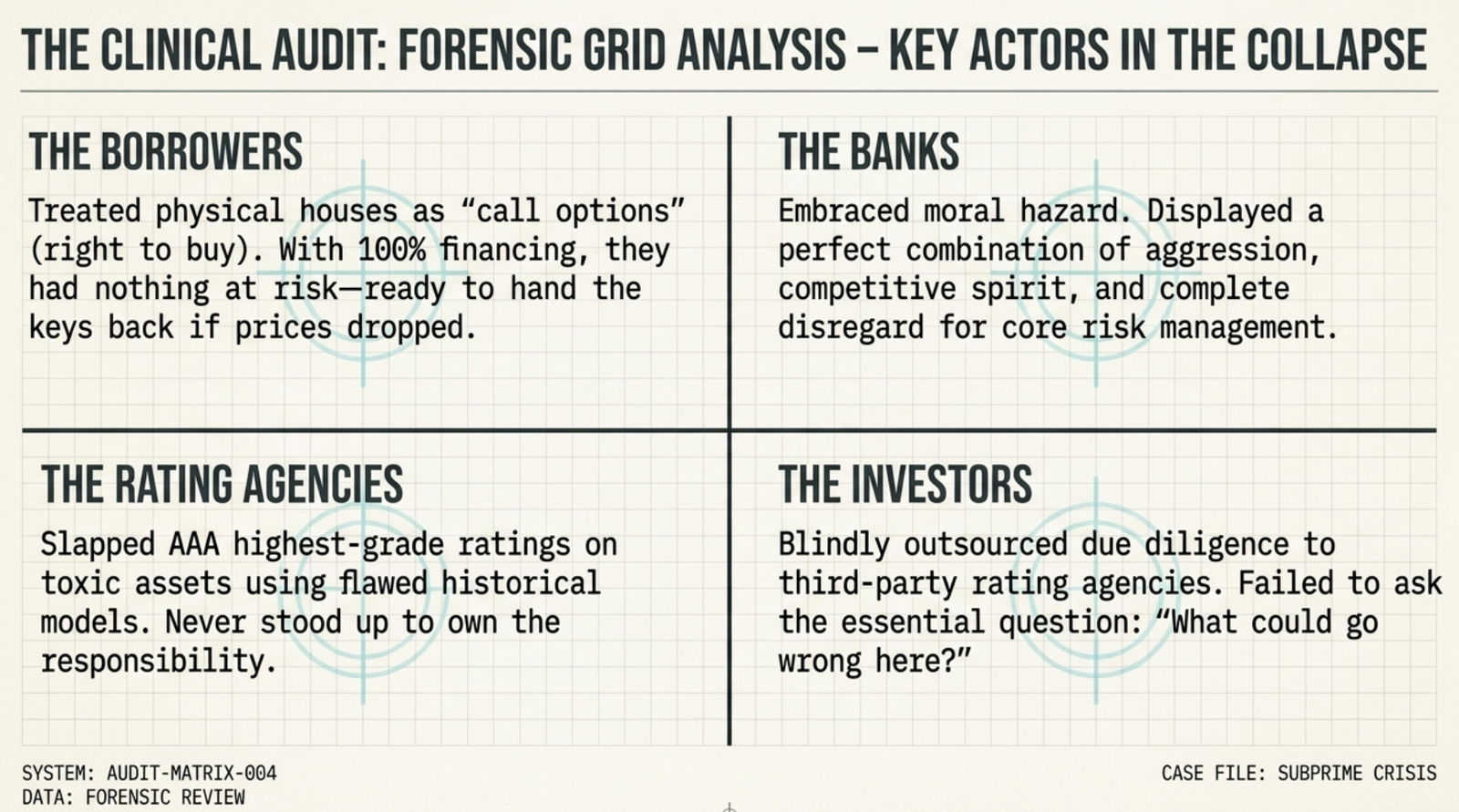

Let's understand perspective of house buyers/owners. They started looking at buying assets as call options (right to buy). They had very little or nothing at risk as competing banks were offering them almost 100% financing option. Their thought was quite clear and simple - If prices of assets go up, they could sell the house and repay to the bankers with some profits left for them; and, if prices of assets go down, they would turn the keys to the bankers. Clearly, there were lots of takers for the mortgages with these dynamics of finance.

As long as prices continue to climb, there was vibrancy all around. However, when prices of assets started to stumble, banks started encountering more and more defaults from the buyers/owners. It came like a falling pack of cards, when things turned bad.

The Investors' Role

Let's turn to the side of investors for mortgaged backed securities. Investors had money but no origination point. As banks had large machinery for origination of mortgages, it was a perfect marriage between banks and investors (funds). Banks would originate mortgages and turn the portfolio to funds at an origination price (discount on the mortgage rate). Investors also sold those assets to the other investors at lower yields and the process continued. Like in the game of passing the pillow, funds, which owned these mortgage assets last were the ones to be penalized by the event. They found themselves sitting on the assets, where prices fell sharply to couple of cents to the $ face value.

The Rating Agencies

It is also interesting to touch rating of these mortgage backed securities. Credit rating agencies always believed in the great quality of these securities, specially, given the fact that these were backed by the hard assets and history on the subject. Most of these mortgage backed securities were accordingly rated highest grade (AAA kind of). Investors/funds of these papers relied heavily on the ratings by rating agencies in absence of their own capability or bandwidth to do the work on credit quality. Prima facie, we may also state that credit rating agencies did not understand the risks in these assets properly.

In addition to above all, there were lots of credit derivatives being written on these mortgaged backed securities by several institutions. Institutions were taking both trading and hedging positions on these securities in the credit derivatives market.

Learnings from the event:

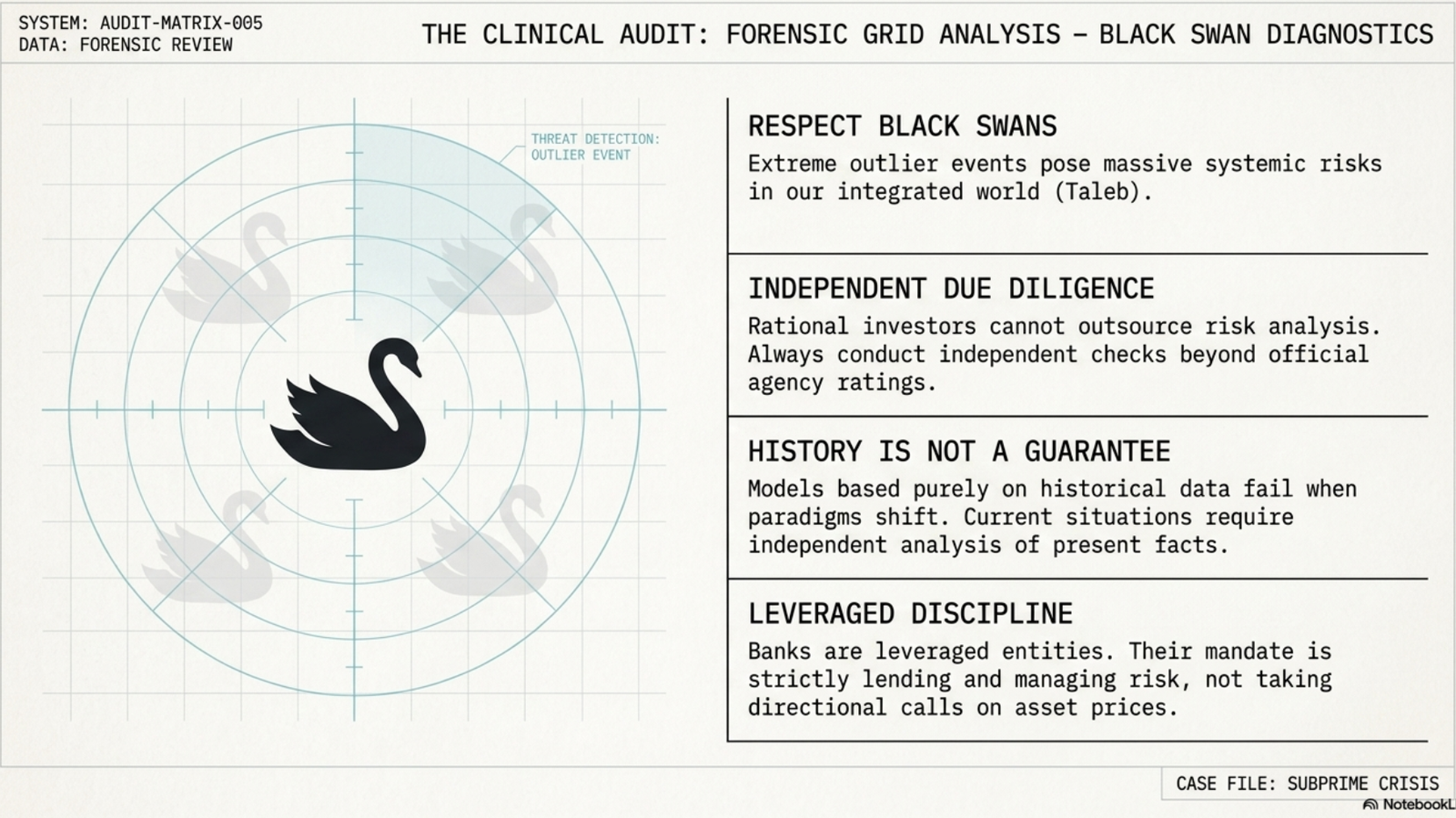

Banks' Responsibility: Banks' attitude may be summarized as a perfect combination of aggression, competitive spirit, view on assets, complete disregard for risk management, moral hazard etc. etc. Banks, being a leveraged entity, must behave in a very disciplined manner all the time. They are into business of lending and not taking calls on the prices of assets. Also, risk management is the heart of the banking operations and competing banks should never dilute their risk management standards in pursuit of higher levels of business.

Investors' Due Diligence: Investors should behave rationally. They should do their independent due diligence in addition to their reliance on third parties such as credit rating agencies. One question investors should ask continuously is "what could go wrong here."

Don't Rely Solely on Historical Data: While history is important, decisions can't be taken purely on the basis of historical data. Credit rating agencies relied heavily on the historical understanding of mortgage markets. While, one should learn from the past, current situation should be analysed independently with facts and figures in hands. While credit rating agencies are liable to a large extent for 2008 event (highest rating of these securities AAA kind off attracted many buyers and sellers to these securities), we never saw any credit rating agency in the world standing up to own the responsibility ever.

Respect Limitations and Black Swan Events: One more thing we learn from this event is that we should respect our limitations on understanding markets. As Dr. Nicholas Taleb mentions "Black Swan events pose significant risk in this integrated world". Therefore, risk management should be paramount for institutions in all the situations.

Some more case studies:

Warren Buffett once stated: "People with pen do much bigger thefts than the people with guns."

Financial markets and businesses appear to be filled with many such stories. Many individuals in the world of business and finance found it difficult to resist the temptation of opportunities to cheat even at the cost of their own reputation and potential downfall.

Over the years, many promoters of "Wall Street darling companies" have breached the trust of the general public to satisfy their own hunger for money and power. Fund managers have also cheated their investors with the means beyond anyone's imagination. Here are some of the stories from the recent past for your contemplation.

Disgraced companies/institutions

Enron:

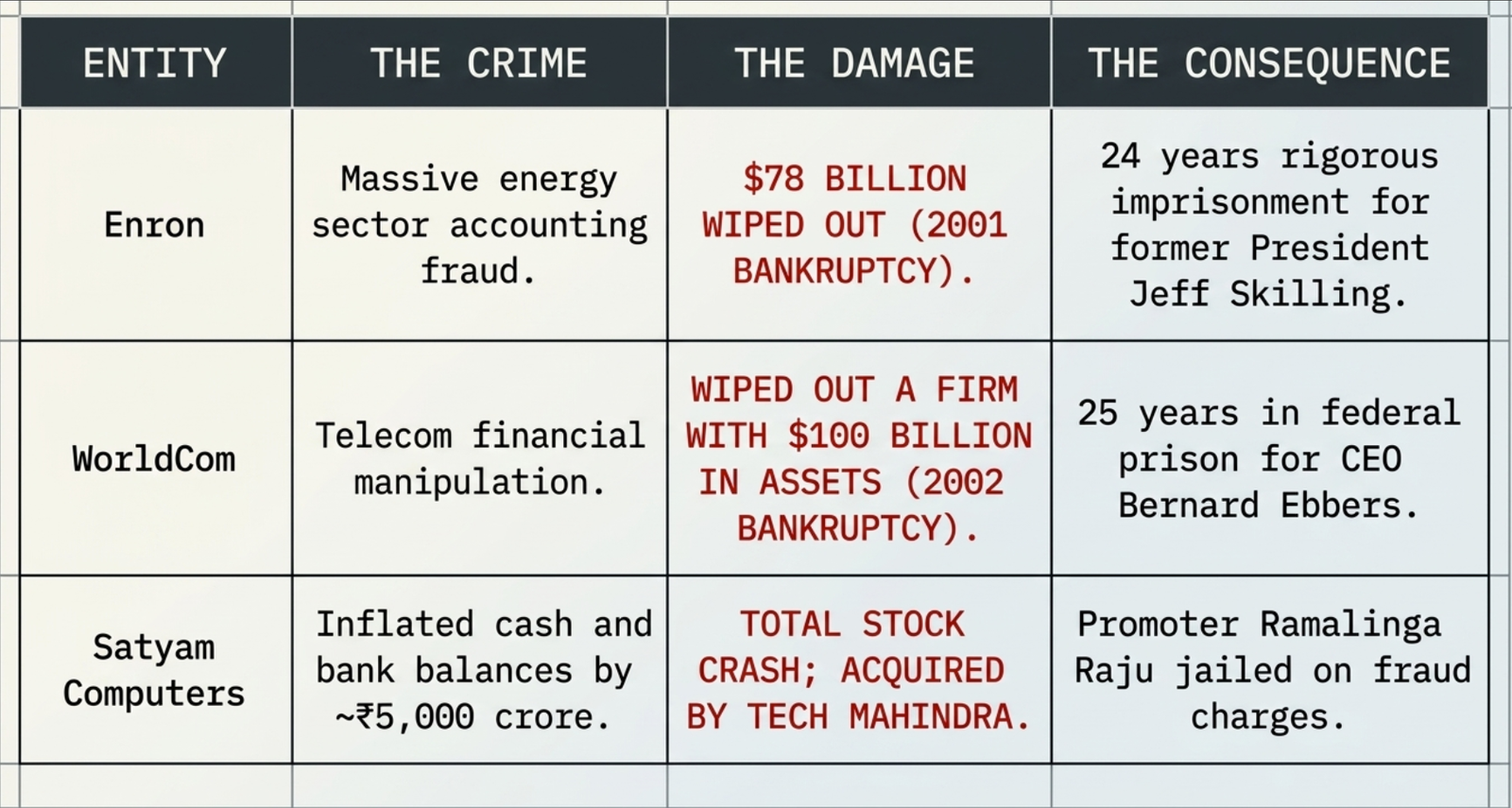

Enron was an incredibly energetic, innovative and creative company in power trading space. Allegations of massive accounting fraud wiped out $78 billion in stock market value of the energy company and resulted in its bankruptcy in 2001. Former President Jeff Skilling is serving a 24 years rigorous imprisonment in jailon charges of accounting frauds and manipulations.

WorldCom:

WorldCom, a telecom giant, also went through the manipulation of financials and fraud by its top management team. The 2002 fraud-induced bankruptcy of this company wiped out a firm that once had more than $100 billion in assets on its books. Former CEO Bernard Ebbers was convicted of fraud and is doing 25 years in federal prison.

Satyam Computers:

Promoter of Satyam, Ramalinga Raju confessed in 2009 that he had cooked up the accounts of Satyam Computers and that the cash and bank balances were inflated by ~Rs 5,000 crore, after a failed attempt to acquire promoters' owned another company Maytas. Investors lost millions as the stock came crashing after the news was out. Raju was put behind bars with multiple charges including fraud and manipulation. Satyam Computers has since been acquired by Tech Mahindra.

Disgraced Fund Managers

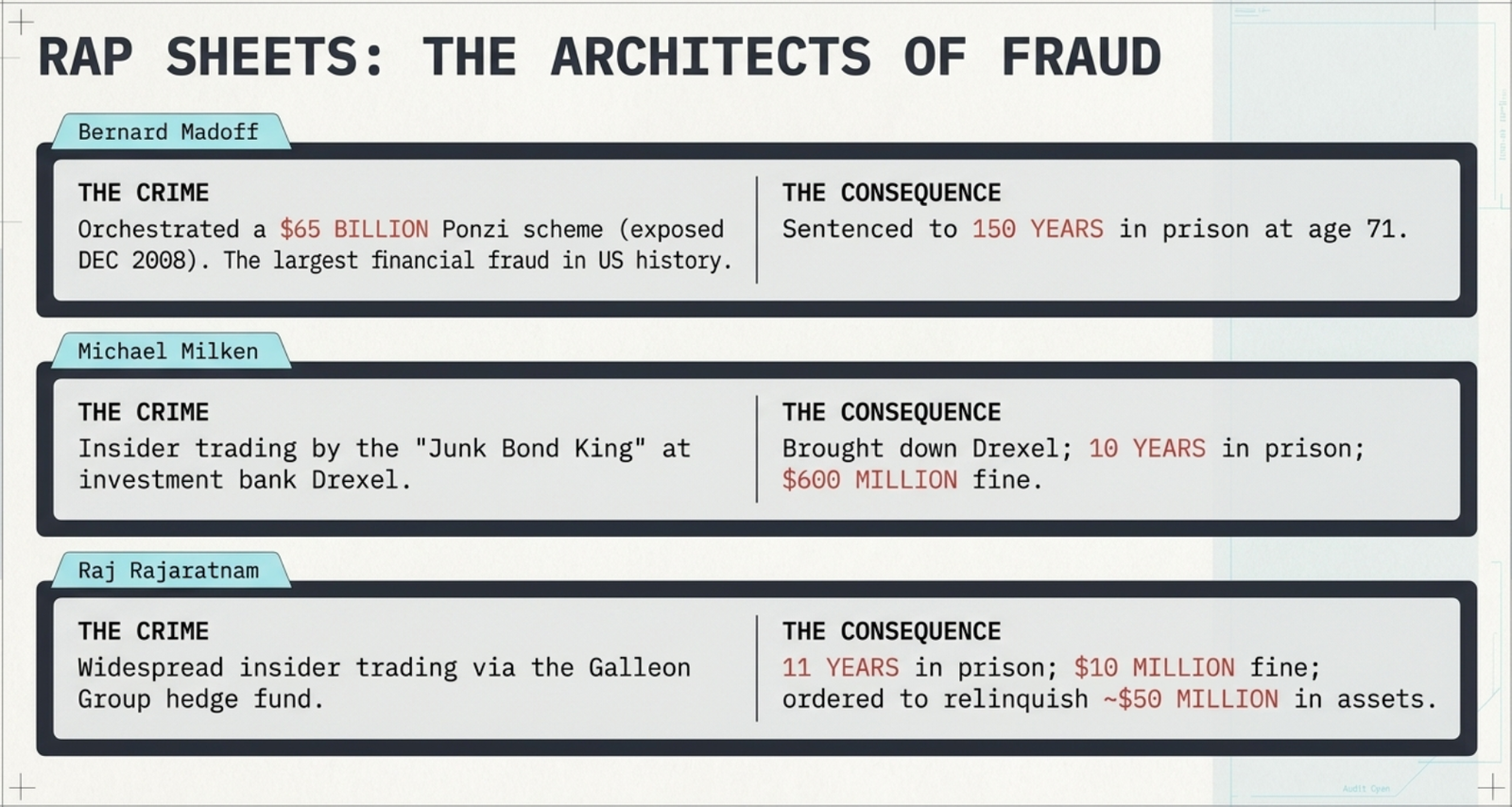

Bernard Madoff:

New York money manager Bernard Madoff orchestrated $65 billion Ponzi scheme, largest financial fraud in the history of the United States, and got exposed in December 2008. In June 2009, 71-year-old Madoff was sentenced to 150 years in prison on 11 counts of fraud, money laundering and theft.

Michael Milken:

In the mid-1980s, Michael Milken of Drexel, an investment banking firm, was known as "Junk Bond King". But insider trading brought the house down and left Drexel fighting bankruptcy. Milken was sentenced to 10 years in prison. He paid a significant $600 million fine.

Raj Rajaratnam:

In 1997, billionaire Sri Lankan-American businessman Raj Rajaratnam co-founded hedge fund management company Galleon Group. In October 2009, he was arrested and charged with several cases of insider trading. In October 2011, he received a sentence of 11 years in prison, pay a $10 million fine and order to relinquish assets worth ~$50 million.

🃏 Flashcards

63 cards · click to reveal the answer · use search to focus on a topic