📑 Chapter Navigation

📖 Complete Course Navigation

Foundation (Ch 1-4)

- Ch 1: Research Analyst Profession

- Ch 2: Securities Market

- Ch 3: Terminology

- Ch 4: Research Fundamentals

Analysis (Ch 5-8)

Advanced (Ch 9-13)

Annexures (Ch 14-16)

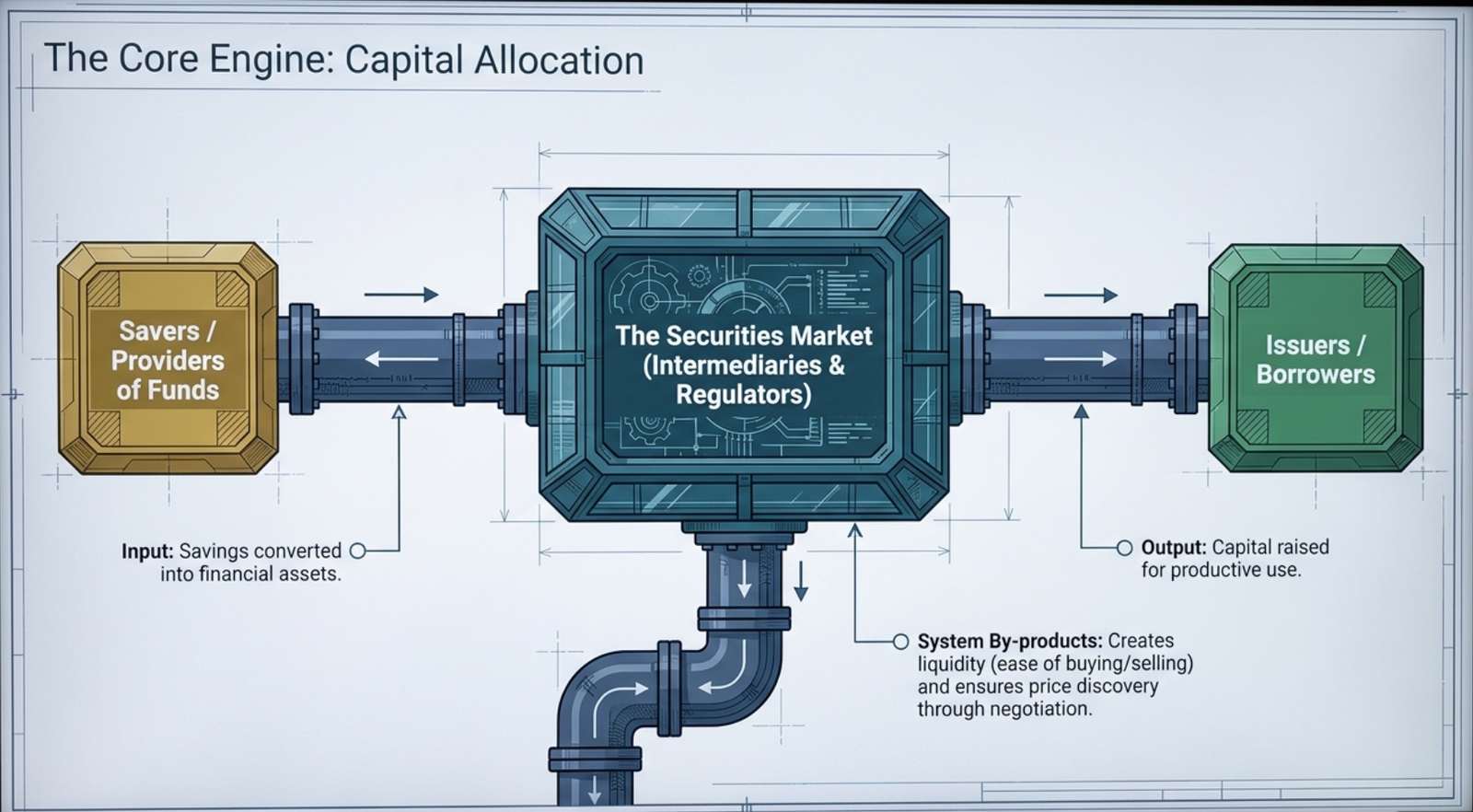

2.1 Introduction to Securities and Securities Market

Examples include: Equity shares, preference shares, debentures, bonds and other such instruments issued by companies, financial institutions or the government.

The Dual Function of Securities

For Investors

Convert savings into financial assets that provide returns

For Issuers

Raise money at a cost to fund business operations and growth

Key Advantage: Securities allow investors to transfer their rights/interests to others without impacting the issuers, enabling long-term capital raising while providing liquidity to investors.

Financial Market Components

(Buyers of Securities)

(Sellers of Securities)

(Infrastructure Facilitators)

(Orderly Development)

Functions of Securities Market:

- Provides channels for conversion of savings into investments

- Connects a broader universe of savers with issuers of securities

- Creates liquidity by bringing together large number of buyers and sellers

- Facilitates resource transfer from those with idle/surplus resources to productive users

- Enables price discovery through efficient market mechanisms

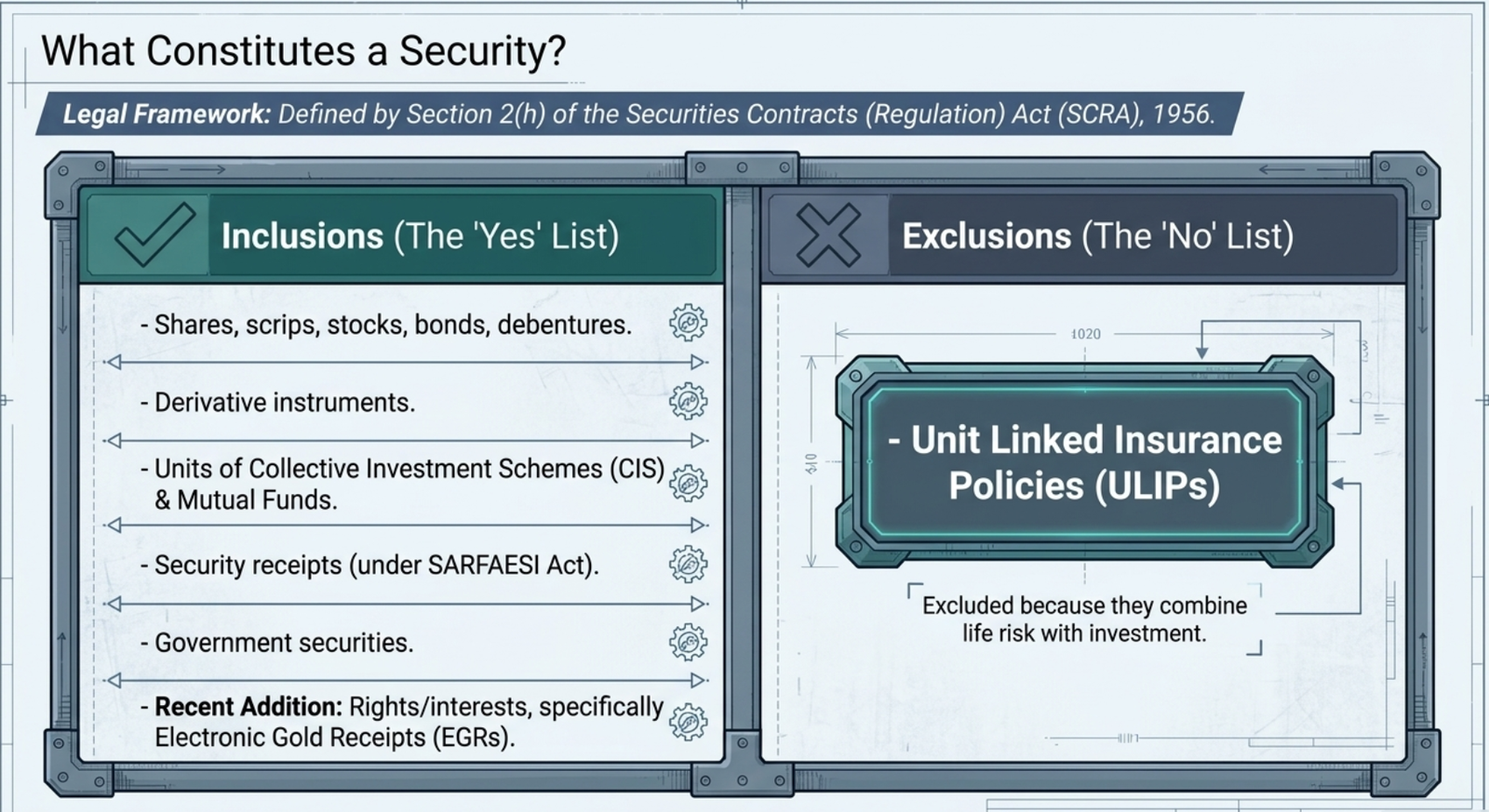

Legal Definition of Securities (Section 2(h) SCRA, 1956)

Complete Legal Definition as per Securities Contracts (Regulation) Act, 1956

The term "Securities" includes:

- Shares, scrips, stocks, bonds, debentures, debenture stock or other marketable securities of a like nature in or of any incorporated company or a pooled investment vehicle or other body corporate

- Derivative instruments - Financial instruments whose value is derived from underlying assets

- Units or any other instrument issued by any collective investment scheme to the investors in such schemes

- Security receipt as defined in clause (zg) of Section 2 of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002

- Units or any other such instrument issued to the investors under any mutual fund scheme

- Units or any other instrument issued by any pooled investment vehicle

- Any certificate or instrument (by whatever name called), issued to an investor by an issuer being a special purpose distinct entity which possesses any debt or receivable, including mortgage debt, assigned to such entity

- Government securities - Issued by central or state governments

- Such other securities as may be declared by the Central Government to be securities

- Rights or interest in securities - e.g., Electronic Gold Receipts (EGR) declared as securities vide gazette notification dated 24 December 2021

Important Exclusion - Explanation Clause:

Securities shall NOT include: Any unit linked insurance policy (ULIP) or scrips or any such instrument or unit, by whatever name called, which provides a combined benefit risk on the life of the persons and investment by such persons and issued by an insurer referred to in clause (9) of section 2 of the Insurance Act, 1938.

Recent Addition: Electronic Gold Receipts (EGR)

Electronic Gold Receipt means an electronic receipt issued on the basis of deposit of underlying physical gold in accordance with the regulations made by the Securities and Exchange Board of India under section 31 of the said Act.

Declared as securities: Vide gazette notification dated 24 December 2021

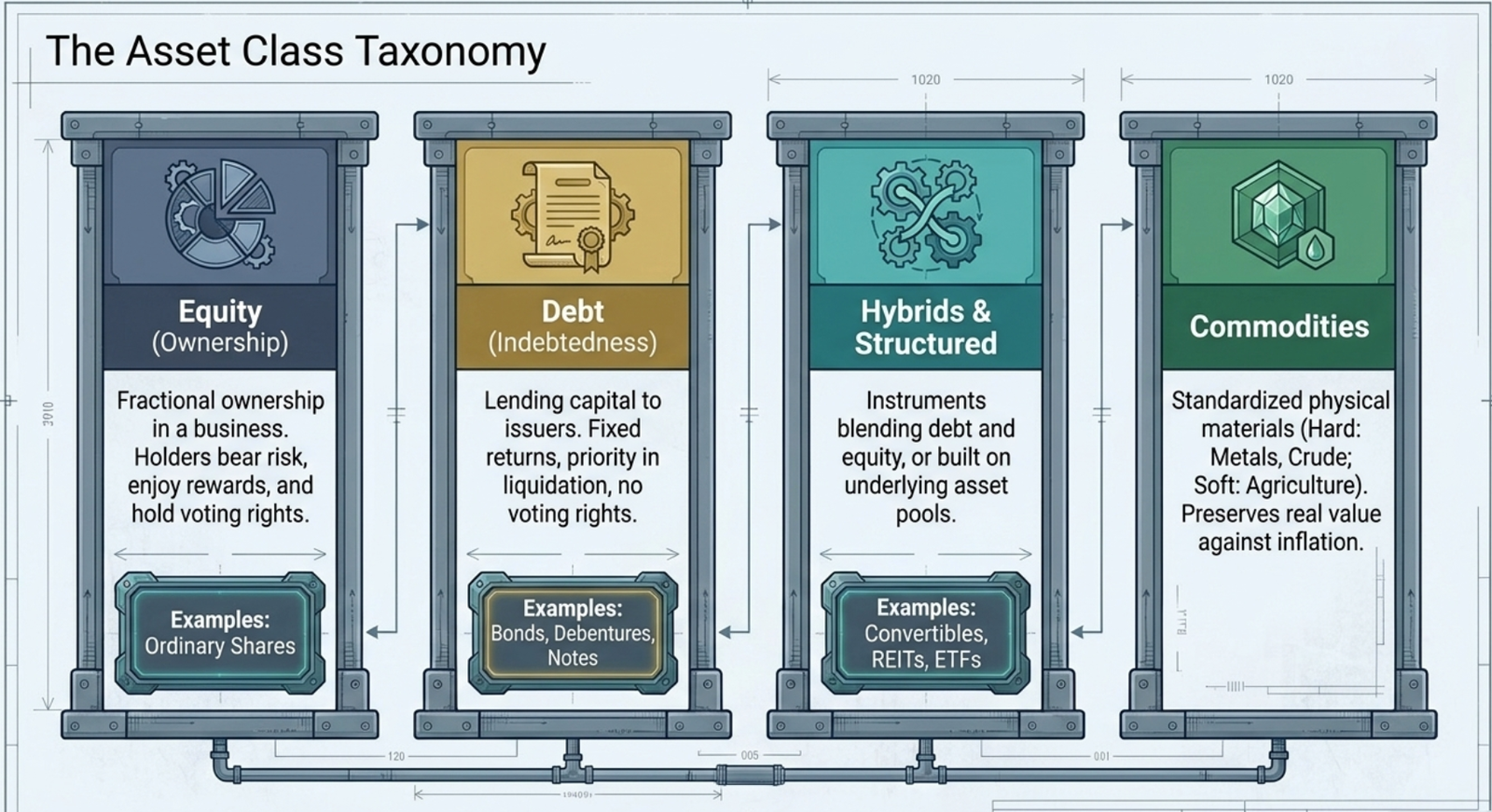

2.2 Product Definitions / Terminology - Comprehensive Coverage

The financial products available in Indian Securities Market can be categorized as equity, debt and derivative products, each with distinct risk and return characteristics.

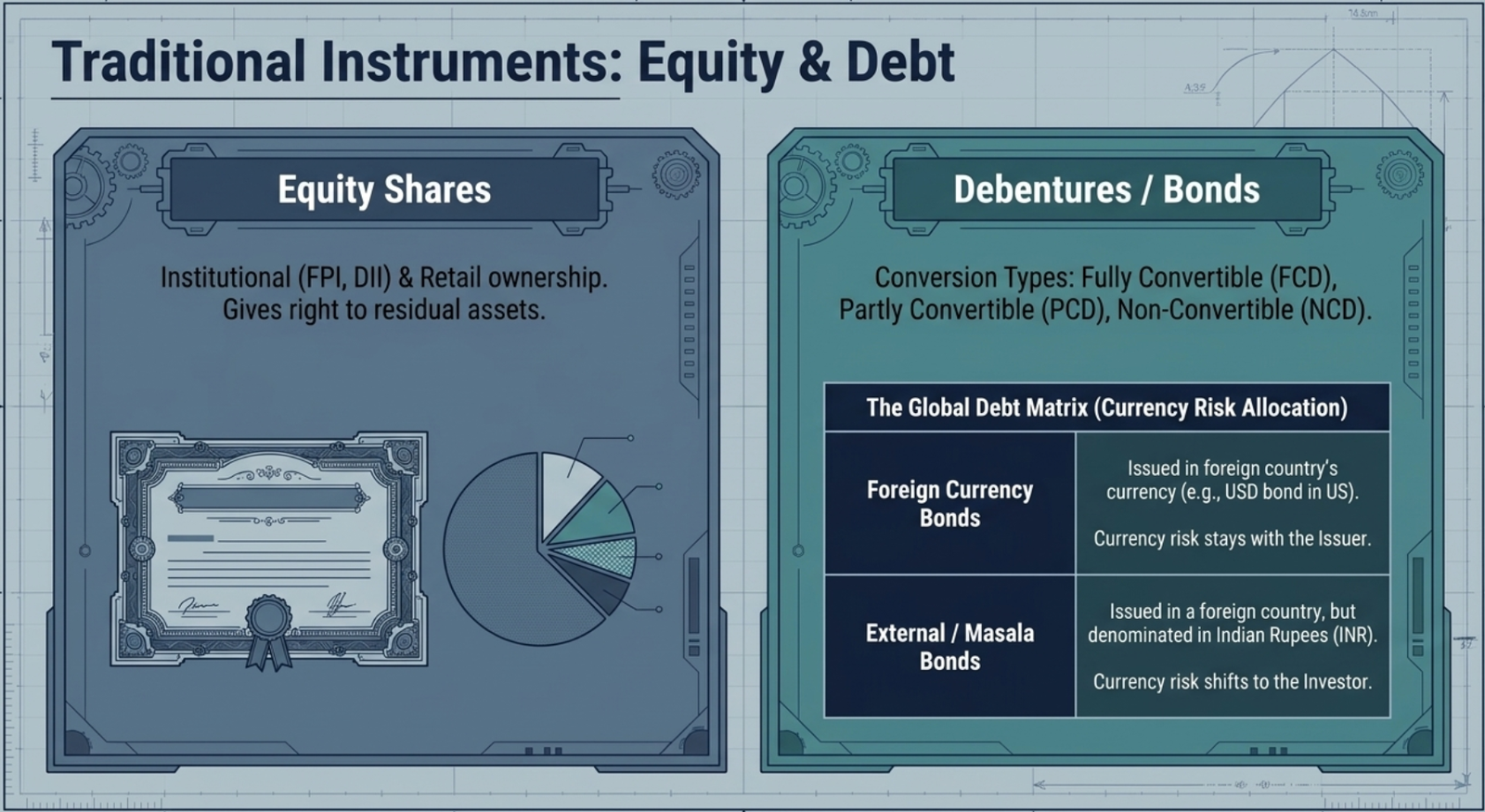

2.2.1 Equity Shares

Issued by: Companies or Issuers

Investors: Institutional (FPI, FII, DII) and Individual (Retail and HNI)

Medium: Direct issuance by companies and Stock Exchange

Regulator: SEBI, Regulators under the Companies Act

Key Features:

- Represents fractional ownership in a business venture

- Equity shareholders collectively own the company

- Bear risk and enjoy rewards of ownership

- Voting rights in company decisions

- Right to residual assets after debt obligations

2.2.2 Debentures/Bonds/Notes

Issued by: Companies, Government, Special Purpose Vehicles (SPVs), Other Issuers

Investors: Institutional and Individual

Medium: Direct issuance by issuers and Stock Exchange (If listed)

Regulator: RBI, SEBI, Regulators under the Companies Act

Types by Conversion Feature:

- Fully Convertible Debentures (FCD): Fully convertible into ordinary shares at specified terms

- Partly Convertible Debentures (PCD): Partly convertible into equity, non-convertible part redeemed

- Non-Convertible Debentures (NCD): Pure debt instruments, repayable on maturity

Security: Can be secured (backed by collateral) or unsecured

Currency: Available in domestic as well as foreign currency

2.2.2.1 Foreign Currency Bonds

Issued by: Companies, Government, SPVs

Currency Risk: Borne by issuer

Definition: Bonds issued by a company in a currency different from its home country currency

Example: Delhi International Airport Limited (GMR Infrastructure SPV) issued USD bonds in February 2020

Advantage: Access to lower interest rates in developed markets

Risk: Foreign currency appreciation increases repayment cost in local currency

2.2.2.2 External Bonds / Masala Bonds

External Bonds (Euro Bonds): Bonds issued in currency different from the country of issue

Masala Bonds: External bonds denominated in Indian Rupees (INR)

- First issued in November 2014 by International Finance Corporation

- Listed on London Stock Exchange

- Currency risk borne by investor (not issuer)

- If INR depreciates, investor receives less in local currency terms

2.2.3 Warrants and Convertible Warrants

Issued by: Companies

Regulator: SEBI

Definition: Options entitling investor to buy equity shares at pre-determined price after specified time period

Status: Only few companies in Indian Securities Market have issued warrants

Features: Similar to call options but issued by the company itself

2.2.4 Indices

Purpose: Track market movements using representative sample of stocks

Major Indian Indices:

- Nifty 50: 50 representative stocks on NSE

- S&P BSE Sensex: 30 stocks on BSE (market cap weighted)

- MSEI SX40: 40 stocks on Metropolitan Stock Exchange

- Other indices: Nifty Next 50, Nifty 100, Nifty 500, S&P BSE 100, BSE 500, BSE MidCap, BSE SmallCap

- Sector indices: Banking, IT, Pharma, FMCG, etc.

Selection Criteria: Liquidity, floating stock availability, market capitalization size

2.2.5 Mutual Fund Units

Issued by: Mutual Funds

Regulator: SEBI

Definition: Investment vehicles pooling money from investors to invest in portfolio reflecting common investment objectives

Unit Value: Net Asset Value (NAV) changes continuously with portfolio value

Types:

- Open-ended: Buy/sell units anytime at NAV-linked prices, no fixed maturity

- Close-ended: Fixed unit capital, specific number of units, mandatorily listed on stock exchange

2.2.6 Exchange Traded Funds (ETFs)

Issued by: Mutual Funds

Regulator: SEBI

Definition: Investment vehicle tracking an index, commodity (e.g., Gold) or basket of assets

Key Characteristics:

- Listed and traded in demat form on stock exchanges

- Real-time pricing throughout trading hours

- Diversification benefits of index fund + trading flexibility

- Lower expense ratios than traditional mutual funds (passive management)

- Can buy/sell even one unit at real-time prices

2.2.7 Hybrids/Structured Products - Comprehensive Coverage

2.2.7.1 Preference Shares

Definition: Special equity shares with preference over common equity in dividend payment and capital repayment during winding up

Equity-like Features:

- Holders are shareholders (not creditors)

- Payment termed as dividend (from Profit after Tax)

- Dividend payment not an obligation (unlike interest)

Debt-like Features:

- Pre-determined dividend rate

- No voting rights or right over residual assets

- Priority over common equity in liquidation

Types:

- Cumulative: Unpaid dividend carried forward

- Non-cumulative: Unpaid dividend lapses

- Convertible: Can be converted to equity (partly or fully)

2.2.7.2 Convertible Debentures & Bonds - Detailed

Definition: Debt instruments convertible into equity shares at predetermined terms

Types:

- Fully Convertible Debentures (FCD): Entire face value converted into equity

- Partly Convertible Debentures (PCD): Portion converted, remaining continues as debenture earning interest and redeemed at maturity

- Optionally Convertible Debentures (OCD): Conversion at discretion of debenture holders

Conversion Specifications (determined at issue):

- Date on which/before which conversion may be made

- Conversion ratio (number of shares per debenture)

- Share allotment price (usually at discount to market price)

- Proportion of debenture to be converted (for PCDs)

Advantages to Issuer:

- Lower coupon rate than pure debt (equity upside compensates)

- No debt repayment on maturity (shares issued instead)

Disadvantages to Issuer:

- Dilution of existing shareholders' stakes on conversion

Advantages to Investors:

- Coupon income during initial stage (company's nascent stage)

- Potential equity appreciation post-conversion

2.2.7.3 Depository Receipts - Comprehensive Coverage

Definition: Financial instruments representing shares of a foreign company, trading in local market and denominated in local currency

Process:

- Company/investor delivers specific quantity of equity shares to a bank

- Bank places security in custodian account in company's domiciled country

- Bank issues certificate (depositary receipt) against shares to investors in overseas market

Types by Sponsorship:

- Sponsored DRs: Company initiates process, can be listed on exchanges, must comply with listing requirements

- Unsponsored DRs: Investor delivers shares, typically OTC trading only, less regulatory requirements

Two-way Fungibility: Subject to regulatory provisions, shares can be converted to DRs and vice versa

Specific Types:

- American Depositary Receipts (ADRs): Issued by non-US company, traded in USA (Examples: Infosys, Wipro, ICICI Bank, HDFC Bank)

- Indian Depositary Receipts (IDRs): Issued by non-Indian company, traded in India (Example: Standard Chartered Bank)

- Hong Kong Depositary Receipts (HKDR): Non-Hong Kong company traded in Hong Kong

- Global Depositary Receipts (GDRs): Traded in multiple countries, often preferred in EU due to regulatory commonality

SEBI Guidelines for IDRs:

- Limit on money raised by company in India

- One year lock-in on conversion of IDRs into shares

- Availability to only resident Indian investors

Benefits:

- For Companies: Wider international investor base

- For Investors: Access to international stocks through domestic exchanges, local currency, existing brokers

- Rights: Dividends and capital appreciation, but typically no voting rights (under SEBI consideration)

2.2.7.4 Foreign Currency Convertible Bonds (FCCBs)

Definition: Foreign currency (usually USD) denominated convertible debt papers issued in international markets

Key Features:

- Generally optionally convertible

- Issued offshore under RBI guidelines

- Interest and principal repayment in foreign currency

- Post-conversion, dividend paid in INR (currency risk with investors)

Regulation: RBI notifications under FEMA, Issue of Foreign Currency Convertible Bonds and Ordinary Shares (Through Depository Receipt Mechanism), 1993

2.2.7.5 Equity Linked Debentures (ELDs)

Definition: Floating rate debt instruments whose interest is based on returns of underlying equity asset

Underlying Assets: Nifty 50, S&P Sensex, individual stocks, customized basket of stocks

Structure:

- Pre-determined part of principal invested in fixed income securities (principal protection)

- Balance used to buy options (equity exposure)

- Generally provides full capital protection with equity participation

Important: Capital Protection ≠ No credit risk. These instruments still carry credit risk of issuer default and are rated by credit rating agencies.

2.2.7.6 Commodity Linked Debentures (CLDs)

Definition: Floating rate debt instruments whose interest is based on returns of underlying commodity asset

Common Underlying: Precious metals (Gold and Silver) are most common globally

Advantage: Provides commodity market returns while protecting initial capital (similar to ELDs)

2.2.7.7 Mortgage Backed Securities (MBS) and Asset Backed Securities (ABS)

Definition: Debt instruments issued against receivables and cash flows from financial assets

Underlying Assets:

- MBS: Home loans

- ABS: Auto loans, rent receivables, credit card receivables, other financial assets

Process:

- Cash flows from underlying assets used for interest and principal repayment

- Issuer creates liquidity in otherwise illiquid assets through securitization

- Instruments are credit rated and may be listed on stock exchanges

2.2.7.8 REITs/InvITs

Real Estate Investment Trust (REITs): Investment vehicles pooling money to invest in revenue generating real estate projects

Infrastructure Investment Trusts (InvITs): Investment vehicles pooling money to invest in revenue generating infrastructure projects

Structure: Formed as trust, issue units to investors

Regulatory Requirements:

- REITs: 80% of assets in real estate assets

- InvITs: 90% of unit capital in revenue generating infrastructure projects

- Assets held directly or through Special Purpose Vehicle (SPV)

- Distribution: At least 90% of distributable surplus cash flow to unit holders

Tax Treatment: Favourable tax treatment as long as regulatory requirements are met

2.2.8 Commodities - Comprehensive Coverage

Example: A bar of gold is a commodity (homogenous), while gold jewellery is not (design preferences vary)

Hard Commodities

Natural resources that are mined or extracted

Examples: All types of metals, crude oil

Soft Commodities

Agricultural products that are grown

Examples: Grains, pulses

Investment Characteristics: Since inflation and commodity prices are directly related, investing in commodities can help protect real value of investment. However, most commodities involve huge storage costs and are thus not suitable direct investments.

2.2.8.1 Precious Metals

Investment Appeal: Gold and silver viewed as investments that preserve real value of money

Advantages:

- Very long life (unlike many other commodities)

- Storage cost very small compared to values

- These characteristics make precious metals viable investment options

2.2.8.2 Commodity ETFs

Definition: Exchange traded fund investing pooled investment in range of physical commodities

Investment Process:

- Investors buy units of the fund

- Unit value moves in line with NAV, which moves with commodity prices

- Storage handled by fund (no storage obligation for investors)

Most Common: Gold ETFs (easy to store and manage for the fund)

2.2.8.3 Managed Futures Contract

Futures Contract: Contract to buy or sell asset at specified future date at specific price

Managed Futures Contract: Portfolio of futures contracts actively managed by professionals

Investment Advantage:

- Buyer gains if price increases (predetermined price advantage)

- Gain from price rise without buying actual product

- Professional management of futures portfolio

- Investment managers take positions in futures instead of underlying assets

2.2.8.4 Warehouse Receipts

Definition: Document showing proof of ownership of goods stored in a warehouse

Key Features:

- Most warehouse receipts are negotiable

- Title to underlying goods can be transferred by transferring receipts

- Provides investment access to commodities without physical handling

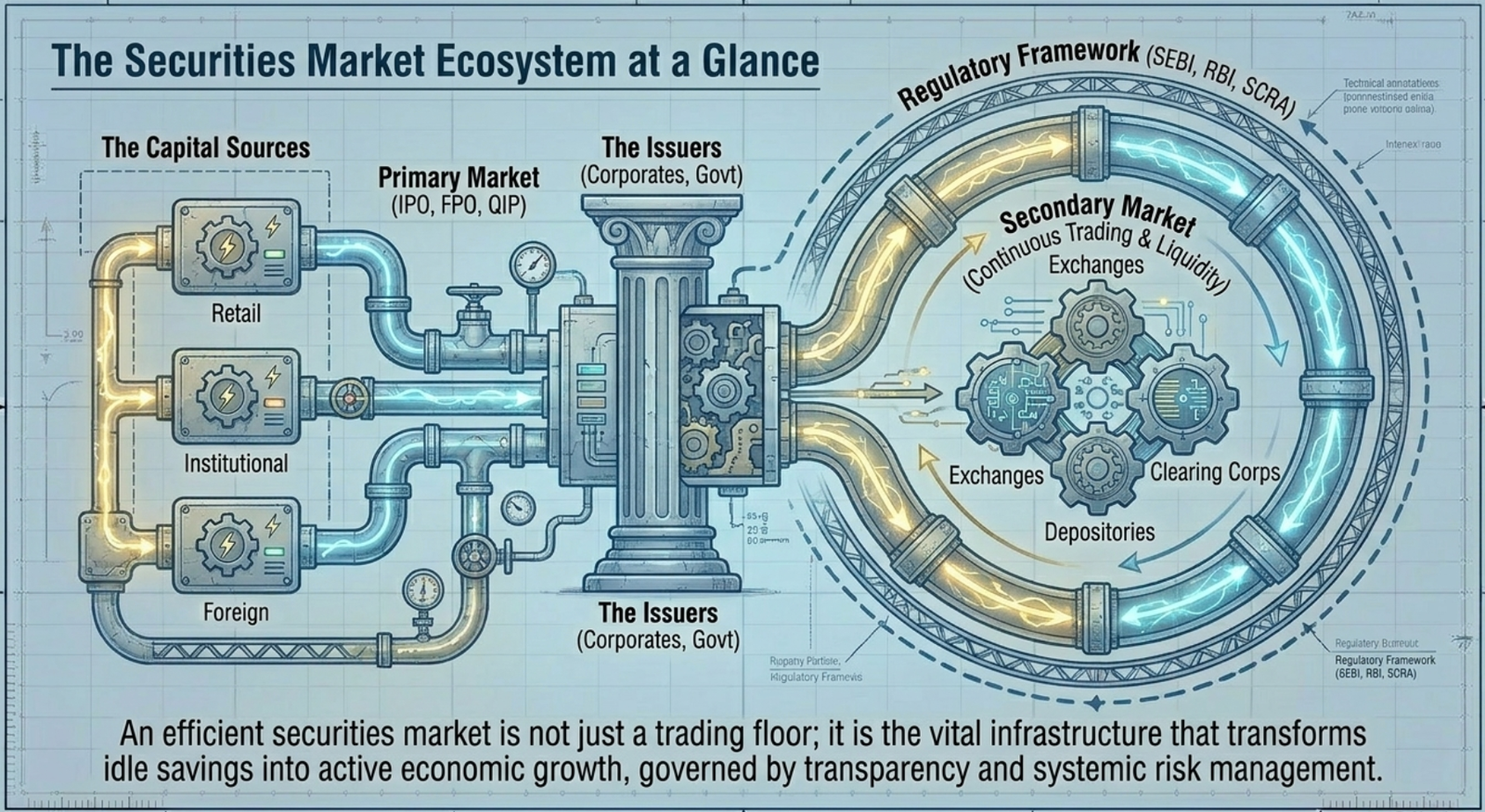

2.3 Structure of Securities Market - Complete Framework

Has two interdependent and inseparable segments: Primary Market and Secondary Market

Primary Market vs Secondary Market

(New Issue Market)

Fresh Capital Raising

(Trading Market)

Existing Securities Trading

Interdependence: Primary market facilitates creation of financial assets, secondary market facilitates their marketability/tradability

2.3.1 Primary Market - Comprehensive Coverage

Purpose: Used by companies (issuers) for raising fresh capital from investors

Types of Offerings: Public offering or private placement to select group of investors

Nature of Shares: May be new shares issued by company, or offer for sale where existing large investors/promoters offer portion of their holding

Complete Types of Primary Market Issues:

| Type | Description | Key Features & Requirements |

|---|---|---|

| Initial Public Offer (IPO) | First sale of corporate common shares to investors at large | • Main purpose: Raise equity capital for business growth • SEBI eligibility: Minimum net tangible assets, profitability, net-worth • Mandatory listing on nationwide stock exchange • Dematerialized form offering • Allocation: Min 35% to retail (≤₹2,00,000), Max 50% to QIBs |

| Anchor Investor Concept | QIB making application for ≥₹10 crore in book building IPO | • Introduced by SEBI in 2009 • Up to 60% of QIB portion • Bidding opens one day before public subscription • Price can be lower than final issue price • Volume/value serves as quality indicator |

| Follow-on Public Offer (FPO) | Already listed company's fresh issue or offer for sale to public | • Fresh issue: Additional capital for growth or capital structure redo • Offer for sale: Increase public shareholding for regulatory compliance |

| Private Placement | Issue large quantity of shares to select set of investors | • Companies Act 2013: Max 50 investors • Forms: QIP or Preferential allotment • Can be done regardless of prior public offer • Can be listed if meets requirements |

| Qualified Institutional Placements (QIPs) | Private placement by listed company to QIBs | • QIBs: Financial institutions, mutual funds, banks, etc. • SEBI defines eligibility criteria for corporates • Specific terms on quantum and pricing |

| Preferential Issue | Issue to select person/group on private placement basis | • Excludes: Public issue, rights, bonus, ESOP, ESPS, QIP, sweat equity, offshore DRs • SEBI compliance: Pricing, disclosures, lock-in + Companies Act requirements |

| Rights Issue | Securities offered to existing shareholders as on cut-off date | • Specific price for additional securities • Particular ratio to existing holdings • Options: (i) Exercise right (ii) Transfer right (iii) Let rights lapse |

| Bonus Issue | Free shares to existing shareholders without consideration | • In lieu of dividends • Requires sufficient retained earnings • Amount equal to share value transferred from retained earnings to share capital |

| Onshore vs Offshore Offerings | Capital raising location classification | • Onshore: Domestic market capital raising • Offshore: International investors capital raising |

| Offer for Sale (OFS) | Existing shareholders sell already allotted shares | • No increase in company share capital • Proceeds go to offerors (promoters/large investors) • Example: Government disinvestment in PSUs • Secondary market transaction via primary market route |

| Sweat Equity | Shares issued as reward for contribution (Sec.54 Companies Act 2013) | • Recipients: Employees, promoters, technocrats, others • Purpose: Motivate stakeholders, reduce agency risk • Not primarily for capital raising but involves new share issuance |

| Employee Stock Option Scheme (ESOPs) | Option to buy company shares at pre-determined price | • Vesting period: Typically >1 year + additional conditions • Employee gains only if share price > exercise price • Company issues shares if employee exercises option • Purpose: Align employee interests with company |

2.3.2 Secondary Market - Complete Framework

Purpose: Provides liquidity to instruments issued in primary market

Relationship: Active secondary market promotes primary market growth and capital formation by assuring investors of continuous market for liquidity/exit

Participants: Dealings between investors (issuers do not come into picture, unlike primary market)

Two Segments of Secondary Market:

Over-The-Counter Market (OTC Market)

Definition: Markets where trades are directly negotiated between two or more counterparties

Settlement: Securities traded and settled over the counter among counterparties directly

Risk Management: Counterparties expected to take care of credit risk on their own

Exchange Traded Markets

Definition: Trading and settlement done through stock exchanges

Settlement: Trades settled through clearing corporation

Guarantee: Clearing corporation acts as counterparty and guarantees settlement to both buyers and sellers

System: Electronic order-matching system for efficient and speedy execution

Trading

Definition: Formal contract to buy/sell securities

Venues: OTC market or Exchange Traded Market

Indian Exchanges: Feature electronic order-matching system for efficient and speedy trade execution

Clearing and Settlement - Detailed Process

Definition: Post trading activities constituting core part of equity trade life cycle

Clearing: Ascertaining net obligations of buyers and sellers for specific time period

Settlement: Next step of settling obligations by delivering shares (seller) and paying money (buyer)

OTC vs Exchange Settlement:

- OTC: Direct settlement between counterparties

- Exchange: Settlement through clearing corporation for all stock exchange trades

Clearing House Process:

- Stock exchange provides all transaction details to clearing house

- Clearing house gives obligation report to brokers and custodians

- Settlement of money/securities obligations within specified deadlines

- Penalties for non-compliance with deadlines

Novation: Clearing corporation provides full novation of contracts - acts as buyer to every seller and seller to every buyer, substantially reducing counterparty risk

Risk Management - Comprehensive Coverage

Exchange Trade Risk Management: Clearing corporation gives settlement guarantee but faces default risk from buyers/sellers

Margin Types:

- Initial/Upfront Margin: Percentage of transaction value based on "Value At Risk" philosophy

- Peak Margin: Additional margin requirements

- Mark-to-Market (MTM) Margin: Notional loss suffered by outstanding trade during specified period due to price movements

Purpose: Handle risk of default by market participants and ensure settlement guarantee integrity

2.4 Various Market Participants and Their Activities - Complete Coverage

Market Participants in Securities Market include buyers, sellers and various intermediaries between buyers and sellers.

2.4.1 Market Intermediaries - Comprehensive Coverage

Stock Exchanges

Function: Provide trading platform where buyers and sellers transact in already issued securities

Examples: NSE, BSE, MSEI (nationwide exchanges)

Features: Electronic trading terminals with anonymous order matching

Services: Appoint clearing and settlement agencies, clearing banks for funds and securities settlement

Depositories

Function: Hold securities in electronic form for investors

Securities Held: Shares, debentures, bonds, government securities, mutual fund units

India: NSDL (National Securities Depository Limited), CDSL (Central Depository Services Limited)

Access: Investors open accounts through registered Depository Participants

Services: Transaction services for dematerialized securities

Depository Participants (DP)

Role: Agent of depository interfacing with investors and providing depository services

Account Structure: Maintain investor-level accounts (company-level accounts maintained by depository)

Appointment: By depository with SEBI approval

Eligible Entities: Public financial institutions, scheduled commercial banks, foreign banks (with RBI approval), SFCs, custodians, stock-brokers, clearing corporations, NBFCs, RTAs (complying with SEBI requirements)

Trading Members/Stock Brokers

Role: Registered members of stock exchange facilitating buy/sell transactions

Requirement: All secondary market transactions must be conducted through registered brokers

Eligibility: Individuals (sole proprietor), Partnership Firms, Corporate bodies meeting minimum prudential requirements

Authorised Person

Definition: Person (individual, partnership firm, LLP or body corporate) appointed by stock broker as agent

Purpose: Reach investors scattered across country

Appointment: Prior approval from concerned stock exchange for each person

Approval: Specific to exchange segment

Evolution: Sub-brokers ceased to exist from April 01, 2019; migrated to Authorised Persons or Trading Members

Custodians

Clients: Large institutions (banks, insurance companies, foreign portfolio investors)

Functions:

- Safeguarding securities and funds

- Settling transactions in securities

- Tracking corporate actions

- Maintaining client securities and funds accounts

- Collecting benefits/rights accruing to clients

- Keeping clients informed of portfolio actions

Clearing Corporation

Role: Safeguard investor interests in Securities Market

Functions: Ensure exchange members meet obligations to deliver funds or securities

Guarantee: Act as legal counter party to all trades and guarantee settlement of all transactions

Structure: Can be part of exchange or separate entity

Clearing Banks

Role: Important intermediary between clearing members and clearing corporation

Requirement: Every clearing member maintains account with clearing bank

Pay-in: Clearing member ensures funds availability on pay-in day for trade obligations

Pay-out: Clearing member receives amount in clearing bank account on pay-out day

Merchant Bankers

Registration: SEBI registered entities

Roles: Issue managers, investment bankers, lead managers

Service: Help issuers access security market with securities issuance

Functions:

- Single point contact during new issues

- Evaluate capital needs of issuers

- Structure appropriate instruments

- Pricing the instrument

- Manage entire issue process until listing

- Coordinate with other intermediaries

Underwriters

Role: Subscribe unsubscribed portion of public offers

Function: Provide comfort to issuers that securities will be bought if public demand insufficient

Types:

- Hard Underwriting: Commitment at initial IPO stages

- Soft Underwriting: Commitment after pricing determination, includes exit option for certain events

Risk Management: Devolved shares usually placed with other financial institutions

2.4.2 Institutional Participants - Comprehensive Coverage

Definition: Backbone of securities market lending surplus resources to companies for productive activities

Classification: Retail Investors and Institutional Investors

Domestic Institutional Investors:

Mutual Funds

Definition: Professionally managed collective investment scheme pooling money from many investors to purchase securities

Investment: Stocks, bonds, and other securities based on stated investment objective

Management: Fund manager with research team takes major decisions (companies, percentage allocation, exit timing)

Ownership: Each investor owns units representing portion of fund holdings

Diversification: Important aspect reducing investment risk - less likely to lose money on all investments simultaneously

Insurance Companies

Core Business: Ensure assets (life insurance, general insurance, etc.)

Investment Corpus: Huge corpus making them important investors in Indian economy

Investment Areas: Equity investments, government securities, other bonds

Decision Making: Designated investment decision personnel (similar to mutual funds)

Pension Funds

Purpose: Facilitate and organize investment of retirement funds

Contributors: Employees and employers (or only employees in some cases)

Objective: Common asset pool for stable long-term growth, providing retirement income

Management: Usually run by financial intermediary for company and employees; larger corporations may operate in-house

Capital Control: Relatively large capital amounts, among largest institutional investors

Venture Capital Funds

Definition: Pooled investment vehicle investing in early stage development enterprises with long-term growth potential

Target Companies: Longer gestation period, higher failure risk, difficult conventional finance access

Value Addition: Venture capitalists bring managerial and technical expertise along with capital

Private Equity Firms

Definition: Funding for companies in early growth stages, expansion, or buy-outs

Target: Privately held or publicly traded companies

Inclusion: Term includes venture capital firms

Structure: Limited partners contribute money, general partners invest and manage

Specialization: Some funds specialize in particular industry, company stage, or targeted deals (buyouts)

Hedge Funds

Definition: Investment vehicle pooling capital from investors, investing across assets, products, and geographies

Mandate: Very wide mandate to generate returns on invested capital

Strategy: Hunt for opportunities to make money wherever possible

Note: Term "hedge fund" is misnomer as these funds may not necessarily be hedged

Alternative Investment Funds (AIFs) - Complete Framework

Definition (SEBI AIF Regulations 2012): Privately pooled investment fund (Indian or foreign sources) in form of trust, company, body corporate, or LLP not covered by other SEBI fund management regulations or sectoral regulators (IRDAI, PFRDA, RBI)

Investment Areas: Real estate, private companies, commodities, other alternative assets (excluding listed equities, fixed income, fixed deposits, collective investment schemes like mutual funds, NPS, insurance)

SEBI Categories:

- Category I AIF: Invest in start-ups, early-stage ventures, social ventures, SMEs, infrastructure, socially/economically desirable sectors. Includes venture capital funds (including angel funds), SME Funds, social venture funds, infrastructure funds

- Category II AIF: Don't fall in Category I & III, don't undertake leverage/borrowing (except day-to-day operational requirements). Includes real estate funds, private equity funds, distressed asset funds

- Category III AIF: Use complex investment strategies including leverage and derivatives. Includes hedge funds, PIPE Funds

Employee Provident Fund (EPF)

Purpose: Provide retirement benefits through defined benefit schemes

Contribution: Employer provides 12% of basic salary, equal amount deducted from employee salary

Administration: Funds deposited with Employees' Provident Fund Organisation (EPFO)

Returns: Pre-determined annual interest rate decided yearly

Investment: Debt and equity instruments (employees have no say in investments or asset allocation)

National Pension Scheme (NPS)

Nature: Government sponsored retirement scheme

Process: Regular subscriber contributions, maturity funds used to buy annuity products

Withdrawal: Option to partially withdraw funds at maturity

Corporate NPS: Offered by employers in addition to other retirement benefits

Choice: Various fund choices, beneficiaries can route to fund of their choice

Family Offices

Definition: Organisation handling wealth of wealthy family

Services: All aspects of financial management including investments, estate planning, tax planning

Operations: Day-to-day accounting, income/expense management, vendor payments, household staff payments

Types: Single family offices, Multifamily offices (handle multiple families)

Corporate Treasuries

Purpose: Handle surplus funds for future opportunities or obligations

Rationale: Temporary investment better than idle funds in current accounts

Organization: Large corporates have separate treasury teams; smaller businesses use regular finance teams

Investment Options: Larger treasuries access various securities types; smaller businesses mostly use mutual funds

Foreign Institutional Investors:

Foreign Portfolio Investors (FPIs)

Definition: Entity established or incorporated outside India proposing to make investments in India

Registration: Must register with SEBI to participate in Indian Securities Market

P-Note Participants

Participatory Notes (P-Notes/PNs): Instruments issued by SEBI registered foreign portfolio investors to overseas investors

Purpose: Allow investment in Indian stock markets without registering with SEBI

Access: Provide access to Indian securities for these investors

Investment Advisers

Services: Work with investors on asset allocation and investment choices

Assessment Basis: Investor needs, time horizon, return expectation, risk bearing ability

Financial Planning: Help define financial goals, propose appropriate saving and investment strategies

2.4.3 Retail Participants

Retail Investors: Individual investors buying and selling securities for personal account (not for another company or organization)

HNIs/UHNIs: High/Ultra High Net-worth Individuals investing large sums

International Retail: NRIs (Non Resident Indians), PIOs (Persons of Indian Origin), QFIs (Qualified Foreign Investors) can undertake direct investments under RBI Automatic Route

2.4.4 Proxy Advisory Services Firms

Function and Value Addition

Services: Advise investors on exercise of rights in company including public offer recommendations and voting recommendations on agenda items

Need: Investors may not track shareholder announcements of all investee companies or analyze each proposal in depth

Process: Analyze voting proposals, assess impact on investor interests, suggest voting decisions

Client Base: Typically engaged by institutional investors for voting matters

🏛️ Analyze Real Market Participants & Their Portfolios

You've just learned about FPIs, DIIs, mutual funds, and other market participants. Now analyze their actual holdings and investment patterns!

📊 FPI/DII Holdings Analysis

Track real institutional holdings across our 71+ company reports:

- Foreign Portfolio Investor holdings

- Domestic Institutional Investor data

- Mutual Fund investments by scheme

- Quarterly trend analysis

🏢 Corporate Action Tracking

Monitor real market events as they happen:

- Rights Issues & Bonus announcements

- IPO analysis and recommendations

- Stock splits and dividend tracking

- QIP and OFS impact analysis

Real Data, Real Insights: Practice analyzing the same participants you're studying in NISM with live market data!

2.5 Kinds of Transactions - Complete Coverage

Securities market transactions range from immediate settlement to distant settlement, varying based on stock market or OTC trades.

2.5.1 Cash, Tom and Spot Trades/Transactions

| Transaction Type | Settlement Cycle | Description & Examples |

|---|---|---|

| Cash Trades | T+0 | Settlement on same trading day. Unusual in financial markets though Indian stock exchanges gradually moving to this for all stocks. Common in daily life (groceries, vegetables, fruits) |

| Tom Trades | T+1 | Settlement on day next to trading day. Some Foreign Exchange Market transactions settle on T+1 basis. Indian equity markets moving towards this cycle |

| Spot Trades | T+2 (Spot Date) | Settlement normally two business days after trade date. Current norm for Indian equity markets. FX markets globally offer spot transactions by default |

2.5.2 Forward Transactions - Detailed

Characteristics: Both parties committed and obliged to honour transaction irrespective of underlying asset price at settlement. Terms and conditions customized between parties. Over-the-counter (OTC) contracts.

Example: Agricultural Forward Contract

Farmer agrees to sell wheat produce to miller 6 months later when crop ready, at price both agree today.

Settlement Terms (decided at contract time):

- Quantity and quality of wheat

- Price and payment terms

- Reference benchmark for cash settlement

Counterparty Risk: If either party fails to honour contract. Generally entered between known parties using informal protection mechanisms. Forward markets in several parts of India based on mutual trust despite risks.

2.5.3 Futures - Exchange Traded Forwards

Exchange Features: Traded and settled on stock exchange with clearing corporation settlement guarantee. Subject to stringent margin requirements. Available on equities, equity indices, commodities, currencies, interest rates.

Example: MCX Wheat Futures Specifications

- Trading unit: 10MT

- Minimum order size: 500MT

- Maximum position per individual: 5000 MT

- Quality: Standard Mill Quality as specified by exchange

- Contract begin date: 21st of the month

- Delivery options: Physical delivery only

- Delivery date: 20th of the month

- Delivery centre: Exchange approved warehouses

2.5.4 Options - Detailed Coverage

Participants: Buyer/holder pays premium and buys right. Writer/seller receives premium with obligation to sell/buy underlying asset if buyer exercises right.

Call Option

Gives buyer right (not obligation) to BUY given quantity of underlying asset at given price on or before given future date

Put Option

Gives buyer right (not obligation) to SELL given quantity of underlying asset at given price on or before given date

Comprehensive Example: Nifty 50 Call Option

Scenario: Arvind buys call option on Nifty 50 from Salim to buy Nifty 50 at 11000, three months from today, paying ₹100 premium.

Key Terms:

- Arvind: Buyer of call option

- Salim: Seller/writer of call option

- Contract timing: Entered today, completed three months later on settlement date

- Strike/Exercise price: 11000 (price Arvind willing to pay for Nifty 50)

- Option premium: ₹100 (upfront payment from Arvind to Salim)

Settlement Scenarios:

- Nifty at 11200: Option "in the money" - Arvind exercises, buys at 11000 when market is 11200. Salim earns ₹100 premium but loses on obligation (sells at 11000 vs market 11200)

- Nifty at 10800: Option "out of the money" - No point paying 11000 when market is 10800. Arvind won't exercise, option expires worthless. Salim pockets ₹100 premium

Trading Venues: Options can be transacted in both OTC Market and Exchange Traded Markets

2.5.5 Swaps - Comprehensive Coverage

Purpose: Help market participants manage risks associated with volatile interest rates, currency rates, and commodity prices.

Detailed Example: Interest Rate Swap

Problem: Borrower has quarterly floating rate interest (T-bill rate + spread) but prefers fixed rate payment.

Swap Arrangement:

- Pay fixed rate to swap dealer every quarter

- Receive T-bill plus spread from swap dealer every quarter

Mechanism:

- Notional principal amount agreed (no principal exchange, only interest)

- Borrower receives floating rate from swap dealer

- Uses received floating rate to pay floating rate dues on borrowing

- Net obligation: Fixed interest rate payment to swap dealer

- Result: Floating rate borrowing converted to fixed rate obligation

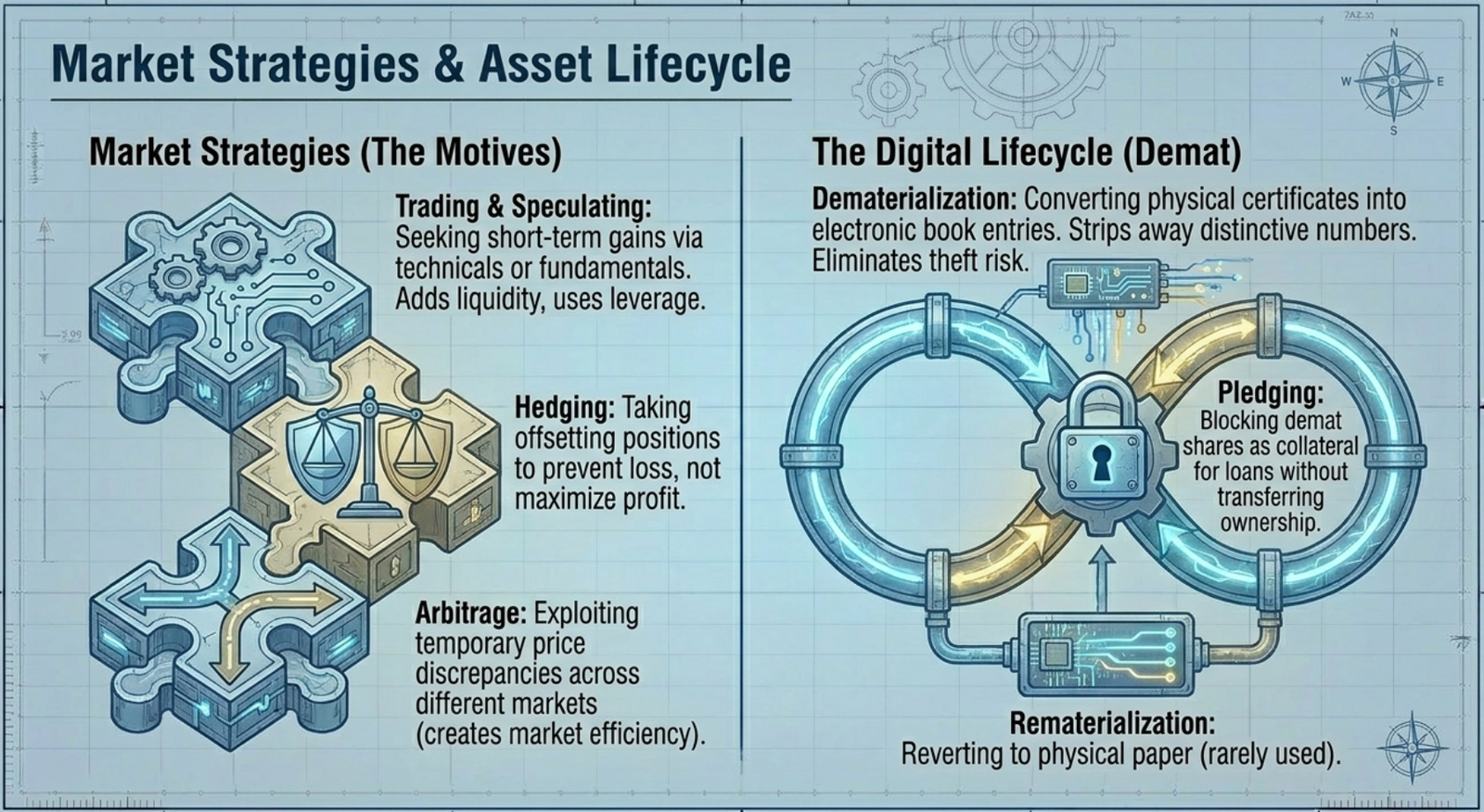

2.5.6 Trading, Hedging, Arbitrage, Pledging of Shares - Complete Coverage

Trading/Speculation

Definition: Purchase or sale of asset expecting gain from short-term price changes

Purpose: Benefit from acting on information causing price changes

Market Impact: Actions increase market liquidity

Leverage: Typically use borrowed funds, magnifying gains and losses

Hedging

Definition: Taking position to offset potential losses from another position

Instruments: Insurance, forward/futures contracts, swaps, options

Effect: Hedged position limits loss and gains (appreciation in one position offset by depreciation in other)

Arbitrage

Definition: Simultaneous purchase and sale of asset to profit from price discrepancies in different markets

Example: Buy stock in spot market, simultaneously sell in futures market for price differential profit

Efficiency: In efficient markets, arbitrage opportunities exist only briefly or not at all

Market Impact: Buying in lower-priced market raises prices, selling in higher-priced market lowers prices, eliminating arbitrage opportunity

Pledging of Shares

Definition: Taking loan against securities by investor

Parties: Pledgor (investor), Pledgee (loan provider)

Mechanism: Dematerialized securities pledged/hypothecated for loan/credit facility

Security State: Pledged securities remain in pledgor's demat account but blocked for other transactions

Resolution: Unpledging after obligation fulfillment; pledgee can invoke pledge on default

2.6 Dematerialization and Rematerialization of Securities - Complete Process

Dematerialization (Demat) - Comprehensive Coverage

Key Feature: In demat form, one investor's shares not distinguished from another investor's shares - no distinctive numbers, folio numbers, or certificate numbers.

SEBI Regulatory Requirements:

- Companies making public issue must enter agreement with all depositories

- Must dematerialize shares to give investors option of holding in dematerialized form

- Mandatory enablement for public issue companies

Benefits of Dematerialization:

- Eliminates risks of loss, theft, forgery of physical certificates

- Faster settlement and transfer processes

- No distinctive numbers or certificate management required

- Easier corporate action processing

- Reduced paperwork and administrative burden

- Electronic record keeping and tracking

Process and Infrastructure:

Depositories: NSDL and CDSL hold company-level accounts of issued securities

Depository Participants: Maintain investor-level accounts in securities

Interface: DPs provide interface between depositories and investors for demat services

Rematerialization (Remat) - Reverse Process

Process: On investor request, securities on rematerialization are allotted in physical form with distinctive numbers, replacing securities held electronically in book-entry form with depository.

Practical Note: Most investors prefer to keep securities in demat form due to convenience, safety, and efficiency benefits. Rematerialization is rarely requested except for specific requirements.

🃏 Flashcards

Click any card to reveal the answer. 68 cards covering the full chapter.

Comprehensive Test Your Understanding

Question 1: As per Section 2(h) of SCRA, which of the following is NOT included in the definition of securities?

Question 2: In Masala bonds, the currency risk is borne by:

Question 3: The clearing corporation provides which of the following in exchange traded markets?

Question 4: Which category of AIF uses complex investment strategies including leverage and derivatives?

Question 5: In REITs, what percentage of assets must be held in real estate assets?

Question 6: What is the settlement cycle for Tom trades?

Comprehensive Key Takeaways from Chapter 2

- Legal Framework: Securities defined comprehensively under Section 2(h) SCRA including shares, derivatives, mutual fund units, government securities, and Electronic Gold Receipts (excluding ULIPs)

- Market Structure: Two interdependent segments - Primary Market (fresh capital raising) and Secondary Market (existing securities trading) with various sophisticated mechanisms

- Comprehensive Product Range: Equity shares, various debenture types, foreign currency bonds, Masala bonds, warrants, depository receipts, REITs/InvITs, commodity investments, and structured products

- Advanced Instruments: FCCBs, ELDs, CLDs, MBS/ABS providing specialized risk-return profiles for different investor needs

- Primary Market Mechanisms: IPOs with anchor investors, FPOs, QIPs, preferential issues, rights/bonus issues, ESOPs, sweat equity, OFS with specific regulatory frameworks

- Secondary Market Infrastructure: OTC vs Exchange trading, comprehensive clearing and settlement with novation, sophisticated risk management through multiple margin types

- Extensive Participant Ecosystem: Market intermediaries (exchanges, depositories, DPs, brokers, custodians), institutional investors (domestic and foreign), retail participants, and specialized service providers

- Alternative Investment Landscape: Three categories of AIFs, pension funds, venture capital, private equity, hedge funds, family offices, corporate treasuries

- Transaction Sophistication: Multiple settlement cycles, derivative instruments (forwards, futures, options, swaps), and specialized transaction types (trading, hedging, arbitrage, pledging)

- Technological Infrastructure: Dematerialization enabling electronic securities holding, eliminating physical certificate risks and enabling efficient settlement

- International Integration: Foreign investment frameworks (FPIs, P-Notes), cross-border instruments (ADRs, GDRs, IDRs), currency risk management

- Risk Management Framework: Clearing corporation guarantees, margin systems, counterparty risk mitigation, and settlement assurance mechanisms

Continue Your Learning Journey

You've completed the comprehensive Chapter 2! This enhanced version includes all NISM workbook content plus detailed explanations. Here's what comes next:

- Chapter 3: Terminology in Equity and Debt Markets

- Chapter 4: Fundamentals of Research

- Chapter 5: Economic Analysis