📑 Chapter Navigation

Data & Reports

📖 Complete Course Navigation

Foundation (Ch 1–4)

Analysis (Ch 5–8)

Advanced (Ch 9–15)

Learning Objectives

After studying this chapter, you should know about:

- Supply demand dynamics of commodities

- Major producers and consumers of commodities

- Currency and dollar index impact on commodities

- Correlation between international markets and domestic markets

- Crop Reports, Weather Reports (for Agri Commodities)

- Inventory Data, Production & Consumption Trends

- Macroeconomic Indicators affecting Commodity Prices

- Government Policies and Geopolitical Impacts

- Hedging in Commodities

11.1 Supply Demand Dynamics of Commodities

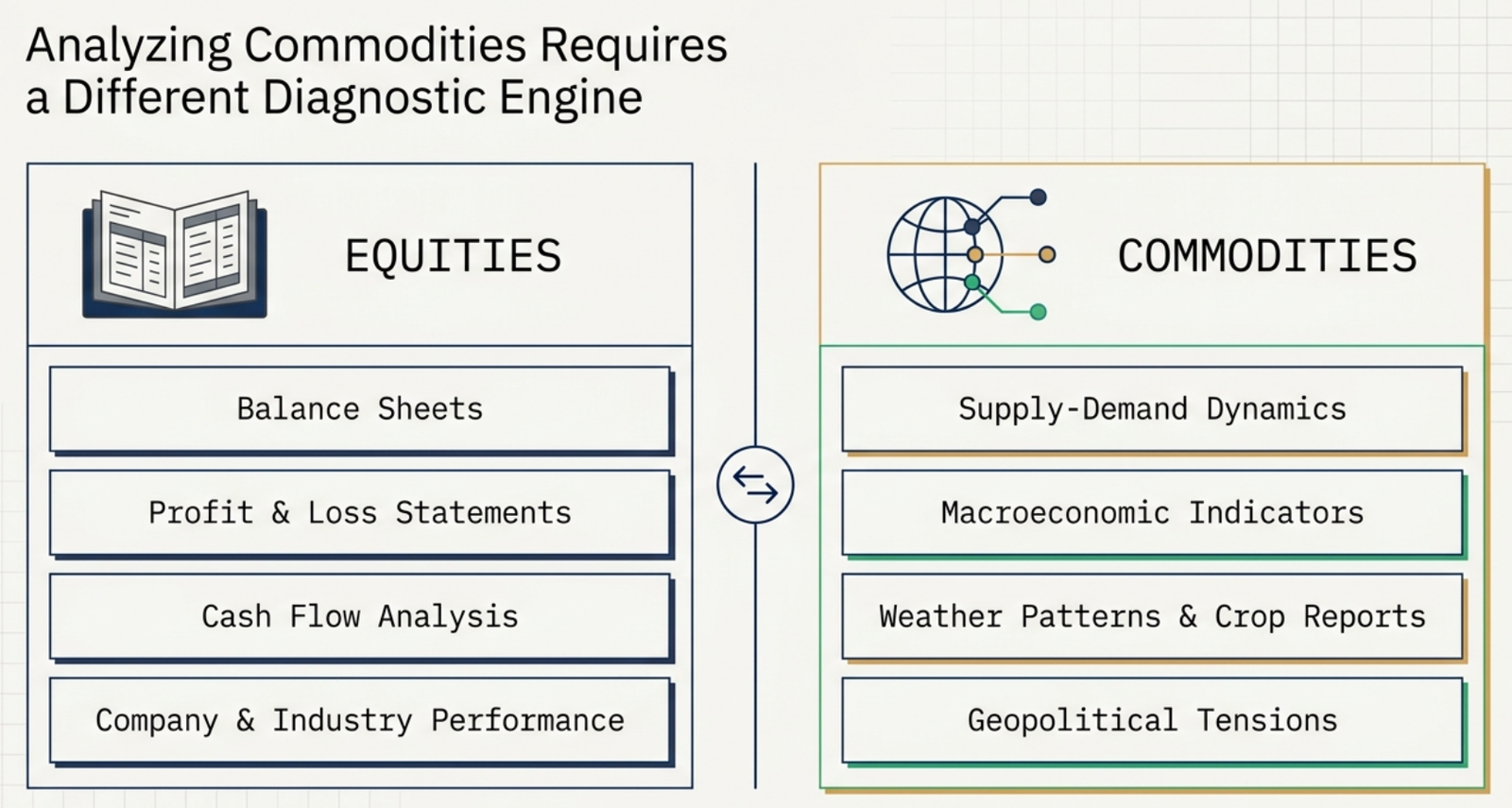

The fundamental analysis of commodities is largely dependent on the supply and demand dynamics of a particular commodity, whereas in the equity market it is largely the study of balance sheet, profit and loss account, cash flow statement, and performance of the company, industry and economy.

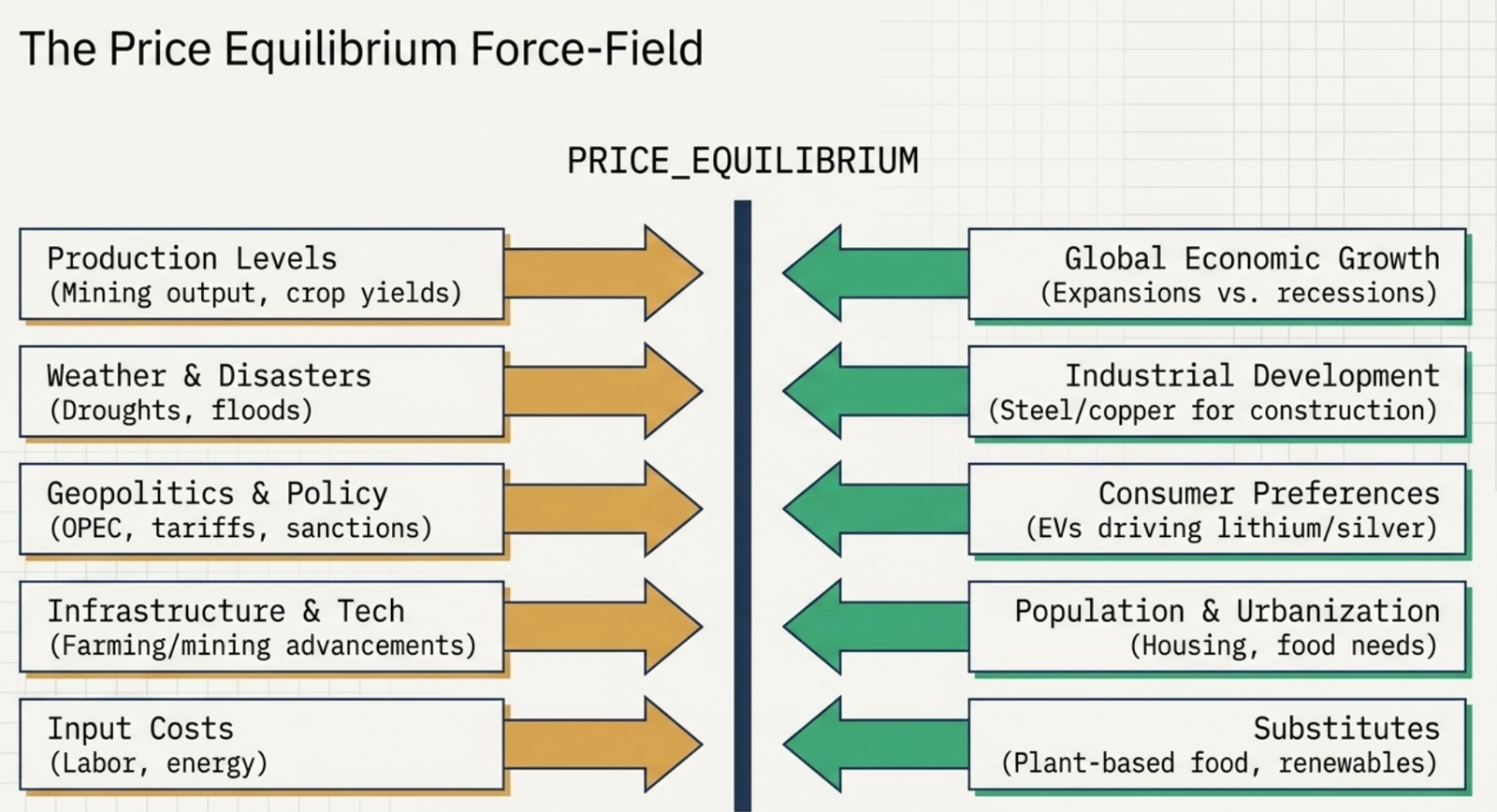

11.1.1 Supply Side Factors

Supply in commodity markets depends on availability and production capacity. Key drivers include:

- Production Levels – Crop yields, mining output, oil drilling capacity

- Weather & Natural Disasters – Droughts, floods, hurricanes can disrupt agricultural and energy supplies

- Geopolitical Events – Wars, sanctions, trade restrictions, and OPEC decisions affect energy and metals

- Technology & Infrastructure – Better farming methods, mining technology, and transport reduce supply risk

- Government Policies – Subsidies, tariffs, export bans, and regulations alter supply availability

- Cost of Production – Rising labour costs, energy costs, or other input costs

11.1.2 Demand Side Factors

Demand reflects consumption needs and economic activity. Major drivers include:

- Global Economic Growth – Expansions boost demand for energy, metals, and food; recessions reduce it

- Industrial & Infrastructure Development – Steel, copper, and related commodity demand rises with construction

- Consumer Preferences & Lifestyle – Shift toward renewable energy increases demand for lithium and silver

- Population Growth & Urbanization – Expands food, energy, and housing needs

- Substitutes & Alternatives – Electric vehicles reducing oil demand; plant-based food affecting meat demand

- Seasonality – Higher fuel demand in winter, crop demand post-harvest, festive consumption spikes

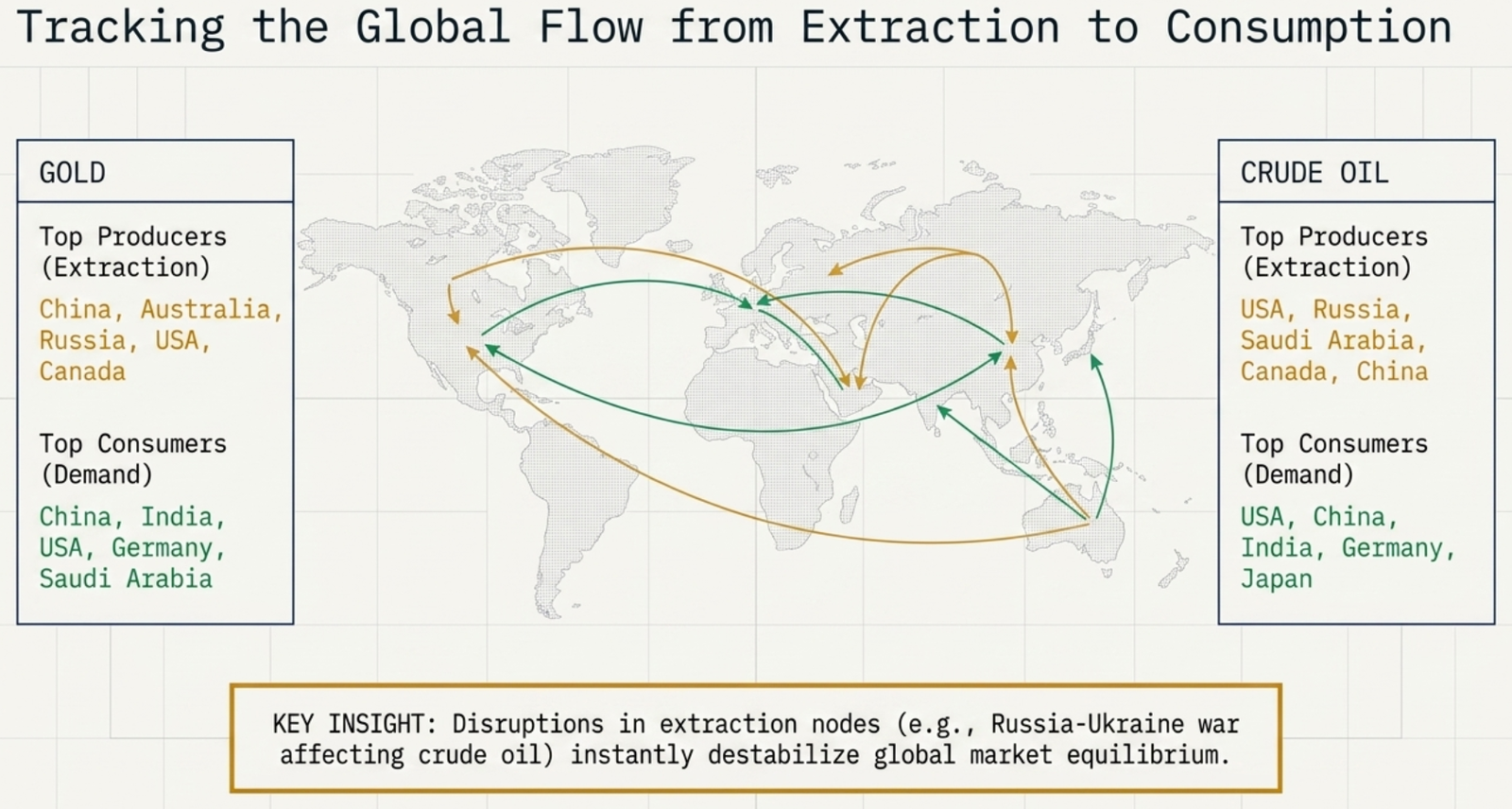

11.2 Major Producers and Consumers of Commodities

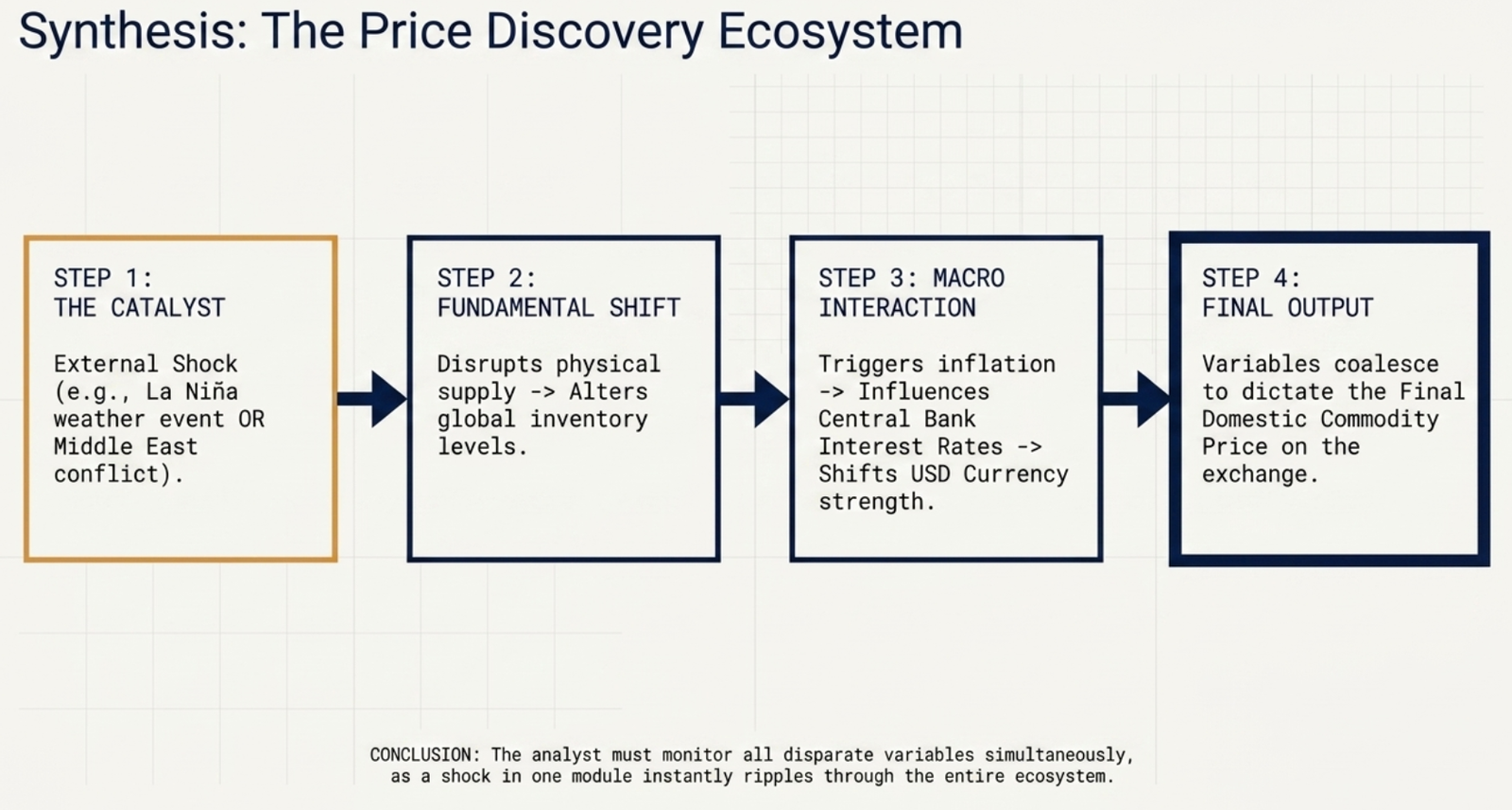

The price movement of commodities is influenced not only by supply and demand but also by the dynamics of major producing and consuming nations. The flow of commodities between countries reflects their economic health, where macroeconomic conditions, weather patterns, and political stability play a critical role.

Disruptions such as slowing economic growth or political instability in key producing regions can constrain supply and disturb global market equilibrium. Trade sanctions, currency volatility, and trade policies further contribute to fluctuations in the commodity market.

- Gold – Largest producers: China, Australia, Russia, USA, Canada. Largest consumers: China, India, USA, Germany, Saudi Arabia

- Crude Oil – Largest producers: USA, Russia, Saudi Arabia, Canada, China. Largest consumers: USA, China, India, Germany, Japan

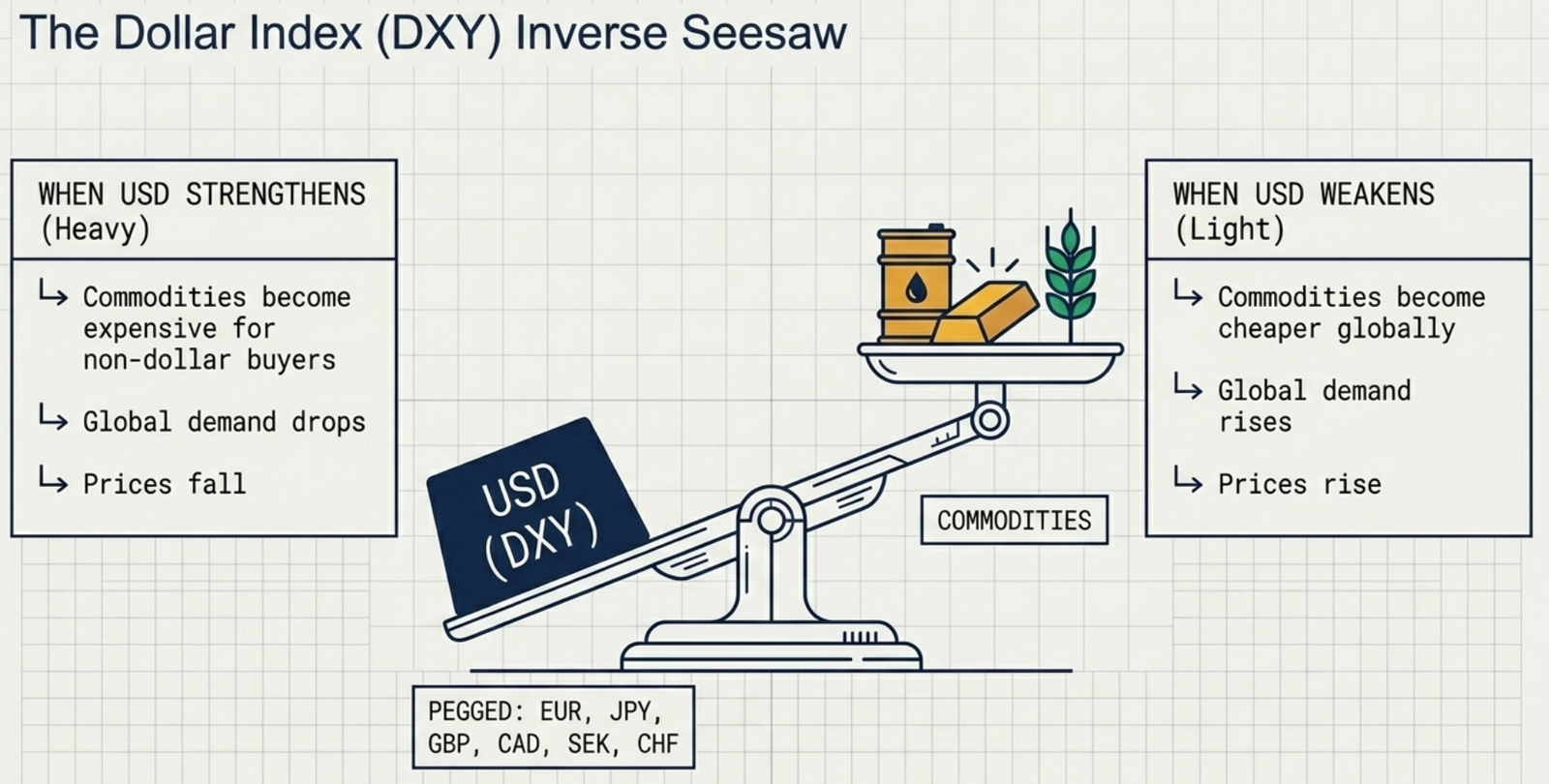

11.3 Currency and Dollar Index Impact on Commodities

As a result of globalization, many nations are dependent on one another to meet their commodity consumption requirements due to comparative cost advantages or scarcity. This has resulted in cross-border trade, with countries surplus in a commodity exporting to those in scarcity.

Most commodities — crude oil, gold, silver, and agricultural products — are priced and traded internationally in US dollars. The US Dollar established itself as the most preferred internationally convertible currency since the post-World War period and serves as the international reserve currency for central banks worldwide.

The Dollar Index

The Dollar Index measures the strength of the US Dollar against six major currencies: Euro, Japanese Yen, Pound Sterling, Canadian Dollar, Swedish Krona, and Swiss Franc.

| Dollar Movement | Effect on Commodity Prices |

|---|---|

| Dollar strengthens | Commodities become more expensive for non-dollar buyers → demand falls → prices drop |

| Dollar weakens | Commodities appear cheaper in other currencies → demand rises → prices increase |

11.4 Correlation Between International and Domestic Markets

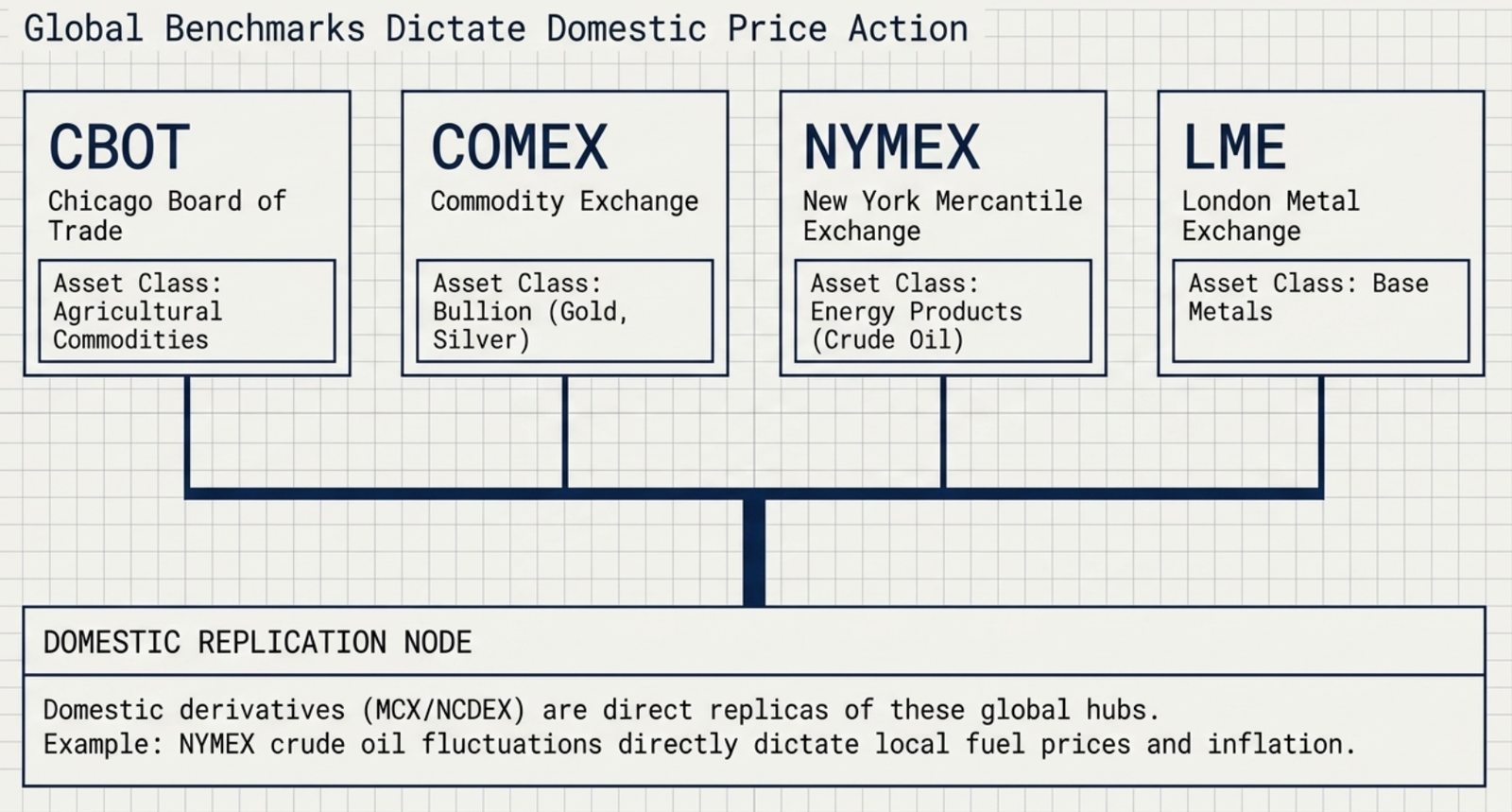

Commodity trading evolved from a barter system to organized exchanges in the mid-19th century. Major global commodity exchanges now serve as international benchmark-setting organizations:

| Exchange | Benchmark For |

|---|---|

| Chicago Board of Trade (CBOT) | Agricultural commodities |

| COMEX | Bullion (Gold, Silver) |

| NYMEX | Energy products (Crude Oil) |

| LME (London Metal Exchange) | Base metals |

The derivatives products traded on Indian exchanges (MCX, NCDEX) are replicas of their global counterparts and their prices strongly correlate to international exchange prices. Changes in crude oil prices on NYMEX directly impact fuel prices and inflation in importing countries like India.

Domestic commodity markets are also influenced by currency fluctuations, trade policies, and import-export dynamics. Strong local demand, government interventions, and seasonal supply variations can sometimes cause domestic prices to diverge from international benchmarks.

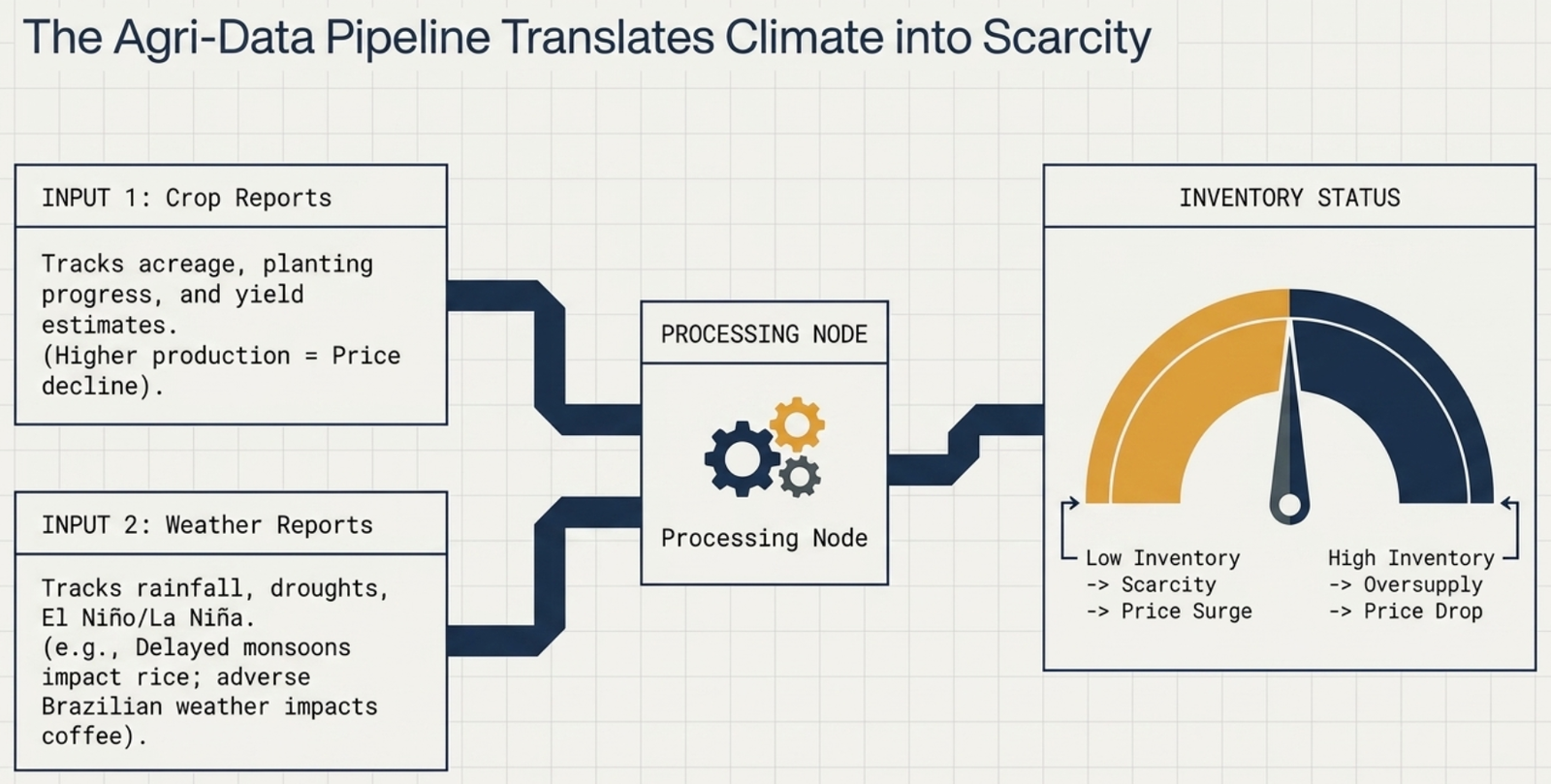

11.5 Crop Reports and Weather Reports

Crop reports and weather reports play a critical role in agricultural commodity fundamental analysis, as they directly influence supply, demand, and price trends.

Crop Reports

Crop reports provide detailed insights into acreage, planting progress, yield estimates, production levels, and inventory status of key crops. Released by government agencies or research organizations, they help traders, processors, and policymakers gauge the availability of commodities such as wheat, corn, soybeans, cotton, and pulses.

- Higher-than-expected production → price declines

- Lower output projections → prices rise

Weather Reports

Agricultural commodities are highly sensitive to climatic conditions. Rainfall patterns, temperature fluctuations, droughts, floods, and unexpected frosts can significantly impact crop yields.

- Delayed monsoons in India affect rice and sugarcane production

- Adverse weather in Brazil can disrupt coffee and soybean supply

- Long-term patterns like El Niño or La Niña create substantial shifts in global supply chains

11.6 Inventory Data, Production & Consumption Trends

Inventory data, production, and consumption trends are core pillars of commodity fundamental analysis as they directly reflect the balance between supply and demand.

| Factor | What It Measures | Price Impact |

|---|---|---|

| Inventory Data | Quantity held in warehouses, exchanges, or government reserves | High inventory → oversupply → price falls; Low inventory → scarcity → price rises |

| Production Trends | Supply being delivered to market | OPEC output increase → crude price falls; Reduced mining → metal prices rise |

| Consumption Trends | Demand dynamics from industrial use and lifestyle changes | Rising demand without matching supply → price rises |

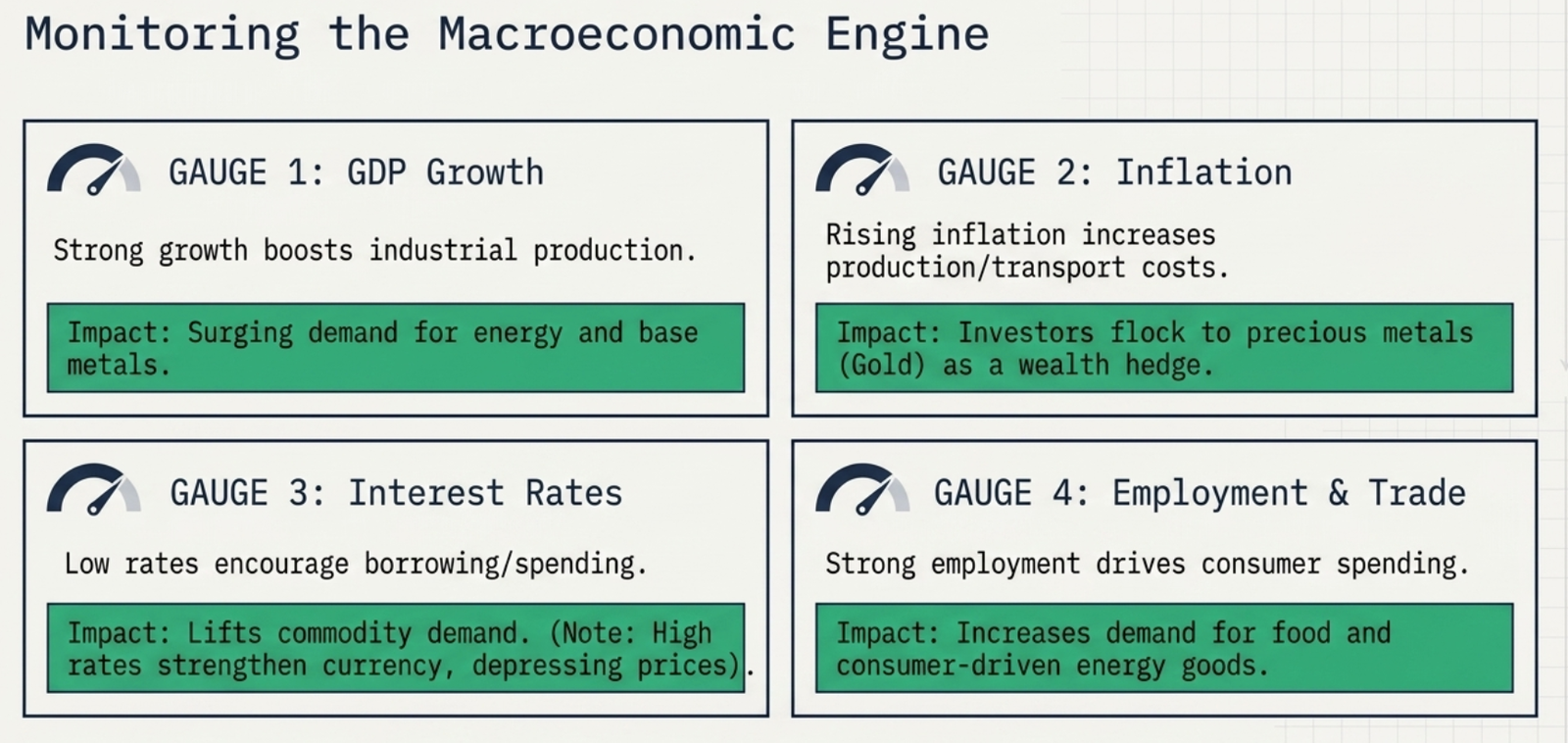

11.7 Macroeconomic Indicators Affecting Commodity Prices

Macroeconomic indicators reflect the health of economies, monetary conditions, and global trade flows. Since commodities are raw materials for industries and essentials for consumption, their demand and supply are deeply connected with broader economic trends.

| Indicator | Impact on Commodities |

|---|---|

| GDP Growth | Strong growth → higher demand for energy, metals, agricultural products. Recession → price decline. |

| Inflation | Rising inflation → investors move to commodities (especially gold as hedge). Also raises production & transport costs. |

| Interest Rates | Low rates → more borrowing & spending → commodity demand rises. High rates → stronger currency → commodity prices fall. |

| Trade Balances | Import-dependent countries face higher prices during supply chain disruptions; export restrictions tighten global markets. |

| Employment Data | Strong employment → higher consumer spending → demand for food, energy, goods rises. |

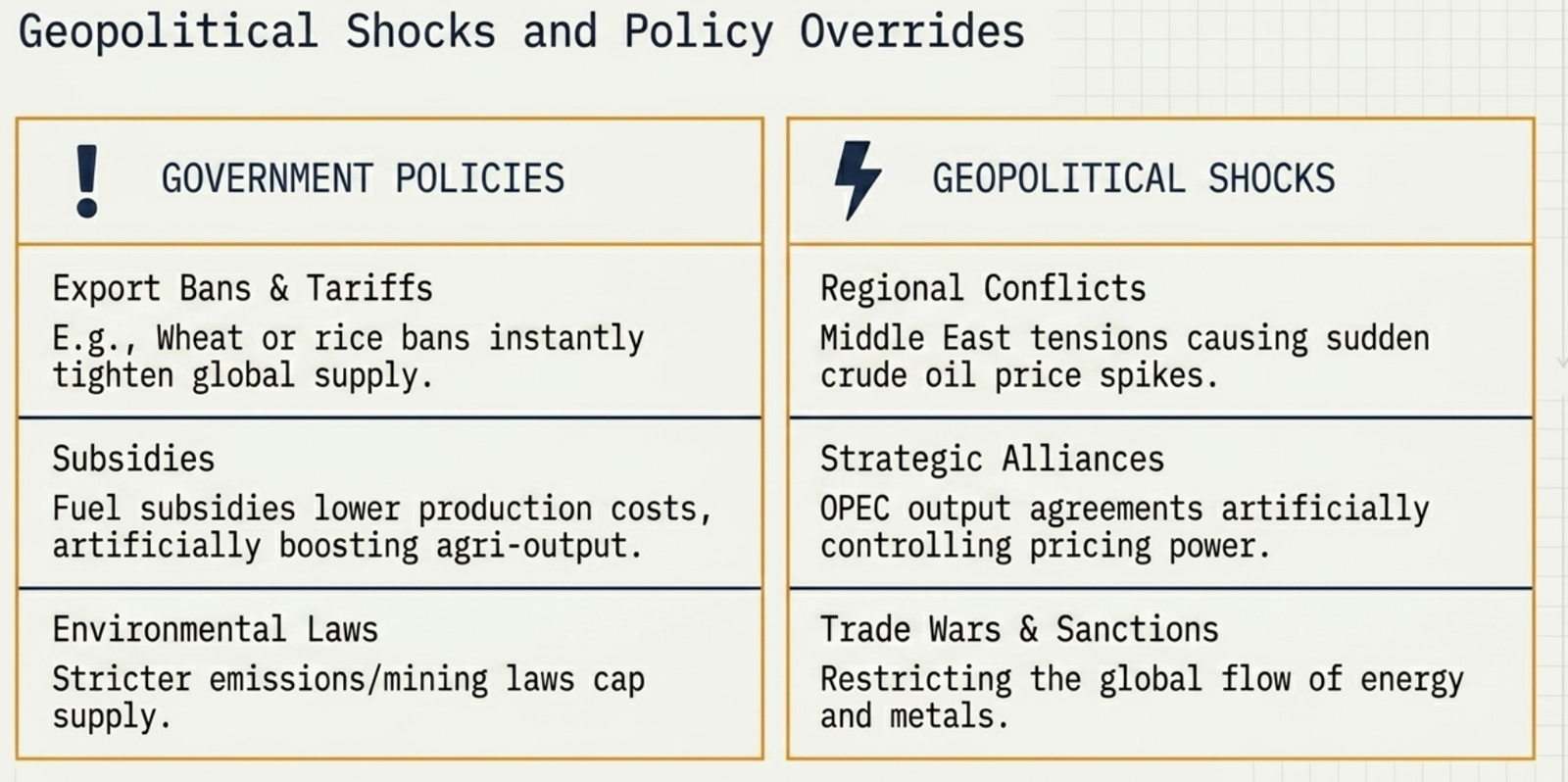

11.8 Government Policies and Geopolitical Impacts

Government Policies

Government policies directly shape commodity availability and prices through:

- Import-export regulations, subsidies, tariffs, and quotas – An export ban on wheat or rice tightens global supply and drives prices higher

- Fuel subsidies – Reduce production costs, encouraging higher agricultural output

- Environmental regulations – Stricter mining or emission laws may reduce commodity production

- Monetary and fiscal policies – Interest rate changes, taxation, and infrastructure spending impact industrial consumption

Geopolitical Factors

- Conflicts in oil-producing regions (e.g., Middle East) lead to supply disruptions and sharp increases in crude oil prices

- Trade wars or sanctions restrict flow of key commodities like energy, metals, and agricultural products

- Political instability in major producing nations — strikes in mining regions or unrest in agricultural hubs — can cause sudden supply shortages

- Strategic producer alliances (e.g., OPEC's output agreements) significantly affect pricing power and market stability

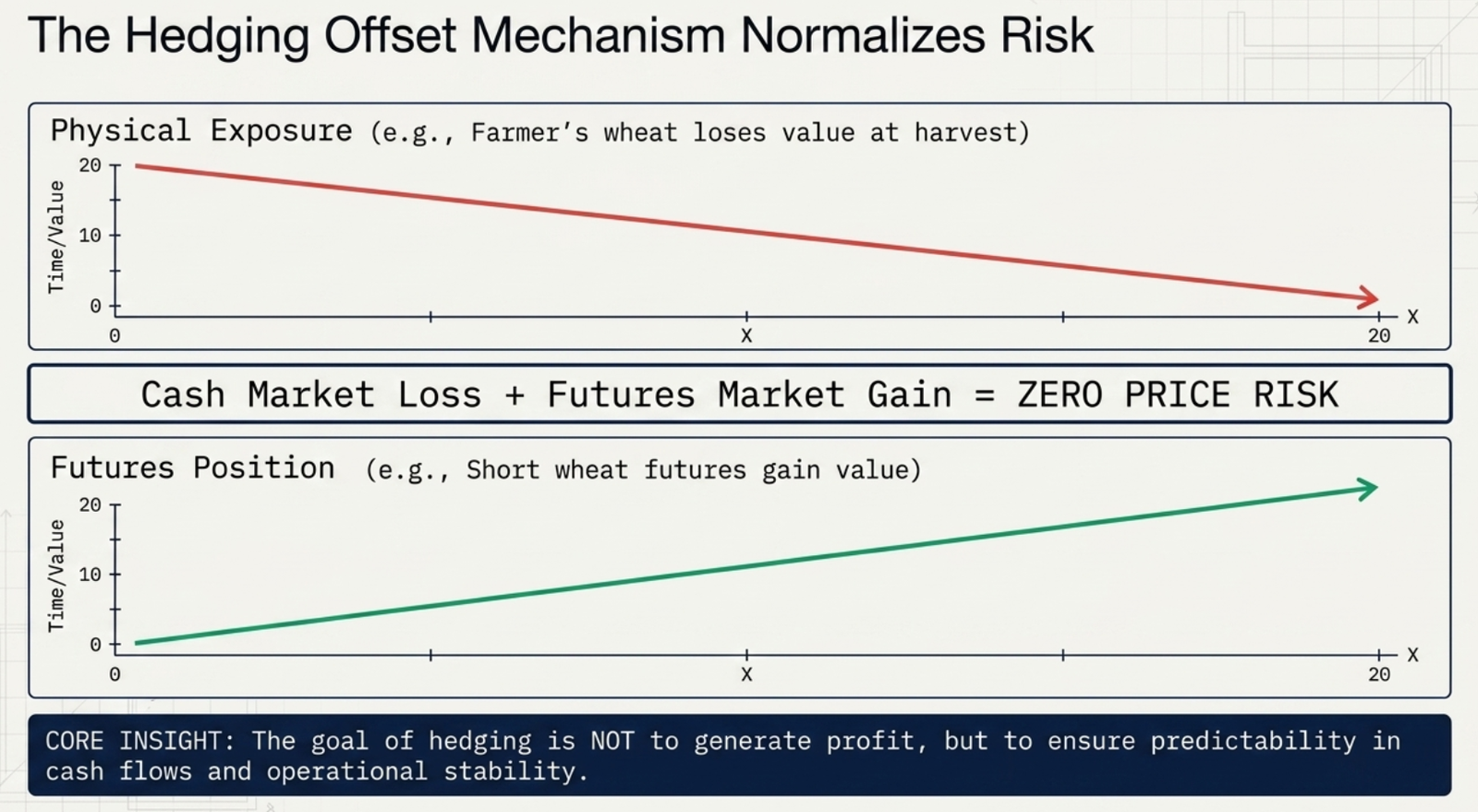

11.9 Hedging in Commodities

Hedging is a crucial risk management strategy used by producers, consumers, and investors to protect themselves from adverse price fluctuations. Since commodity markets are highly volatile, hedging provides a way to stabilize earnings and costs.

Hedging involves taking an opposite position in the futures or options market to offset potential losses in the physical or cash market.

- Farmer: Sells wheat futures in advance. If prices fall at harvest, the loss in cash market is compensated by gains in the futures market.

- Airline: Buys crude oil futures to lock in fuel costs and protect profitability against rising fuel prices.

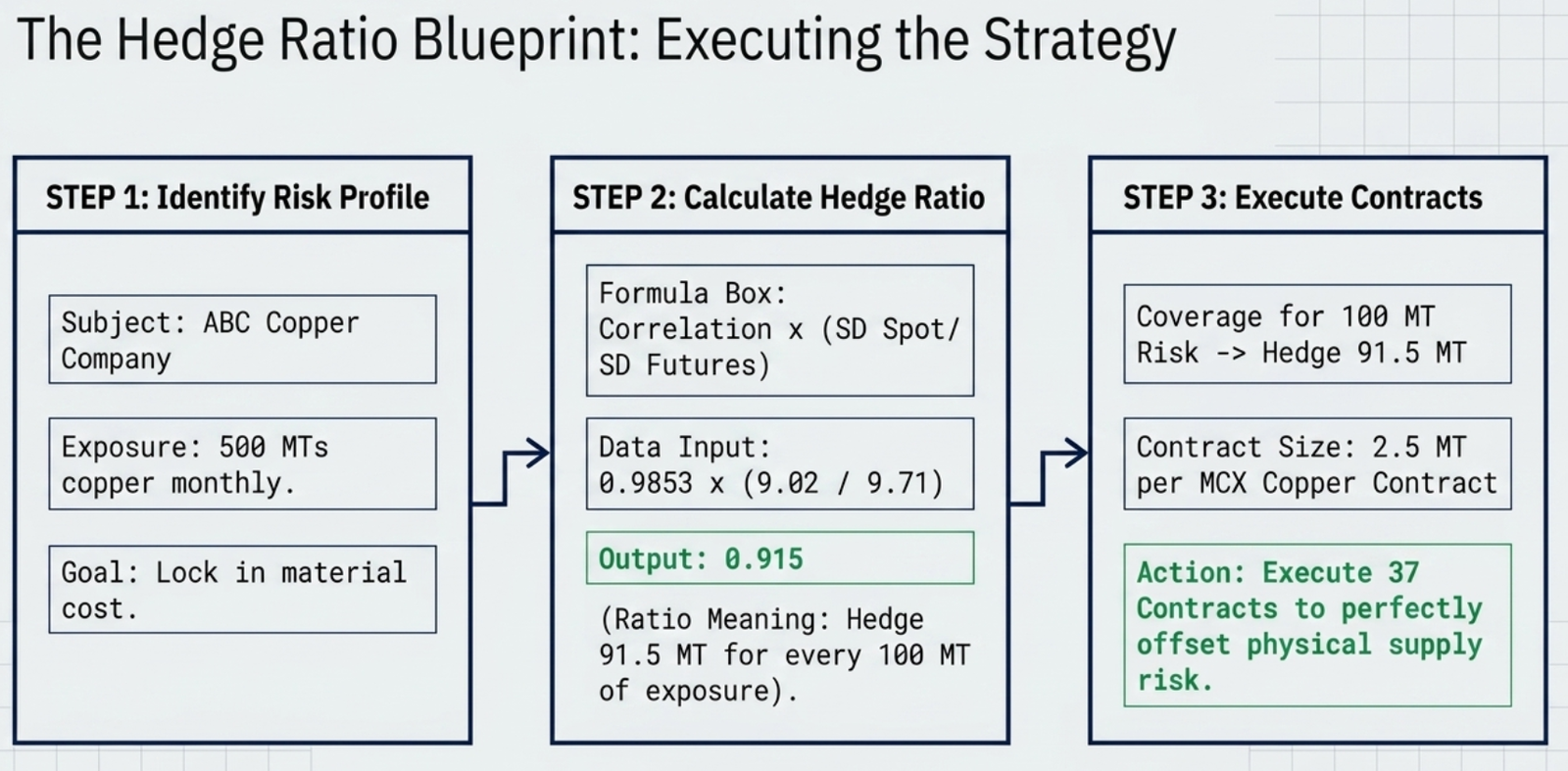

11.9.1 Hedge Ratio

The hedge ratio measures the proportion of a position that is hedged through derivative instruments.

Hedge Ratio = Correlation(Spot, Futures) × (SD of Spot Price Change / SD of Futures Price Change)

Worked Example – ABC Copper Company

ABC Company manufactures copper wires and requires 500 MTs of copper per month. Given the following data:

| Metric | Value |

|---|---|

| Standard Deviation of Spot Price Change | 9.02 |

| Standard Deviation of Futures Price Change | 9.71 |

| Correlation (Spot & Futures) | 0.9853 |

| Hedge Ratio | 0.915 |

| Quantity to Hedge (per 100 MT) | 91.5 MT |

| No. of Contracts (MCX copper = 2.5 MT each) | 37 contracts |

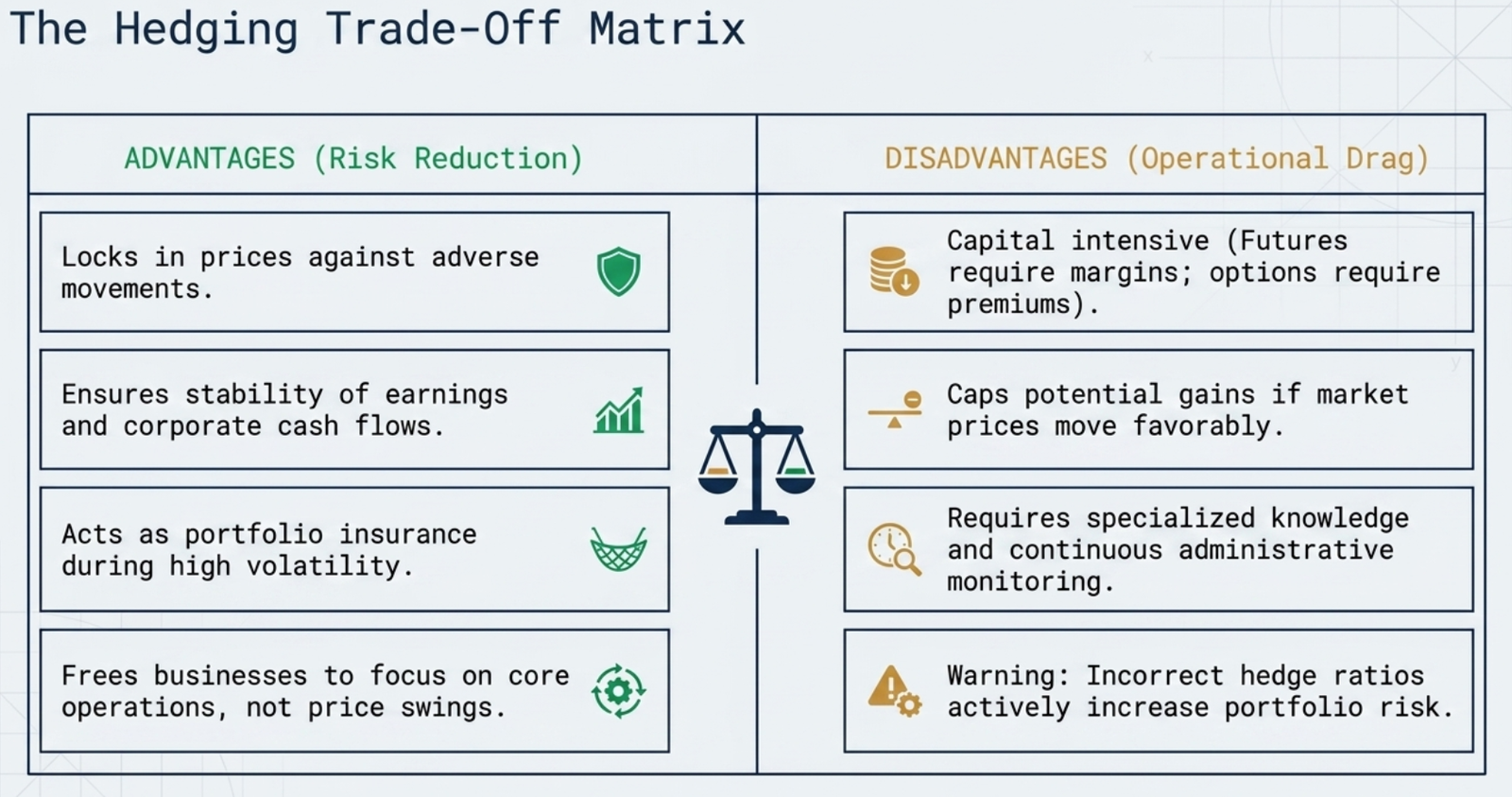

11.9.2 Advantages and Disadvantages of Hedging

| Advantages | Disadvantages |

|---|---|

| Risk reduction — locks in prices against adverse movements | Cost of hedging — margins, option premiums reduce profitability |

| Stability of earnings and cash flows for planning | Caps potential gains — if market moves favourably, hedge limits upside |

| Acts as insurance for investors during volatile periods | Poorly designed strategies or wrong hedge ratios can increase risk |

| Enables focus on core operations without constant price worry | Requires specialized knowledge, monitoring, and admin effort |

Key Takeaways

- Commodity prices are driven by supply-demand dynamics unique to each commodity, unlike equity analysis which focuses on financial statements

- The US Dollar Index is a key barometer for commodity traders — a stronger dollar generally pressures commodity prices downward

- Global exchanges (CBOT, COMEX, NYMEX, LME) set international benchmarks that Indian markets closely follow

- Crop and weather reports are essential for agricultural commodity analysis; El Niño / La Niña effects can reshape global supply chains

- Inventory levels, production capacity, and consumption growth collectively determine commodity price direction

- Government export bans, import tariffs, and geopolitical conflicts can cause sudden and sharp price movements

- Hedging allows commodity stakeholders to lock in prices and reduce exposure — the Hedge Ratio determines how much of the exposure to cover

🃏 Flashcards

59 cards · click to reveal the answer · use search to focus on a topic

📝 Sample Questions

Questions from the official NISM workbook

Q1. The _______ of commodities is largely dependent on the supply and demand dynamics of the particular commodity.

- a) Fundamental Analysis

- b) Technical Analysis

- c) SWOT Analysis

- d) Ratio Analysis

Commodity fundamental analysis is primarily based on supply-demand dynamics, unlike equity analysis which studies financial statements.

Q2. Which of the following factors affect global disruptions thereby affecting the global commodity market equilibrium?

- a) Increase in economic growth

- b) Stable political condition in the producing countries

- c) Currency fluctuations and trade policies

- d) All of the given options

These create instability in commodity markets. Economic growth and political stability generally support equilibrium, not disrupt it.

Q3. A _______ domestic currency against the US Dollar can make imports more expensive, in the scenario of rising global prices.

- a) Weakening of

- b) Strengthening of

- c) Stable

A weaker domestic currency means you need more local currency to buy the same amount of US dollars, making dollar-denominated imports more expensive.

Q4. Which of the following is the correct formula for Hedge Ratio?

- a) Correlation × (SD of Futures / SD of Spot)

- b) Correlation × (SD of Spot / SD of Futures)

- c) (SD of Spot / SD of Futures) / Correlation

- d) (SD of Spot + SD of Futures) × Correlation

Hedge Ratio = Correlation(Spot, Futures) × (SD of change in spot price ÷ SD of change in futures price).

Q5. The Dollar Index measures the strength of the US Dollar against how many major currencies?

- a) Four

- b) Five

- c) Six

- d) Eight

The Dollar Index measures USD against: Euro, Japanese Yen, Pound Sterling, Canadian Dollar, Swedish Krona, and Swiss Franc.

✅ Chapter 11 Complete!

You've completed Chapter 11! Here's what comes next: