📑 Chapter Navigation

DCF Models

Relative Valuation

Assessment & Practice

📖 Complete Course Navigation

Foundation (Ch 1-4)

Analysis (Ch 5-8)

Advanced (Ch 9-13)

Annexures (Ch 14-16)

📚 Learning Objectives

After studying this chapter, you should know about:

- Need for business valuations and sources of value in a business

- Various approaches to valuation

- Different types of business valuation models

- Objectivity of valuations and important considerations in business valuation

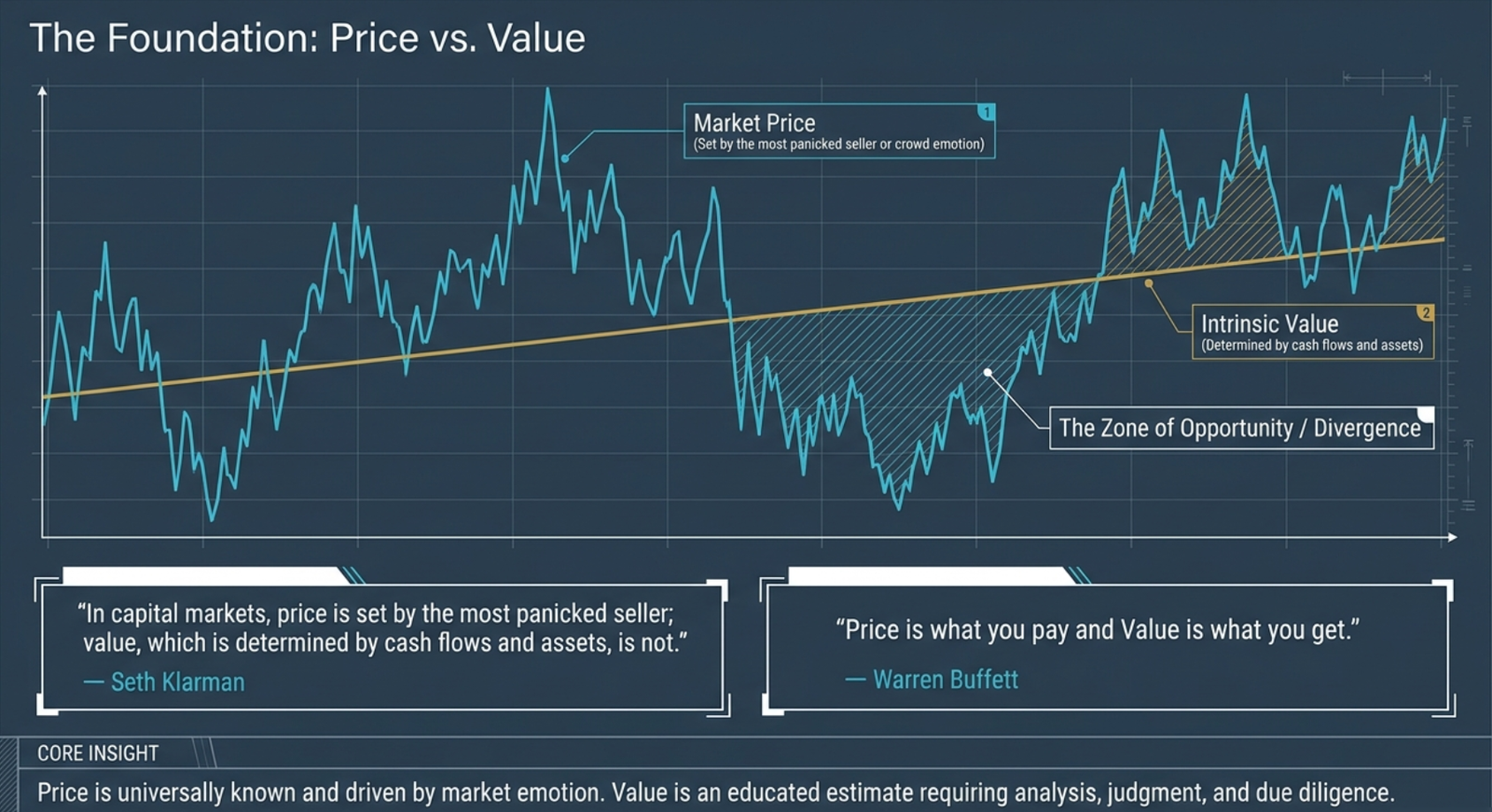

10.1 Difference between Price and Value

Mr. Seth Klarman, a known value investor stated: "In capital markets, price is set by the most panicked seller; value, which is determined by cash flows and assets, is not. This is both the challenge and the opportunity of investing: to carefully sift through the markets to find the greatest divergence between price and value, and to concurrently avoid the extreme emotions of the crowd and, indeed, to take a stand against them."

Warren Buffett is also known to state frequently: "Price is what you pay and Value is what you get."

Price and value are two different concepts in investing. While price is available from the stock market and known to all, value is based on the evaluation and analysis of the valuer at a point in time.

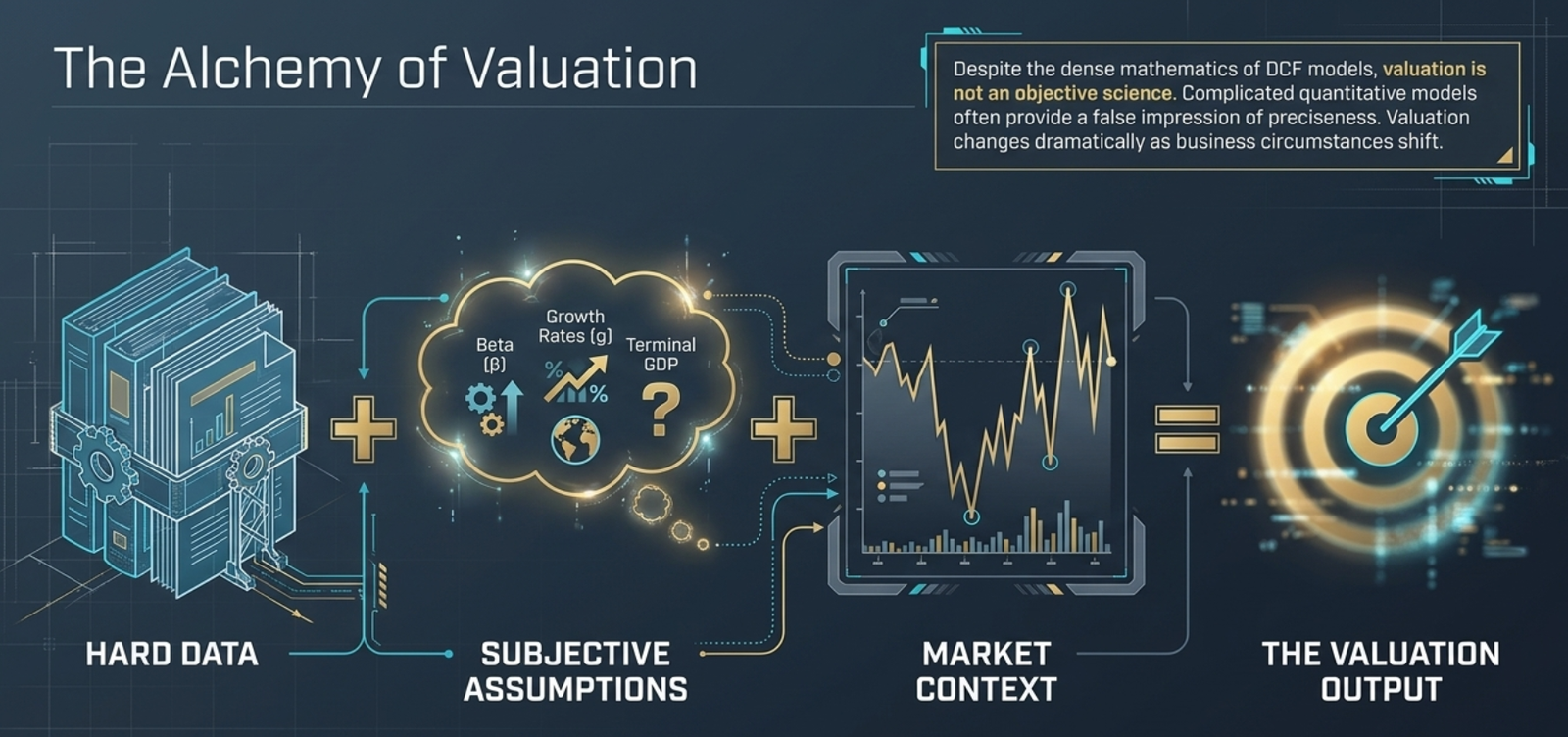

There is no formula or method to put to throw a precise number on valuation of an asset. There are uncertainties associated with the inputs that go into the valuation process. As a result, the final output can at best be considered an educated estimate, provided adequate due diligence associated with valuing the asset has been complied with. That is the reason, valuation is often considered an art as well as a science. It requires the combination of knowledge, experience and professional judgment in arriving at a fair valuation of any asset.

10.2 Why Valuations are required

While purpose of carrying out valuation could vary from person to person, some of the reasons for carrying out valuations of assets/businesses/liabilities are as follows:

- Buying a business as part of investment exercise

- Selling a business as part of investment exercise

- Mergers and Acquisitions

- General sense of value of business to owners

- Fair treatment to different set of stake holders in case of equity swap

- Accounting, taxation and other regulatory and legal requirements

Whatever may be the objective of valuation, the purpose of valuation is to relate price to value and estimate if it is fairly priced, over-priced or under-priced. Given the limitations in the valuation process, valuers typically present multiple scenarios that reflect the effect of a change in the primary variables on the output value.

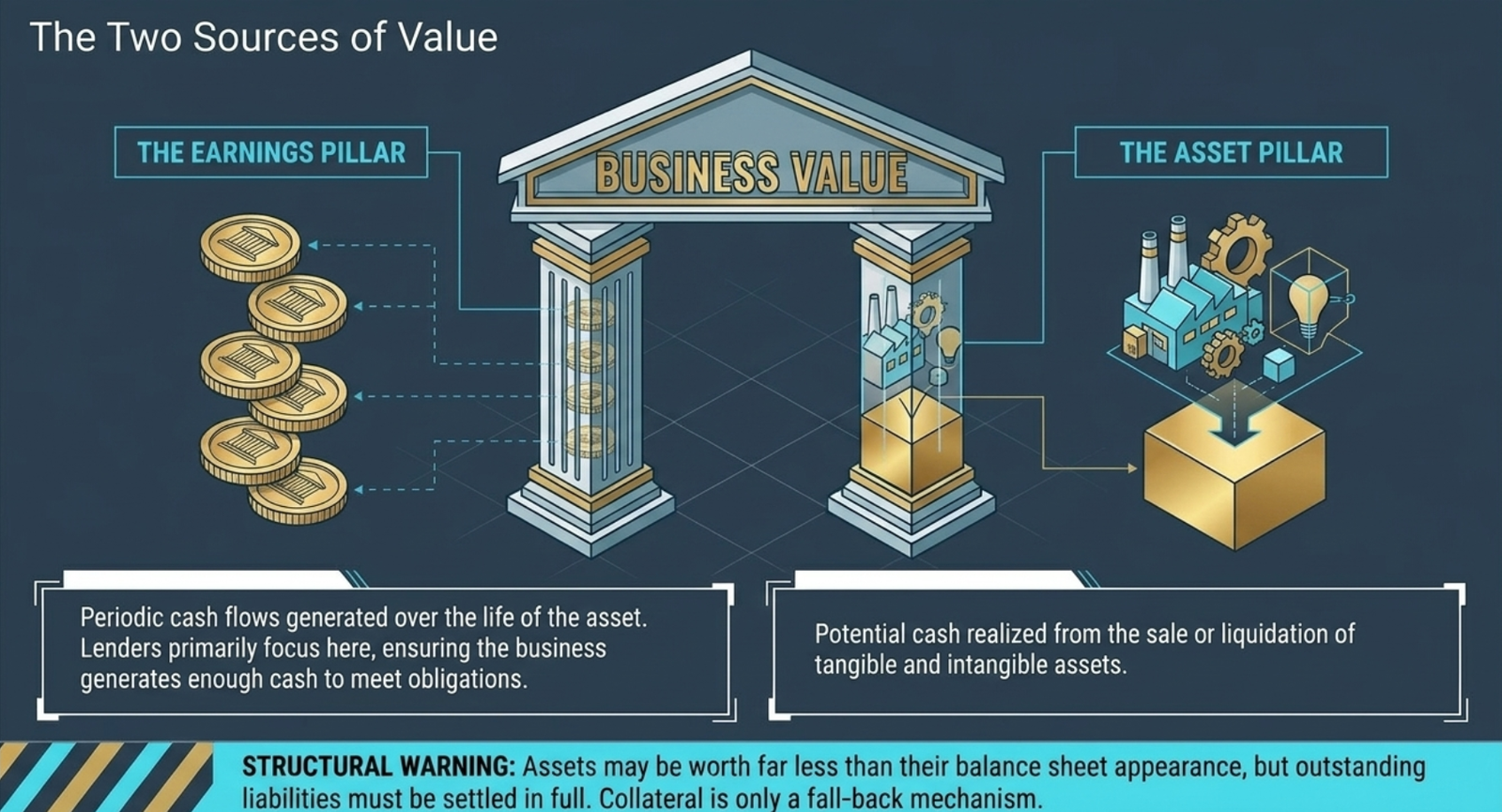

10.3 Sources of Value in a Business – Earnings and Assets

Warren Buffett stated: "There are only two sources of value in a business - Earnings and Assets". Any asset, whether a financial asset such as a stock or a bond, or a real asset generates two streams of cash flows - periodic earnings and a final inflow on sale of the asset.

- In case of bonds, coupons produce earnings and redemption/sale of bond in the market produces one-time cash flow

- Equities also produce earnings in the form of dividends and then onetime cash flows on sale

- Real estate provides rental income and an appreciated capital value on sale

Important Note: The capability of the business assets to pay up all liabilities and settle the equity holders is always doubtful. Assets may be worth a lot less than what they appear for in the balance sheet. But the outstanding liabilities have to be settled in full.

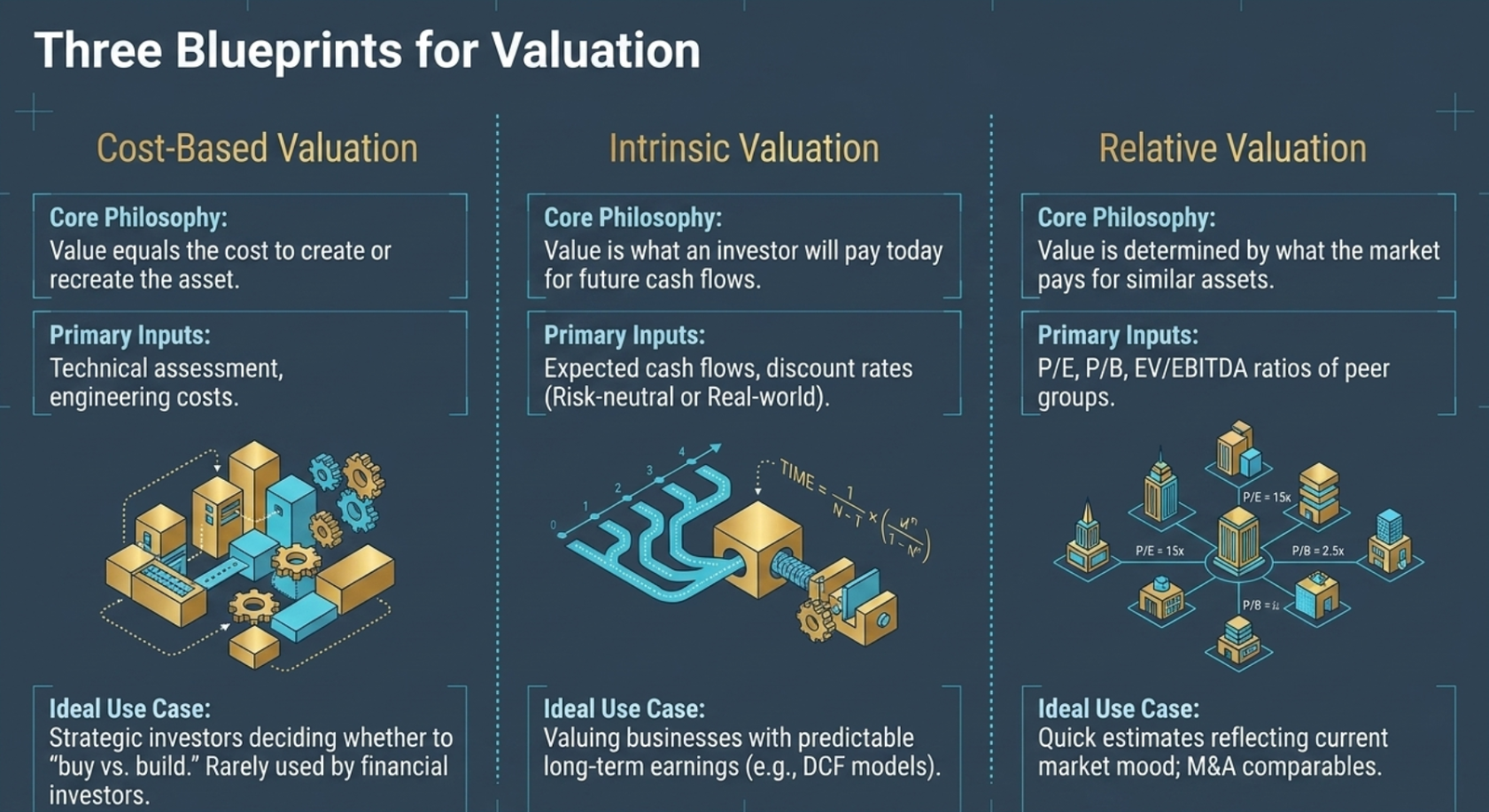

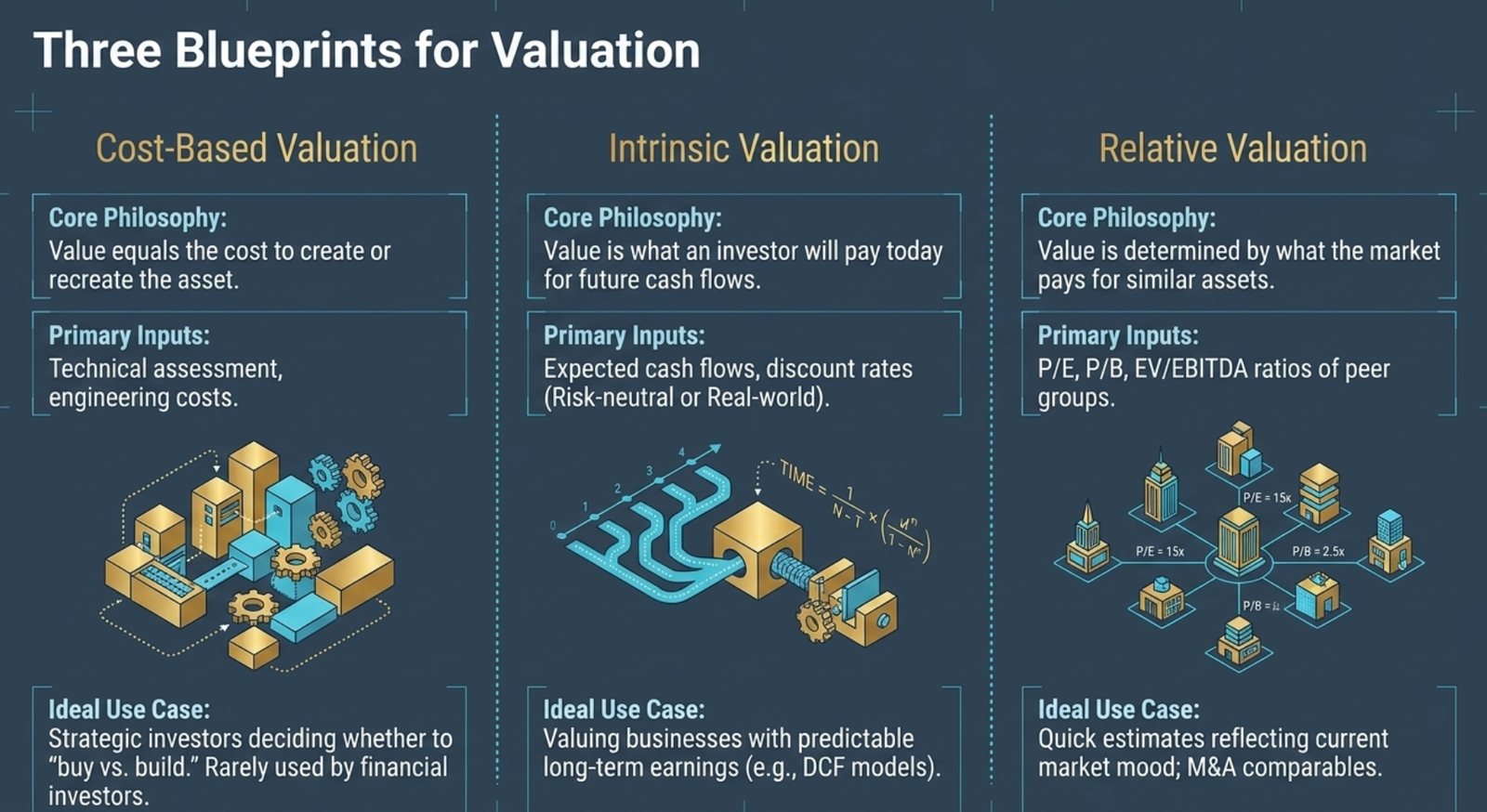

10.4 Approaches to valuation

Asset valuation can be broadly classified into three categories:

1. Cost based valuation

Under this approach, an asset is valued based on the cost that needs to be incurred to create it. This option is suitable only for a buyer who has choice between buying versus making. Most investors in the stock market typically do not have a choice to build and run a company on their own. Hence, this approach is generally not suitable for financial investors. However, strategic investors, who intend to carry on the business into the long term may consider using this approach.

2. Cash flow based valuation (intrinsic valuation)

Intrinsic valuation approach assigns value to an asset based on what an investor would be willing to pay for the cash flow generated by the assets. This approach typically involves valuing an asset by discounting its cash flow at a suitable rate that reflects the rate of return expected by an investor.

Intrinsic valuation can be divided into two categories:

- Risk neutral valuation: It involves adjusting the cash flows by the probability of realising the cash flow. It is then discounted at risk free rate. Insurance companies are typically valued using this approach (embedded value and appraisal value).

- Real world valuation: It involves estimating the most likely cash flow and discounting it at a rate of return that reflects the risk free rate plus a suitable risk premium to account for the uncertainty in the cash flows.

3. Selling price based approach (relative valuation)

Under this approach an asset is valued based on the price of other similar assets. Various valuation ratios such P/E, P/B, EV/EBITDA can be used as the valuation metric.

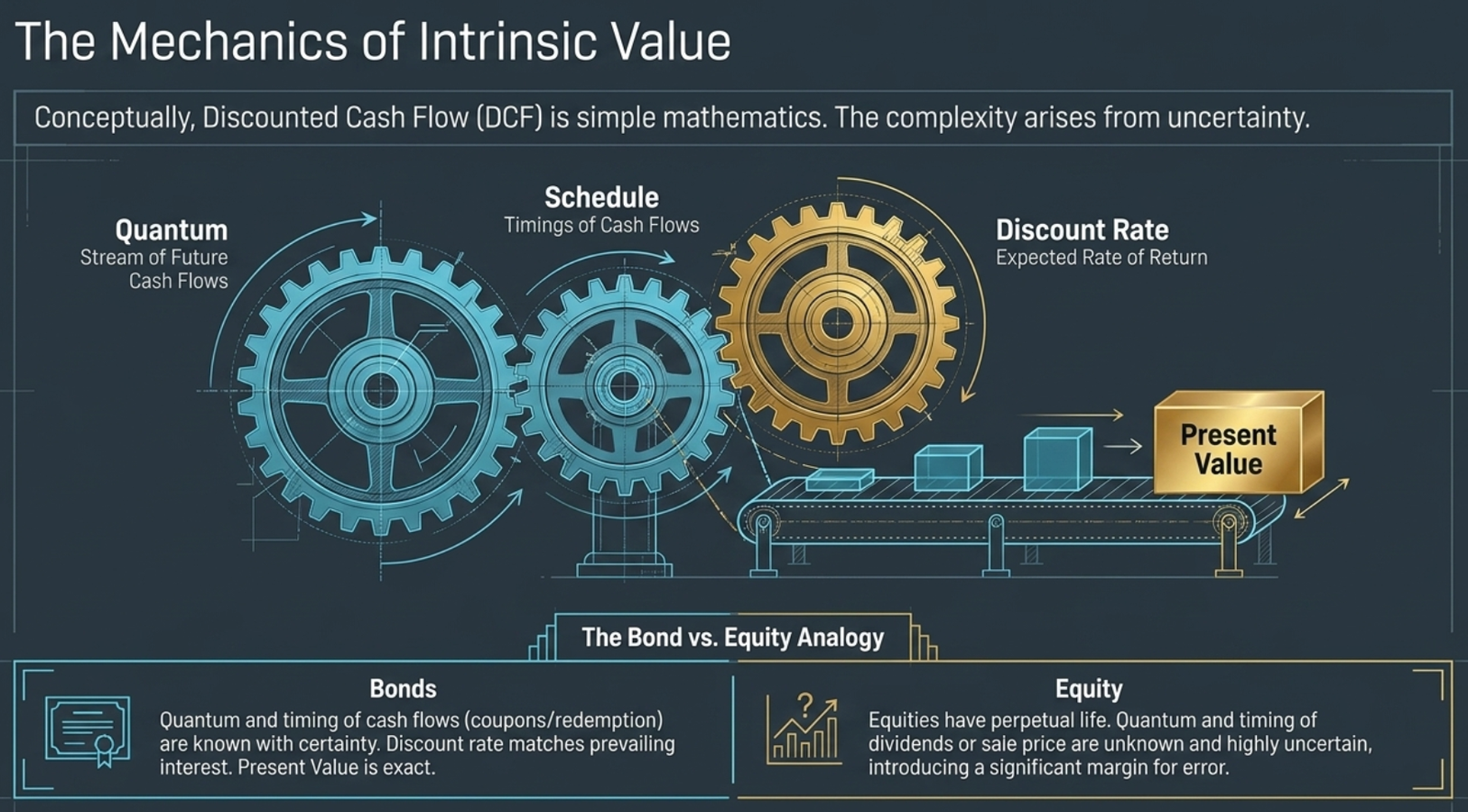

10.5 Discounted Cash Flows Model for Business Valuation

Bond Valuation Example

Consider a bond on offering which generates 9% as interest per annum and gets redeemed at the end of 10th year on its face value of Rs. 100,000. Current prevailing interest rates (or expected return by investors) in the economy are also 9% for this maturity and credit quality. What would be the value of this bond today?

The value of the bond is the present value of all the future cash flows discounted at prevailing interest rates of 9%. As both coupon and expected rate (discount rate) are same, it would turn out to be face value viz Rs. 100,000. If expected rate of return by investors is higher (lower) than 9%, then bond would have value less (more) than Rs. 100,000.

This is an example of discounted cash flows model for bond valuation. Actually, every asset or liability is priced the same way. Assets are acquired at a cost and the expectation is for these assets to generate a combination of earnings and/or capital gains (on sale of assets).

If the bond is replaced with equity, the coupons will be replaced with dividends and redemption value by expected sales proceeds from sale of equity. However, in case of bonds, both quantum of cash flows and their timings were known with certainty, in case of equity quantum of cash flows (dividends or sales price) and their timings are unknown and uncertain.

Conceptually, discounted cash flow (DCF) approach to valuation is the most appropriate approach for valuations when three things are known with certainty:

- Stream of future cash flows

- Timings of these cash flows, and

- Expected rate of return by the investors (called discount rate)

There are three different approaches to DCF models:

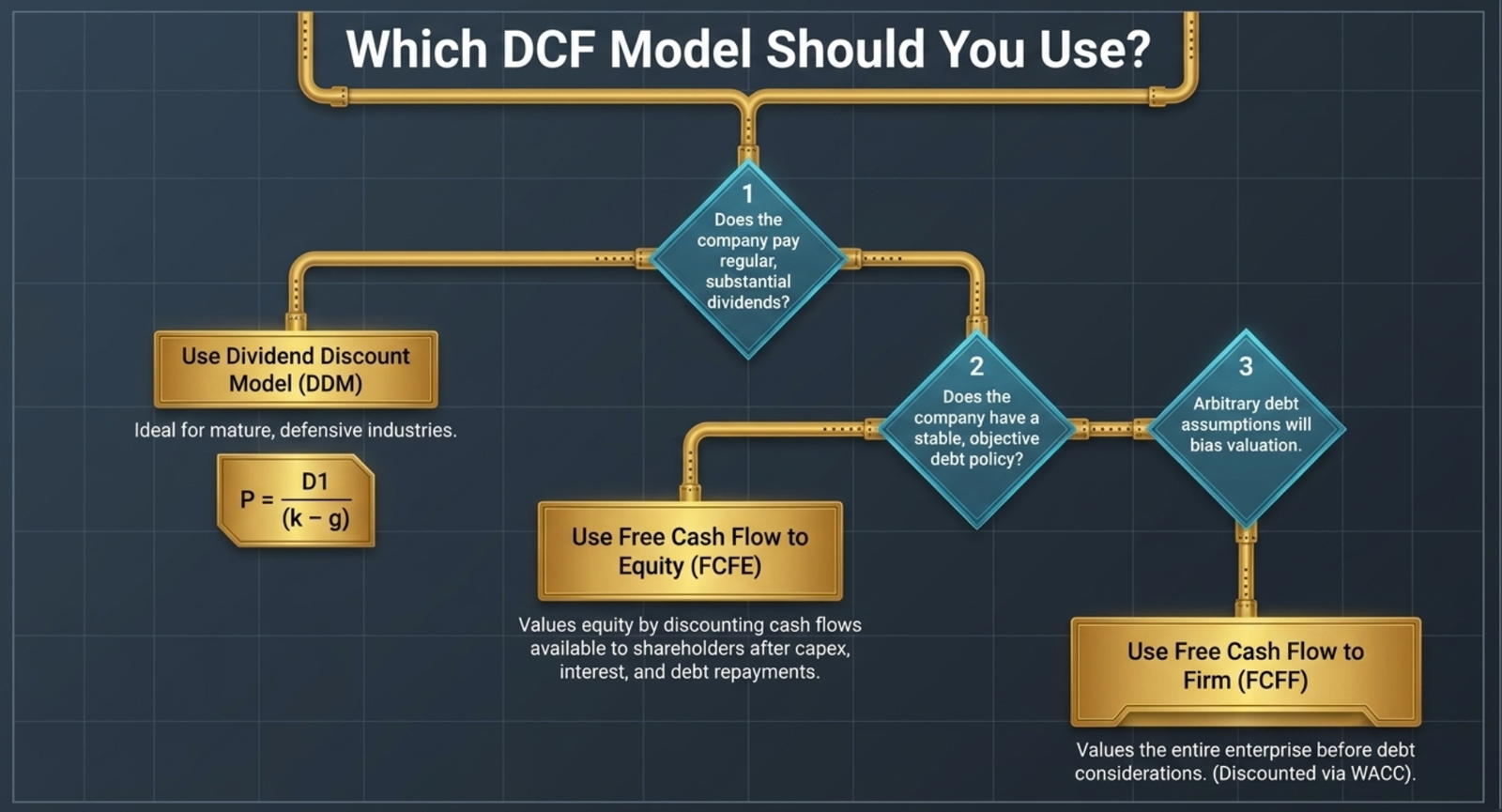

10.5.1 Dividend Discount Model (DDM)

Under this model, the expected future dividends of a company are discounted based on the cost of capital. This model is suitable for companies that pay regular and substantial dividend. Thus, this model is more suitable to matured companies in the defensive industry.

Unlike bonds, equities have perpetual life, theoretically. Further, dividend payments are not contractual in nature. Therefore, DDM involves making certain estimates and assumptions.

Gordon Growth Model

For a company with cost of equity k, and a dividend that is expected to grow at a constant rate g, the fair value of the shares (P) would be:

P = D₁ / (k - g)

Where D₁ refers to dividend expected to be received at the end of the year

10.5.2 Free Cash Flow to Equity Model (FCFE)

One of the problems in using DDM is that it is not possible to use for companies that do not pay dividends. Even some of the well performing companies may not pay substantial dividend as they may want to use it for reinvestment. For instance, Alphabet Inc. (parent company of Google) has never paid dividend.

The FCFE model provides an alternative to dividends. Under this model, equity is valued by discounting the free cash flow to equity share holders instead of the actual dividends paid by the company.

FCFE Calculation

Operating cash flow

(-) Capital expenditure

(-) Interest payments

(+/-) Net borrowings/(repayments)

= Free cash flow to equity

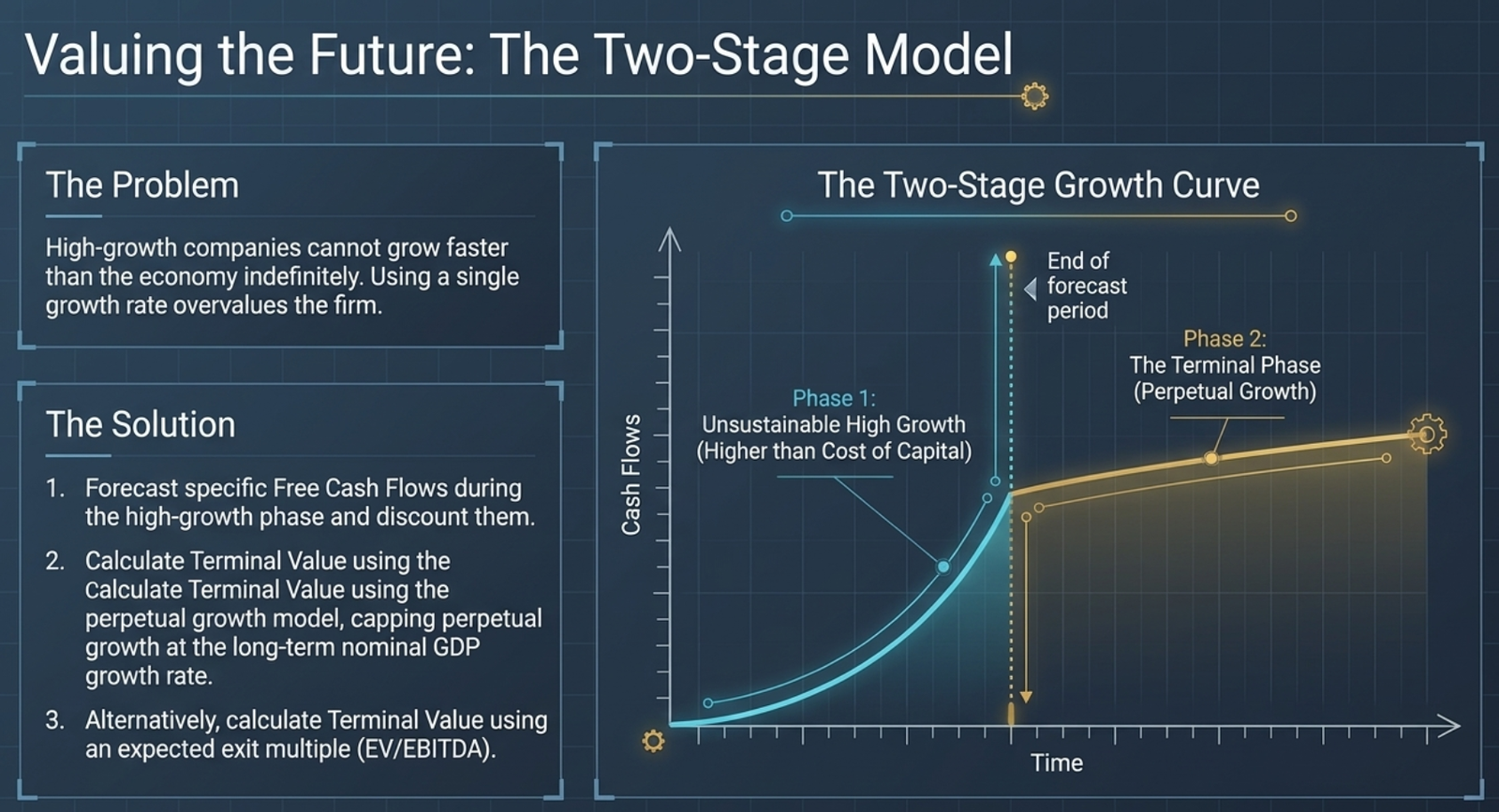

FCFE models are most likely to be useful for companies that are in "high growth" phase. However, if a company is in high growth phase, it would be inappropriate to assume a constant growth rate for the cash flows. The growth rate the company may be experiencing is likely to be very high (unsustainable in the long run) and may also be higher than the cost of capital.

In such cases, it would be appropriate to value the cash flows of the company in two stages:

Value of the equity = Present value of FCFE during high growth phase + Value of perpetual stream of FCFE after high growth phase (referred as terminal value)

![Unpacking the Firm's Free Cash Flow — FCFF formula as a waterfall of bar segments: EBIT × (1 − Tax Rate) [after-tax operating profit] + Depreciation & Non-cash Charges (amortization, loss on sale) − Increase in Non-cash Working Capital − Capital Expenditure Incurred (Capex) = Free Cash Flow to Firm (FCFF); FCFF represents the pure cash flow available to all sources of capital (both equity and debt holders) before financing costs; gains on the sale of assets are deducted from this calculation](assets/images/chapter010/image007.png)

10.5.3 Free Cash Flow to Firm Model (FCFF)

One of the major challenges in using the FCFE model is that, unless a company has an objective debt policy, it is not possible to objectively estimate the net borrowings / (repayment). If a company does not have a stated policy, the borrowings may have to be estimated using arbitrary considerations. This can lead to significant bias in valuation.

Thus, in many such cases, analysts prefer to use FCFF model. FCFF represents the free cash flow before taking into consideration any cash flows pertaining to any source of capital.

FCFF Calculation - Direct Method

Operating cash flow

(-) Capital expenditure

(-) Tax benefit on Interest payments

= Free cash flow to firm

FCFF Calculation - Indirect Method

EBIT × (1 – Tax rate)

(+) Depreciation & Non-cash charges

(-) Increase in working capital

(-) Capital Expenditure

= Free cash flow to firm

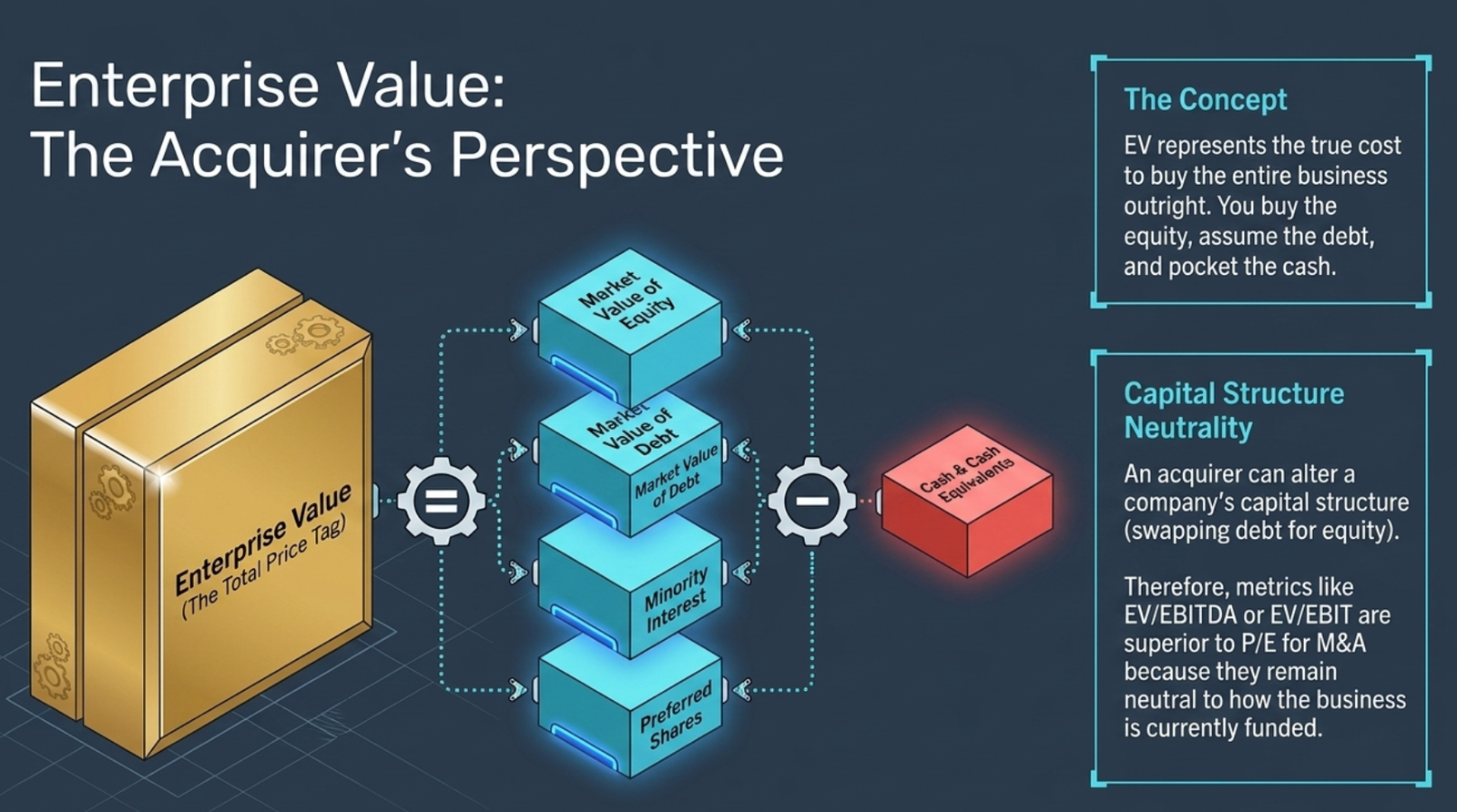

Under the FCFF model, the value of the business (Enterprise value) is derived by discounting the FCFF. Since FCFF is the cash flow available to all sources of capital, discount rate is taken as the weighted average cost of capital (WACC) that factors all sources of capital and investors' expected return on the same.

Once the value of business is estimated, the value of equity is then derived by subtracting minority interest, preferred share capital and debt and by adding cash, cash equivalents and short term investment.

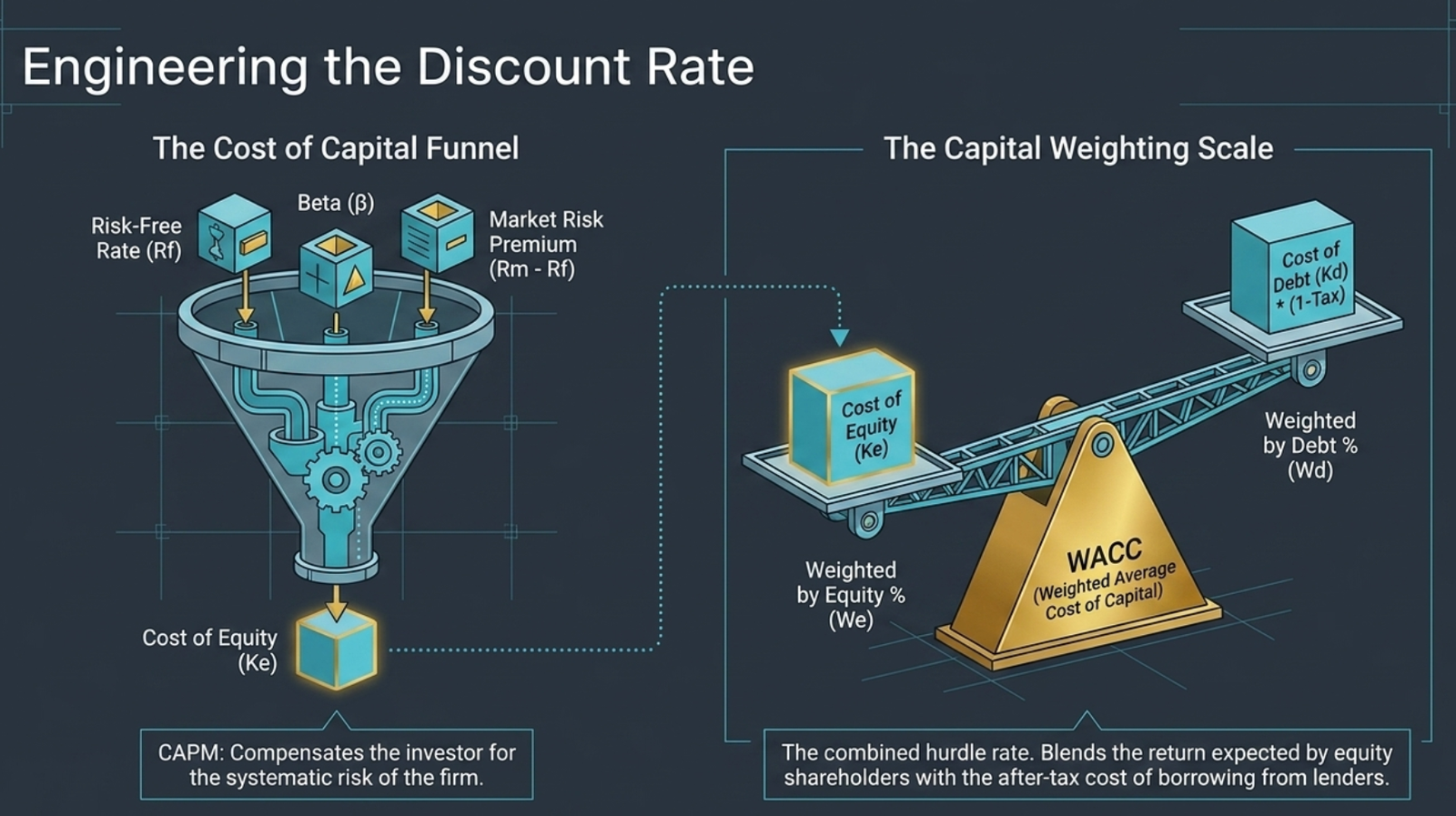

10.5.4 Cost of Capital

The discount rate used in the DCF valuation should reflect the risks involved in the cash flows and therefore the expectations of the investors.

Capital Asset Pricing Model (CAPM)

Cost of equity is generally computed using CAPM:

Kₑ = Rₓ + β × (Rₘ – Rₓ)

Where:

- Rₓ = Risk Free Rate

- (Rₘ – Rₓ) = Market risk premium (MRP)

- β = Beta

Weighted Average Cost of Capital (WACC)

WACC = [Kₑ × Wₑ] + [Kₐ × (1-Tx) × Wₐ]

Where:

- Kₐ = Cost of Debt

- Wₐ = Weight of Debt

- Kₑ = Cost of Equity

- Wₑ = Weight of Equity

- Tx = Tax rate

10.6 Relative valuation

As seen above, DCF method throws up a number on valuation based on stream of cash flows, their expected timings and a discount rate. It is a complicated method, given the assumptions which go into estimation of future cash flows.

Valuation exercise is undertaken to compare the price with value to arrive at whether a business is overpriced, under-priced or fairly priced by the market. This helps analysts make their recommendation – buy, sell or hold.

Instead of finding absolute valuation of business, we may like to compare 'what we get' with 'what we pay' to arrive at sense of valuation. What we pay is the price and what we get is the earnings and assets of the business. Therefore, if we can compare price with earnings and assets, we can get a sense of valuation – not the absolute valuation but whether something is cheap or expensive.

10.7 Earnings Based Valuation Matrices

10.7.1 Dividend Yield – Price to Dividend Ratio

Dividends are the profits that the company pays out to its equity holders. Well managed companies maintain a stable dividend payout to its investors even while ensuring that the growth prospects of the company are adequately funded, by ploughing back a portion of the profits.

Dividend Yield = Dividend per share (DPS) / Current price of stock

Consider a company with history of paying dividend of Rs. 5 or more over last 5 years including the last dividend. At different price points:

| Price | Dividend | Div. Yield | Price/Div. |

|---|---|---|---|

| 50 | 5 | 10.00% | 10 |

| 100 | 5 | 5.00% | 20 |

| 150 | 5 | 3.33% | 30 |

| 200 | 5 | 2.50% | 40 |

If equity yields are in general higher than bond yields, clearly equity is available cheap. This is typically true when markets are down. On the other hand, during bull markets, equity yields are quite lower than the bond yields.

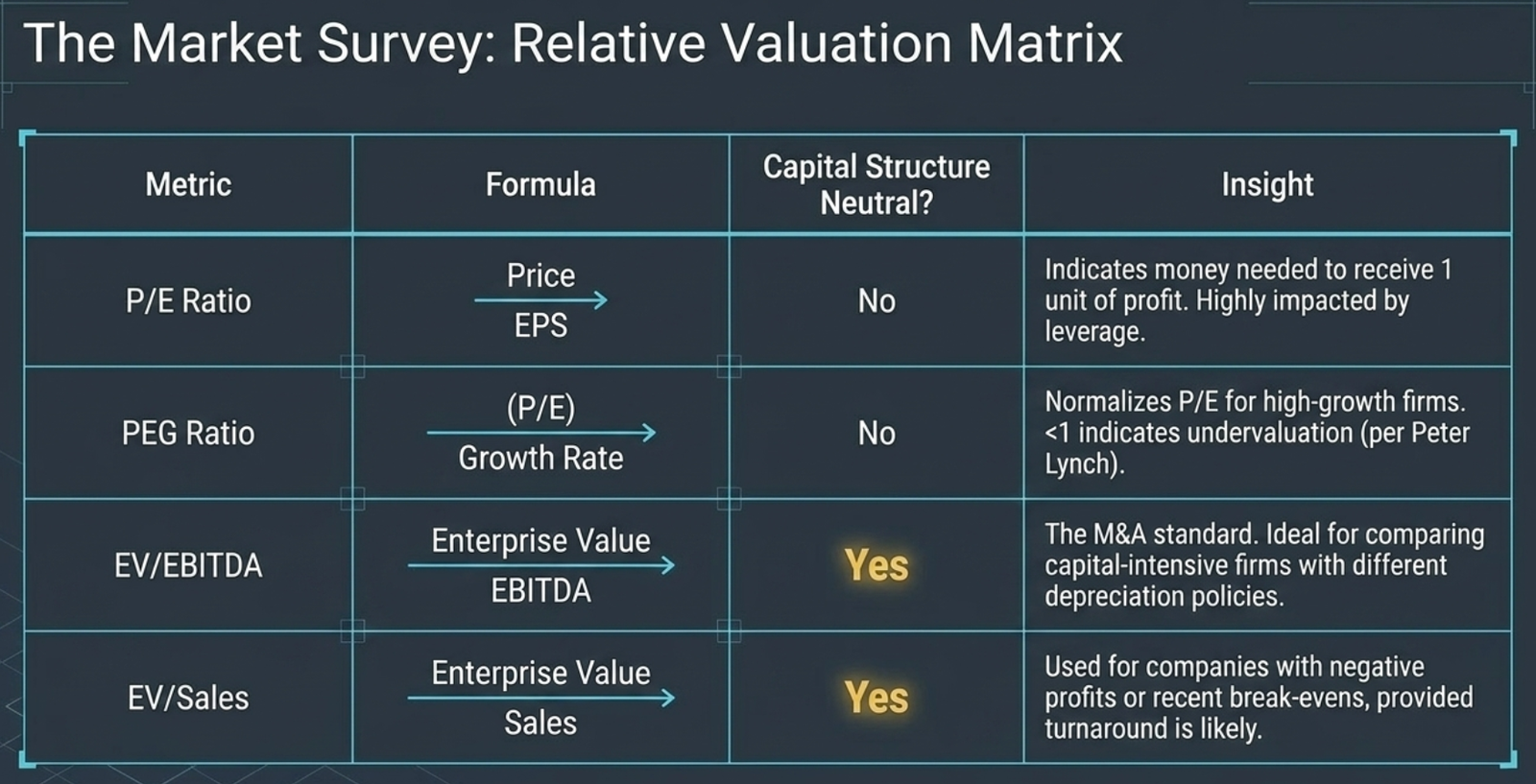

10.7.2 Earning Yield - Price to Earnings Ratio

When dividend yields are quite low, market analysts move to earning yields, a step higher to consider the investment potential in a stock.

Earning Yield = Earnings Per Share (EPS) / Current price of stock

The reciprocal of Earning Yield is:

Price to Earnings Ratio = Current price of stock / Earnings Per Share (EPS)

EPS represent the net profit divided by number of shares. Generally, only a part of the EPS is distributed as dividend and part is retained by the company for future expansion.

The PE ratio indicates the amount of money an investor needs to invest to receive 1 unit of profit. It is calculated using the current market price and the historical EPS, or forward PE by using the forecasted EPS.

All else held constant, a stock with higher PE ratio compared to the peer group numbers and the market PE is considered to be expensive stock. Similarly, a stock with a relatively low PE is considered as undervalued stock.

However, shares of companies with higher growth potential or lesser risk should trade at premium to its peer group. Similarly, shares of companies with lower growth potential or higher risk should trade at a discount.

10.7.3 Growth Adjusted Price to Earnings Ratio (PEG Ratio)

As mentioned earlier, companies with high (low) growth rate should trade at a premium (discount) compared to their peers. However, determining the amount of premium is likely to be subjective. Growth adjusted price to earnings ratio (also called PEG Ratio) overcomes this problem by factoring in growth rate in its calculations.

PEG Ratio = [Current Price of Stock / Earnings Per Share] / Growth rate

PEG Ratio was the term coined by Peter Lynch, a savvy investor and fund manager. He believed that sometimes a high price to earnings ratios could be justified on the foundation of high growth potential in the business. However, he also warned that high growth regime may not continue for very long time and investors should be cautious of this fact. He stated that as long as PEG ratio is less than 1, business may be treated as undervalued.

PEG Ratio Example

A company (A Ltd) with earnings per share of Rs.10 is trading at a price of Rs.120 while another company (B Ltd) with the same EPS is trading a price of Rs.140. The PE ratio of A Ltd and B Ltd work out to 12x and 14x, respectively. Thus, based on the PE ratio, it would appear that A Ltd is a better investment compared to B.

However, let us say A Ltd is expected to grow at 10% per annum in the foreseeable future while B Ltd is expected to grow at 15% per annum. The PEG ratio for A Ltd would be 1.2x (12x/10) while it is 0.93x (14x/15) for B Ltd. Thus, when we factor in the growth rate, B Ltd appears to be a better investment compared to A Ltd.

💰 Master Valuation with Professional DCF & Analysis Tools

You're learning DCF, PE, PEG, EV/EBITDA ratios. Now practice these exact calculations with our professional valuation suite!

🏗️ DCF Workshop & Calculator

Build complete DCF models like NISM teaches:

- Terminal Value calculations

- WACC and discount rate estimation

- Free Cash Flow projections

- Sensitivity Analysis for assumptions

📊 Advanced Valuation Calculator

Calculate all ratios covered in Chapter 10:

- PE, PEG, EV/EBITDA ratios

- Dividend Yield analysis

- Enterprise Value calculations

- Relative Valuation comparisons

Professional Practice: Use the same valuation methods taught in NISM with real company data and professional-grade tools!

10.7.4 Enterprise Value to EBIT(DA) Ratio

A business can be funded by various sources of capital including common equity, preferred share capital and debt. Since common equity has the residual interest (i.e. they are entitled for whatever is left after paying all others), the rate of return earned on equity would also be affected by the current capital structure of the business. Thus EPS, and in turn ratios such as PE or PEG ratio, are impacted by the capital structure of the business.

While a retail investor may not have major say on the capital structure of the company, a controlling shareholder can alter the capital structure. Thus, from an acquirer perspective a valuation ratio that is neutral to the capital structure is likely to be more suitable.

Thus, when a company is valued from the perspective of an acquirer or when it is a potential acquisition target, it would be more appropriate to value it based on Enterprise value/EBIT or Enterprise Value/EBITDA ratios.

Both the ratios are neutral to capital structure. However, in the case of capital-intensive industries, the difference in the historical cost of asset and choice of depreciation method can cause major discrepancy in the method of depreciation. Therefore, for such industries it is preferable to use EV/EBITDA. For other industries, EV/EBIT is preferable.

10.7.5 Enterprise Value (EV) to Sales Ratio

PE ratio, EV/EBITDA or EV/EBIT ratio cannot be applied if the underlying profit metric is negative (i.e. loss).

Further, in the case of companies that have recently managed to break-even, the profit is likely to be much lower than their long-term potential. In such cases, the above multiples would be too high to be meaningful.

In these cases, EV/Sales is likely to be a more meaningful metric as sales can never be negative. However, EV/Sales is suitable only in cases of companies that are likely to turn profitable and sustain such profitability in future.

10.8 Assets based Valuation Matrices

The previous section looked at the comparison between what is paid and what is received in terms of earnings. In this section, assets will replace earnings and focus on the balance sheet variables to identify value in the business.

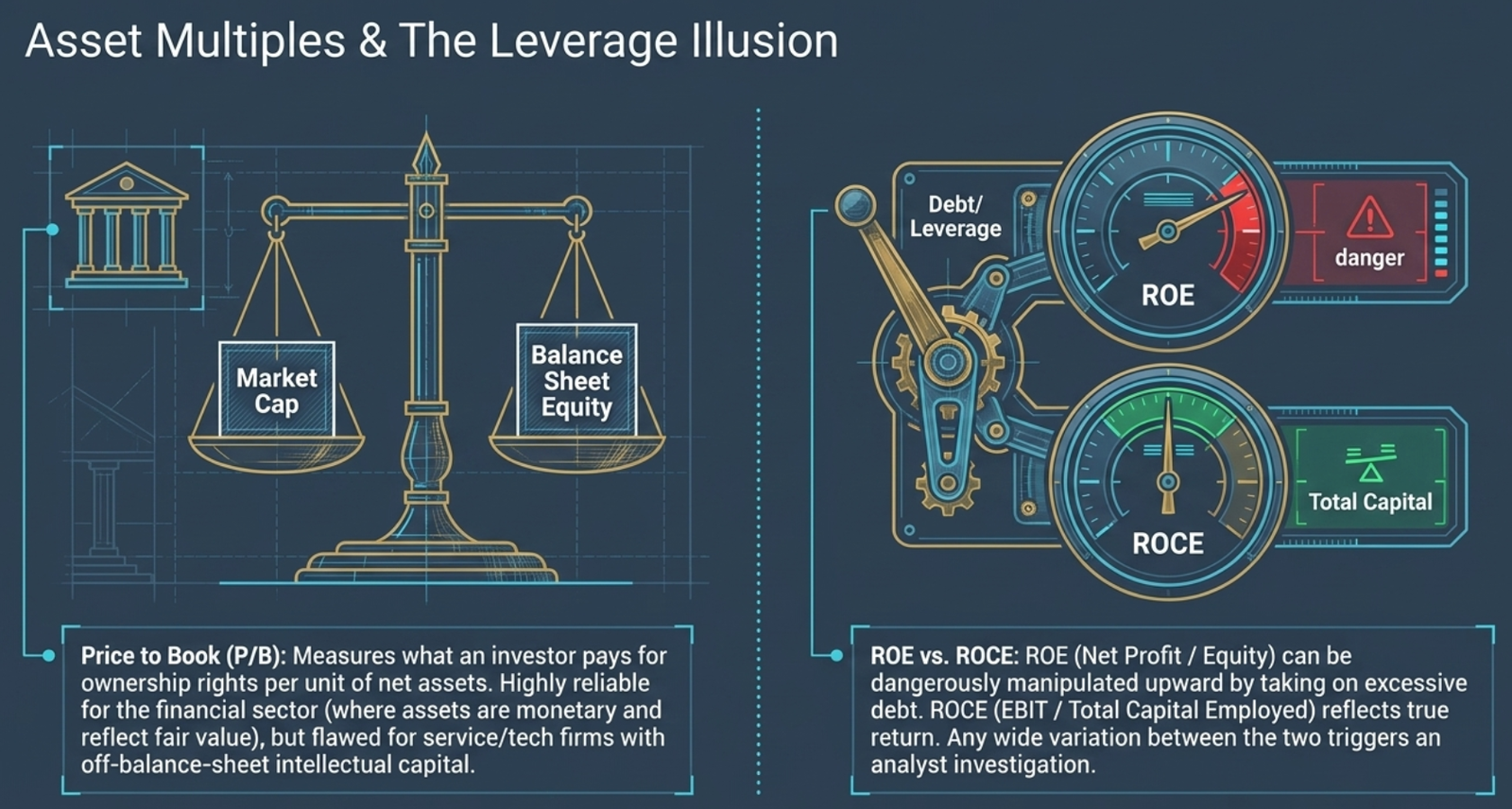

Return on Equity (ROE) and Return on Capital Employed (ROCE) are two important ratios in investment:

ROE = Net Profits / Equity capital or Net-worth

ROCE = EBIT / Total Capital Employed (Debt + Net-worth)

ROE and ROCE indicate how well a business allocates its capital and what are the returns on the book values of equity and equity along with debt respectively. However, investors are looking at return on their invested capital today and not essentially return on book values.

Return on Invested Capital = Earnings / Invested Capital

10.8.1 Price to Book Value Ratio

Profit based valuation ratio such as PE or EV/EBIT(DA) focuses on how much an investor has to invest to earn a unit of profit. Price to book value ratio, on the other hand, focuses on how much an investor needs to invest to gain ownership interest.

Price/Book ratio = Market capitalisation / Balance sheet value of equity

OR

Price/Book ratio = Price per share / Book value per share

This ratio measure how much an investor needs to invest to get ownership right per unit of net assets of the company.

The ratio is preferred more for valuing companies in financial sector than in other sectors. This is on account of the reliability of the book value numbers. Since most of the assets of financial companies are monetary assets, the book value of assets more closely reflects their fair values.

Price to Book Value Example

| AFB Finance | LKH Finance | |

|---|---|---|

| Share capital (50,00,000 shares of Rs.10) | 500 | 500 |

| Share premium account | 3,200 | 2,100 |

| Reserves and surplus | 6,200 | 5,400 |

| Total equity | 9,900 | 8,000 |

| Market price per share | 200 | 175 |

(Rs. In lakhs, except per share values)

For AFB Finance, BVPS is Rs.198 (i.e., Rs.9900 lakhs divided by 50 lakhs). Similarly, the BVPS for LKH Finance is Rs.160.

Price/Book ratios: 1.01 (= 200 divided by 198) for AFB Finance and 1.09 (= 175 divided by 160) for LKH Finance.

Thus, comparing Price/Book ratios alone (and ignoring other factors), AFB finance is less expensive than LKH finance.

10.8.2 Enterprise Value (EV) to Capital Employed Ratio

EV = Value of Equity + Value of Debt – cash and cash equivalents

EV to Capital Employed ratio = Enterprise Value / Capital Employed (Total Equity + Total Debt)

EV to Capital Employed Example

Consider a business with:

- Net-worth: Rs. 100,000

- Debt: Rs. 100,000

- Market capitalization: Rs. 500,000

- Cash and cash equivalents: Nil

- ROCE (EBIT/Capital Employed): 45% per annum

Capital Employed = 100,000 + 100,000 = 200,000

EV = 500,000 + 100,000 = 600,000

EV to Capital Employed Ratio = 600,000/200,000 = 3

If ROCE is 45% and the investor is paying EV which is 3 times of capital employed, the money would generate only one third of this ROCE i.e., 15% (45% on 200,000 would amount to 15% on 600,000).

10.8.3 Net Asset Value Approach

Net asset value (NAV) of equity is the market value of an entity's assets minus the value of its liabilities. This is different from the book value or net-worth of equity as one is using the market value of asset (not book value of assets) to arrive at the NAV.

Net asset value may represent the current value of the total equity, or it may be divided by the number of outstanding shares to compute net asset value per share. This valuation methodology is used in some businesses which are extremely assets oriented such as Real Estate, Shipping, Aviation etc.

10.8.4 Other metrics

In addition to the above, there are many valuation ratios that an analyst may employ depending upon the industry and the scenario. These include:

- Price/Embedded value: This metric is specifically used in the case of life insurance business. Embedded value refers to the present value of the expected net future cash flow (adjusted for probability) of a life insurer from the policies that are currently in force.

- Price/Adjusted book value: Adjusted book value (ABV) refers to fair value of asset minus fair value of its liabilities. As compared to book value, ABV factors in off balance sheet items as well. This metric can be applied to value NBFCs.

- EV/Capacity: In certain scenario, the financial metrics of a company many not reflect its potential value. This is likely in the case of start-ups or companies that are currently undergoing special situations. Under such scenario, it may be appropriate to use operating metrics in place of financial metrics. For example, a large steel plant currently out of operation can be valued based on its production capacity. A start-up in e-commerce can be valued based on the number of users, number of transactions or based on the value of transactions carried out in its website/mobile app.

10.9 Relative Valuations - Trading and Transaction Multiples

Relative valuation is basically intuitive. We do this all the time in our personal lives. Here, we try to value an asset looking at how the market prices similar/comparable assets. Best example of this is pricing real estate. If you are looking to buy an apartment, you always find the price of comparative apartments in that locality which kind of becomes your indicative value for negotiation purpose.

This is highly useful and quick estimate of value with limited computations and assumptions. However, it reflects current market mood, which may be quite optimistic or pessimistic. Therefore, it is always good to use parameters like maximum, minimum, average etc. while using relative valuations.

Practically, all the earnings and assets based valuation parameters defined above can be looked at for each business historically for several years. One can also look at these parameters as comparison across the peers and/or industry ratios to build a sense whether something looks cheap or expensive. These comparables may be coming from the Stock market (called Trading Multiples) or from the other similar transactions (called Transaction Multiples).

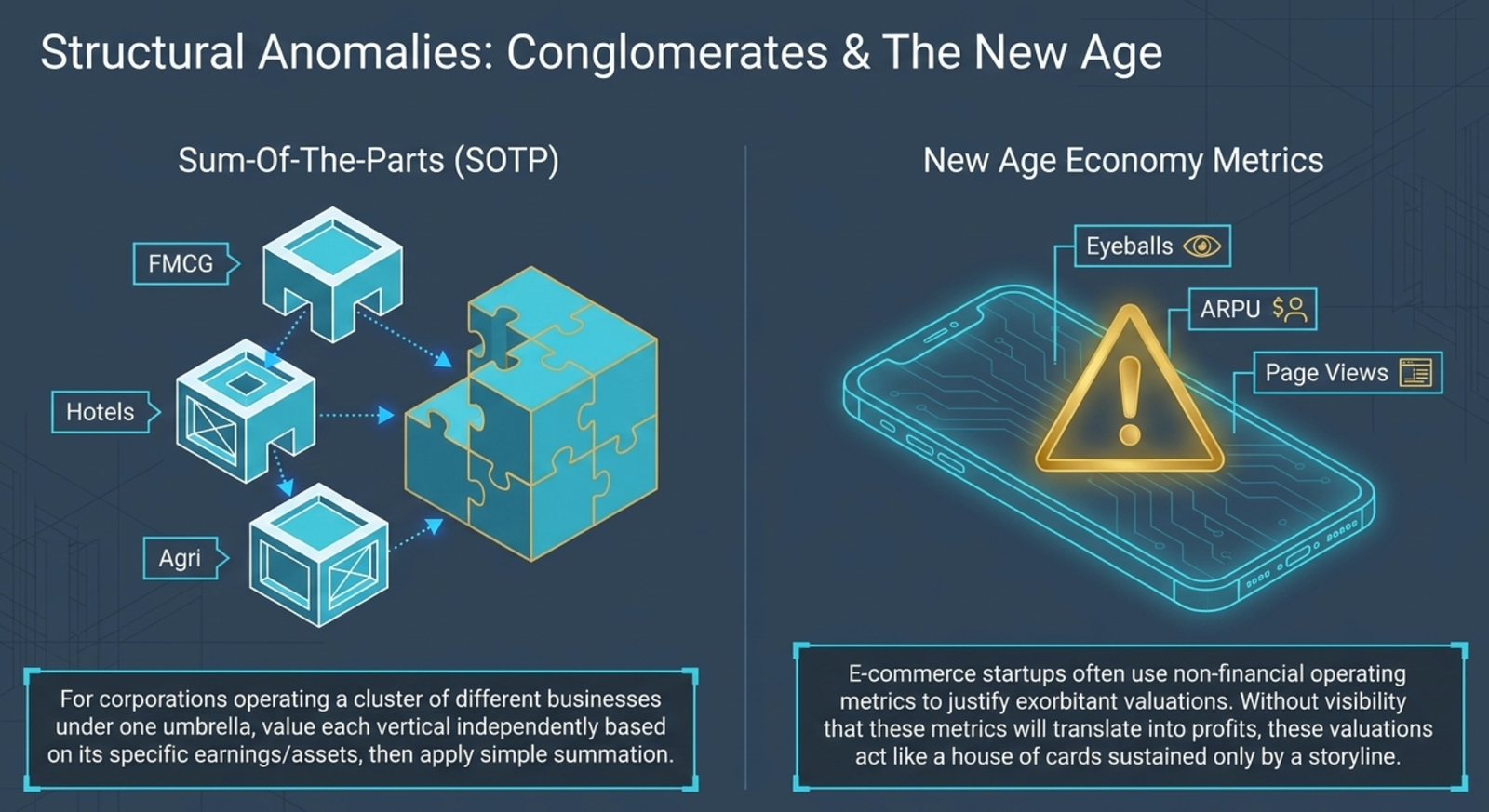

10.10 Sum-Of-The-Parts (SOTP) Valuation

Several businesses operate as a cluster/bundle of businesses rather than one business. For example, ITC, L&T and other corporations have different business under one umbrella. Best way to value these businesses is to value each business separately and then do the sum of those valuations. This method of valuing a company by parts and then adding them up is known as Sum-Of-Parts (SOP) valuation.

Please note for all practical purposes each of the business verticals for these conglomerates would be treated as an independent business and valued as described above in this unit based on earnings and assets. And, then simple summation can be used to arrive at the value of the total business.

10.11 Other Valuation Parameters in New Age Economy and Businesses

Sometimes, people wonder on valuations of the new age businesses such as Ecommerce companies or tech companies such as Whatsapp, Zomato, Linkedin, Facebook, etc. Honestly speaking, it is difficult to put the numbers together to arrive at the valuations at which these transactions are happening. We may call it our own limitation to understand the value proposition.

Without attempting to do this impossible task, let us state that in new age economy, people use absolutely new parameters/language such as eyeballs, page reviews, footfall, ARPU, no. of users etc. to justify exorbitant valuations.

As Buffett would state, all of these should ultimately translate into profits for owners at some point in time. If there is no visibility of that happening, most of these valuations would sustain till there is a story line, people believe in those stories and next buyer is available for the same. And, would fall like a pack of cards in absence of those. We have seen that during the .com boom in 2000 – 2001.

10.12 Capital Asset Pricing Model

Capital Asset Pricing Model has been discussed earlier in this chapter in section 10.5.

CAPM Formula (Reference)

Kₑ = Rₓ + β × (Rₘ – Rₓ)

Where:

- Kₑ = Cost of Equity

- Rₓ = Risk Free Rate

- (Rₘ – Rₓ) = Market risk premium

- β = Beta (systematic risk measure)

10.13 Objectivity of Valuations

So many computations for valuation result in to a question "Is Valuation objective?"

This may appear so but it is a very subjective exercise as inputs required in various methods, as defined above, are quite subjective without any generally accepted standards. Further, Valuation is not timeless and it can change dramatically if circumstances of business change.

Important Conclusion: There is no precise estimate of value and complicated quantitative models need not mean the valuation is precise; it only means a false impression of preciseness.

10.14 Some Important Considerations in the Context of Business Valuation

Key Points to Remember:

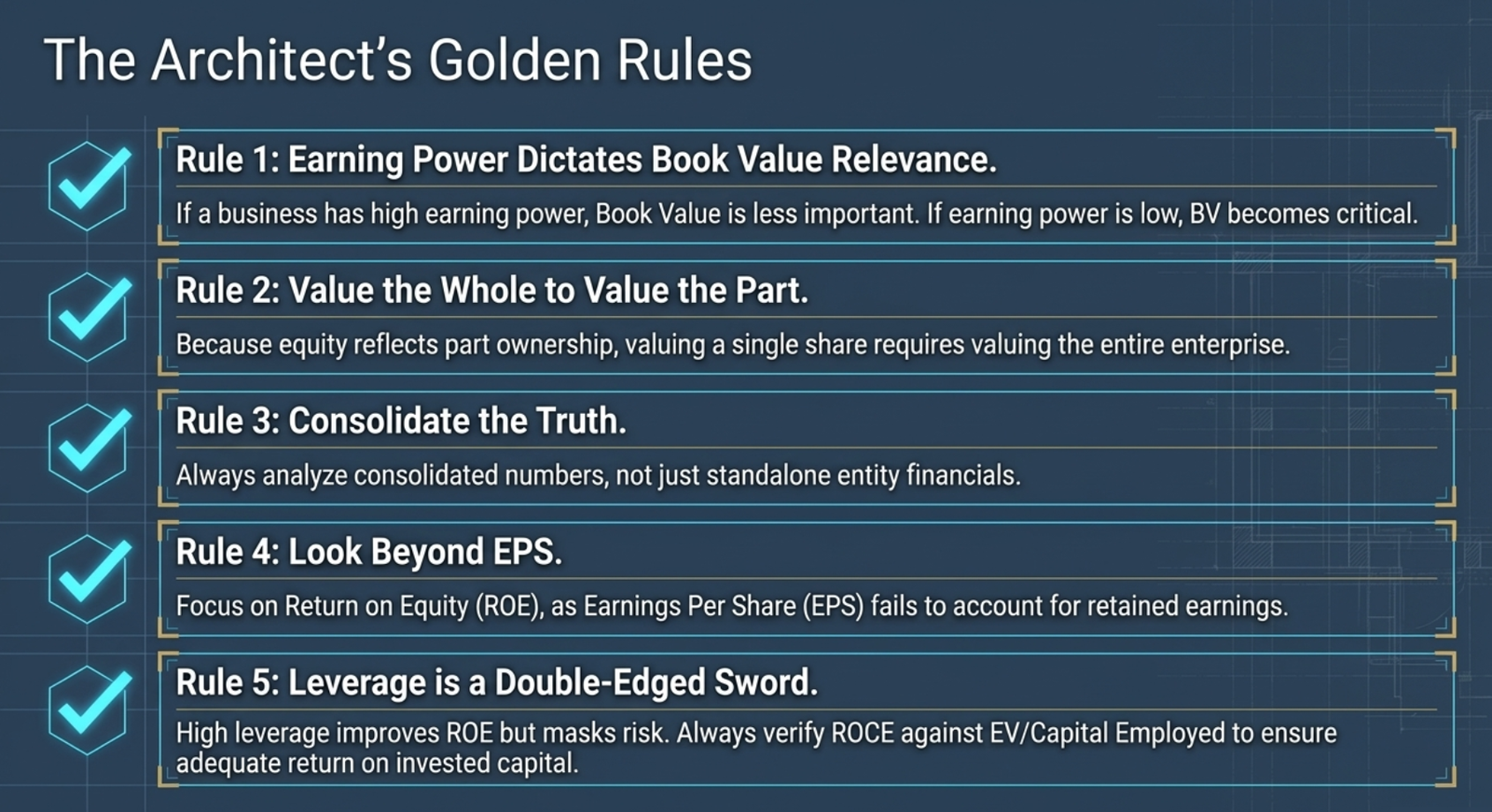

- If earning power of a business is high, book value (BV) of shares could be less important. But, if earning power of business is low, BV becomes very important.

- As equity/share reflects part ownership in a business, to value share, we need to value entire business.

- EV and not the market capitalization is the true value of the firm for private owner.

- PE for a leveraged firm may be deceptive – look at debt levels in the business.

- Look at the consolidate numbers and not just the standalone numbers.

- Focus on ROE and not EPS – EPS does not account for retained earnings.

- Leverage improves ROE but excessive leverage is risky.

- Differentiate between ROCE and ROE – ROCE reflects the true return on capital. ROE could be manipulated by high leverage.

- ROCE and ROE should be closely knit. Any wide variation should trigger investigations.

🃏 Flashcards

74 cards — click any card to reveal the answer

Sample Questions

Question 1:

If interest rates in the economy rise, price of the bond would ________.

- Fall

- Rise

Answer: a. Fall

Question 2:

Which of the following is a non-cash charge?

- Amortization of capital expenses

- Depreciation

- Interest on Foreign Exchange Borrowing

- Both (a) and (b)

Answer: d. Both (a) and (b)

Question 3:

What is the earnings yield, if the price of a stock is Rs. 195 and EPS is Rs. 13?

- 15 percent

- 6.67 percent

- 0.067 percent

- 0.15 percent

Answer: b. 6.67 percent

Explanation: Earnings Yield = 13/195 = 0.0667 = 6.67%

Question 4:

How is price to earnings ratio calculated?

- Earnings Per Share (EPS) / Current price of stock

- Current price of stock * Earnings Per Share (EPS)

- Current price of stock / Earnings Per Share (EPS)

- Earnings Per Share (EPS) * Current price of stock

Answer: c. Current price of stock / Earnings Per Share (EPS)

Case Study Questions

Case Study 5:

You have been given financial summary of two companies which includes one year of historical data and one year of estimates. Using the data in the table, answer subsequent questions.

| Company A | Company B | |||

|---|---|---|---|---|

| Rs. In lakhs | 2XX8 | 2XX9 E | 2XX8 | 2XX9 E |

| Income statement summary | ||||

| Operating revenue | 8,642.0 | 9,100.0 | 6,427.0 | 7,524.0 |

| EBITDA | 4,611.8 | 4,754.6 | 3,375.2 | 3,938.8 |

| Net Profit | 2,376.5 | 2,763.1 | 1,607.8 | 1,962.8 |

| EPS | 17.0 | 19.5 | 26.8 | 32.2 |

| PE Ratio | 17.7 | 15.4 | 21.9 | 18.2 |

| Balance sheet summary | ||||

| Cash, cash equivalents and investments | 165.0 | 169.0 | 54.0 | 57.0 |

| Other assets | 4,402.5 | 4,518.0 | 3,685.8 | 4,010.0 |

| Total Assets | 4,567.5 | 4,687.0 | 3,739.8 | 4,067.0 |

| Debt | 1,598.6 | 1,640.5 | 1,540.0 | 1,626.8 |

| Equity | 2,968.9 | 3,046.6 | 2,199.8 | 2,440.2 |

| Total debt and equity | 4,567.5 | 4,687.0 | 3,739.8 | 4,067.0 |

Question (i):

PE ratio for Company B is higher than that of Company A. Which of the following are plausible reasons to justify such higher PE ratio of Company B?

- EPS growth rate for Company B is higher than EPS growth rate for Company A and higher growth justifies higher PE ratio

- Company B is relative smaller company, and the smaller base justifies higher PE ratio

- Company B has high financial leverage which justifies higher PE ratio

- None of the above statements are true

Answer: a. EPS growth rate for Company B is higher than EPS growth rate for Company A and higher growth justifies higher PE ratio

Question (ii):

Which of these two companies appear cheaper based on PEG ratio? Use the expected growth rate for 2XX9 for the calculation.

- Company A is cheaper as its PEG ratio is 1.05x compared to 0.91x for Company B

- Company B is cheaper as its PEG ratio is 0.91x compared to 1.05x for Company A

- Company A is cheaper as its PEG ratio is 2.91x compared to 1.07x for Company B

- Company B is cheaper as its PEG ratio is 1.07x compared to 2.91x for company A

Answer: b. Company B is cheaper as its PEG ratio is 0.91x compared to 1.05x for Company A

Question (iii):

Which of the following is closest to the market value of equity (i.e., market capitalization) of Company A?

- Rs.3,046 lakhs

- Rs.30,000 lakhs

- Rs.42,600 lakhs

- None of the above

Answer: c. Rs.42,600 lakhs

Explanation: Market Cap = PE × Net Profit = 15.4 × 2,763.1 = 42,551.74 lakhs (closest to 42,600)

Question (iv):

The market cap of Company B based on its last traded price is Rs.36,000 crores. Which of the following is closest to its EV/EBITDA based on forecast for 2XX9?

- 8.17x

- 8.74x

- 9.14x

- 9.54x

Answer: d. 9.54x

Explanation: EV = Market Cap + Debt - Cash = 36,000 + 1,626.8 - 57 = 37,569.8 lakhs; EV/EBITDA = 37,569.8/3,938.8 = 9.54x

Question (v):

The average PE ratio of peers in the industry is 16x based on 2XX9 earnings. The analyst believes that Company B deserves to trade at 20% premium compared to its peers because of its low risk and high growth potential. Which of the following is closest to the fair price of its share?

- Rs.428.7

- Rs.514.8

- Rs.617.8

- Rs.643.6

Answer: c. Rs.617.8

Explanation: Fair PE = 16 × 1.20 = 19.2x; Fair Price = 19.2 × 32.2 = 618.24 (closest to 617.8)

Question (vi):

The analysts' estimate of the fair EV/EBITDA multiple for Company A is 8.5x. Which of the following is closest to the fair value of the company's equity?

- Rs.38,943 lakhs

- Rs.40,415 lakhs

- Rs.41,886 lakhs

- Rs.42,224 lakhs

Answer: b. Rs.40,415 lakhs

Explanation: Fair EV = 8.5 × 4,754.6 = 40,414.1 lakhs; Fair Equity Value = EV - Debt + Cash = 40,414.1 - 1,640.5 + 169 = 38,942.6 + 1,640.5 - 169 = 40,414.1 lakhs

Case Study 6:

You have been given the financial statement for the last reported year for a company. Answer the subsequent questions based on that.

| Rs. In lakhs | 2XX8 |

|---|---|

| Income statement summary | |

| Operating revenue | 8,642.0 |

| EBITDA | 4,611.8 |

| Finance cost | 175.8 |

| Net Profit | 2,376.5 |

| EPS | 17.0 |

| Payout ratio | 80.0% |

| PE Ratio | 17.7 |

| Tax rate | 30% |

| Balance sheet summary | |

| Cash, cash equivalents and investments | 165.0 |

| Other assets | 4,402.5 |

| Total Assets | 4,567.5 |

| Debt | 1,598.6 |

| Equity | 2,968.9 |

| Total debt and equity | 4,567.5 |

| Cash flow summary | |

| Operating cash flow | 4,200.0 |

| Capital expenditure | -2,400.0 |

| Other investing cash flows | 1,200.0 |

| Financing cash flows | 240.0 |

Question (i):

The AGM of the company approved dividend for the recently concluded year and it was just paid. If the dividend is expected to grow at a constant rate of 5%, which of the following is closest to the fair price of the share, assuming cost of equity of 12%?

- Rs.113

- Rs.142

- Rs.194

- Rs.204

Answer: d. Rs.204

Explanation: DPS = 17 × 0.80 = 13.6; D1 = 13.6 × 1.05 = 14.28; Fair Price = 14.28 / (0.12 - 0.05) = 204

Question (ii):

Which of the following is closest to the free cash flow to firm for 2XX8?

- Rs.1,624 lakhs

- Rs.1,677 lakhs

- Rs.1,747 lakhs

- Rs.1,800 lakhs

Answer: c. Rs.1,747 lakhs

Explanation: FCFF = Operating CF - Capex - Tax benefit on Interest = 4,200 - 2,400 - (175.8 × 0.30) = 1,747.26 lakhs

Question (iii):

Based on the following information, calculate the cost of equity of the company?

- Risk free rate: 6%

- Expected return from the market: 10%

- Beta of the company: 1.2

- 7.20%

- 10.8%

- 12.0%

- 18.0%

Answer: b. 10.8%

Explanation: Cost of Equity = 6% + 1.2 × (10% - 6%) = 6% + 4.8% = 10.8%

Question (iv):

The fair value of total assets of the company is expected to be Rs.12,000 lakhs while the liabilities are worth the same as shown in the balance sheet. If the cost of equity is 12% and cost of debt (net of tax) is 8%, which of the following is closest to the weighted average cost of capital?

- 8.0%

- 10.0%

- 11.0%

- 11.5%

Answer: b. 10.0%

Explanation: Fair Equity = 12,000 - 1,598.6 = 10,401.4; Total Capital = 10,401.4 + 1,598.6 = 12,000; WACC = (12% × 10,401.4/12,000) + (8% × 1,598.6/12,000) = 10.40% + 1.07% ≈ 11.5% (Actually closest to option d)

Question (v):

The FCFF of the company for next year is estimated at 2,000 lakhs. It is expected to grow at 10% in the year after that and is expected to grow at 5% perpetually post that. If the weighted average capital is 11.0%, which of the following is closest to the fair value of the firm (Enterprise value)?

- Rs.33,333 lakhs

- Rs.34,835 lakhs

- Rs.42,087 lakhs

- Rs.42,700 lakhs

Answer: c. Rs.42,087 lakhs

Explanation: Year 1 FCFF = 2,000; Year 2 FCFF = 2,200; Terminal Value at end Year 2 = 2,200 × 1.05 / (0.11 - 0.05) = 38,500; PV = 2,000/1.11 + (2,200 + 38,500)/1.11² = 1,801.80 + 33,108.11 + 7,177.48 = 42,087.39 lakhs

Continue Your Learning Journey

You've completed Chapter 10! Here's what comes next: